Date: 31st January 2024 portfolio update

Quick update on my portfolio - continue to follow buy and hold strategy since deep down we all know it’s not what we do randomly that will produce long-term returns; it’s what we do consistently. So then question is what can be done consistently over long periods of time.

After many mistakes and paying high tuition fees, now I prefer to buy and hold quality franchises within reasonable valuation with growth triggers which can last for years (ideally) which top-quality management can harness to build either a moat or pivot swiftly while sustaining growth trajectory.

Below are the 5 core ideas I believe which helps me to find consistency in my thought process and actions subsequently

-

at a fundamental level, earnings drive share prices over time (as an exercise check how convergent or divergent is CMP from 5y/10y profit/eps growth rate)

-

only quality businesses can deliver earnings consistently in the volatile world we live in. my personal NEEV framework (consistent revenue growth, expanding OPM, higher reinvestment rate and shareholder friendly promoters) has helped in in this regard. quality is defined by key characteristics allowing businesses to grow sales and EPS at above-average rates and will continue to do so into the foreseeable future. That’s because of their generally high returns on capital and their ability to reinvest retained earnings at attractive rates and into large addressable market

-

our only job is to find such businesses within one’s own circle of competence which can deliver earnings for a very long time. this process helps me to remain interested, passionate to learn and build conviction to hold over time. due to this, I avoid real estate, banking, pharma (newly added to my anti-portfolio list) etc etc

-

find and buy them at reasonable valuation to it’s peers and industry to enjoy margin of safety. e.g. current PE (non-debt laden cos) or EV/EBITDA (debt laden cos) or P/B (financials) lower than 5yr or 10yr median

-

hold them forever (ideally) and do nothing. we need conviction to hold them forever. conviction will only come if we understand the businesses’ products, customers, suppliers (use porter’s 5-forces model). it’s a slow and incremental process (at least for me)

Here’s my current portfolio:

| Stock name | Weight % | Avg P/E | Profit / Loss % | IRR % | Action |

|---|---|---|---|---|---|

| MOST 100 ETF | 9.4 | 20.7 | 43% | 30.3% | |

| TITAN | 8.4 | 49.4 | 101% | 29.4% | |

| TIPS LIMITED | 8.3 | 20.6 | 122% | 72.3% | |

| BANK BEES ETF | 7.7 | 13.8 | 24% | 16.7% | |

| TATA INVEST CORP * | 7.4 | 29.0 | 202% | 166.6% | |

| BAJAJ FINANCE | 7.4 | 22.5 | 35% | 13.2% | |

| IRCTC | 6.8 | 28.0 | 164% | 59.0% | |

| COAL INDIA * | 5.4 | 5.3 | 69% | 125.1% | |

| ASIAN PAINTS | 4.8 | 47.1 | 11% | 9.3% | |

| NARAYANA HEALTH * | 4.7 | 25.1 | 44% | 84.4% | |

| INDIAMART | 4.6 | 51.7 | 3% | 34.5% | |

| PIDILITE | 4.4 | 57.2 | 32% | 14.1% | |

| TATA ELXSI | 4.0 | 34.0 | 75% | 58.4% | |

| DIXON | 4.0 | 50.2 | 127% | 93.5% | |

| VARUN BEVERAGES * | 3.9 | 47.8 | 73% | 59.7% | |

| IEX | 3.2 | 15.1 | 156% | 17.6% | |

| AMARA RAJA * | 2.6 | 13.3 | 31% | 89.7% | Added more |

| WONDERLA * | 1.8 | 29.8 | -3% | - | Newly added |

| PHANTOM VFX * | 1.3 | 28.3 | 23% | 37.6% |

*(asterisk) signifies <1 yr holding period.

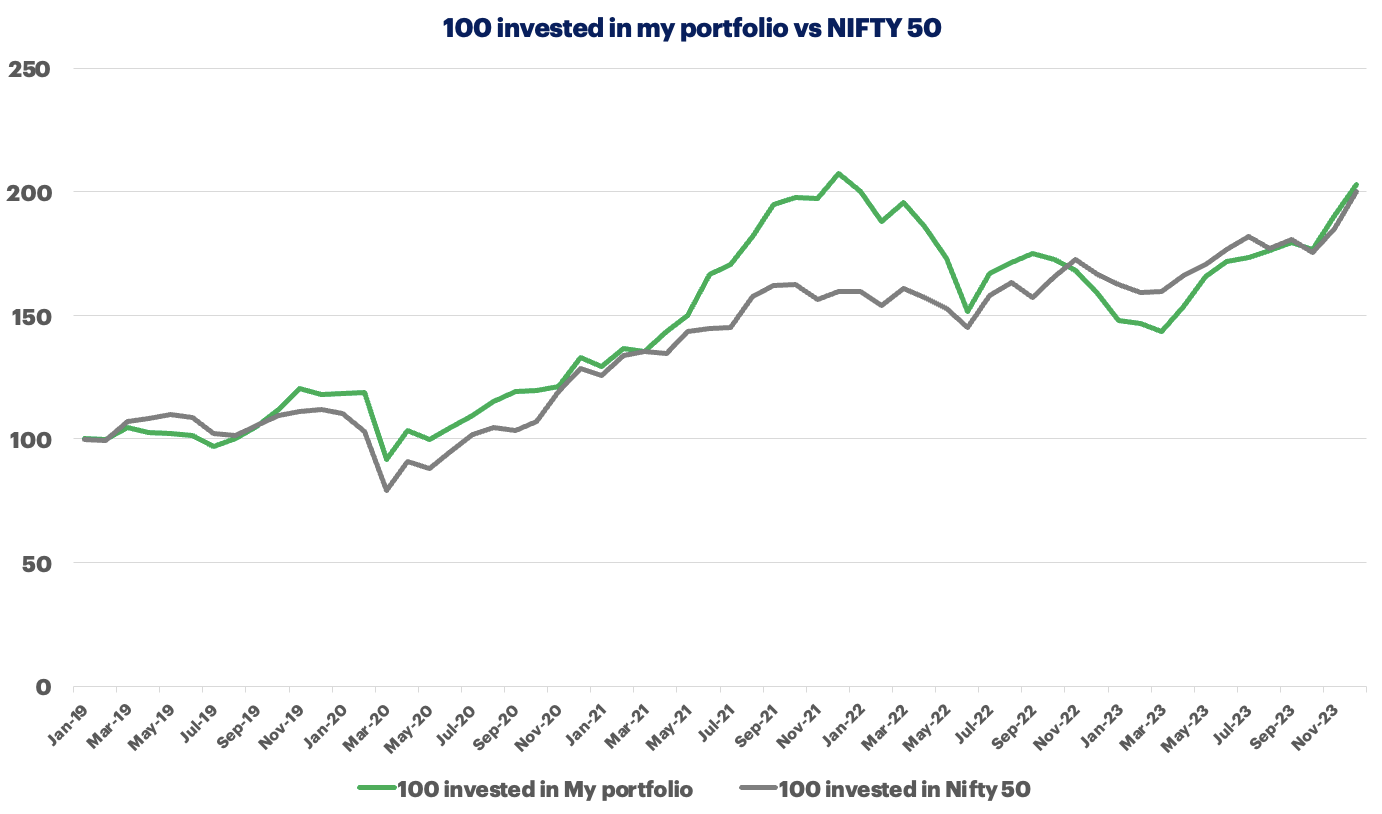

100 invested in my portfolio vs Nifty 50 index

Investments in Jan 2024

- WONDERLA - Company has similar traits to Narayana (long term mgmt, secular growth trends, steady compounder). Also simple business to understand with manageable monitorable growth triggers (footfalls, new park additions, increase in ARPU) and excellent financial metrics with management showcasing conservative approach to growth over long term.

Exits in Jan 2024

- KRSNAA - 100% exit. While much of the triggers are yet to play out (which I am sure it will), but wanted to concentrate my healthcare investments ONLY in Narayana Healthcare. also was finding it difficult to track and measure the B2G contracts effectively

- SATIA INDUSTRIES - 100% exit. Business has given a muted performance over holding period. Also, paper is a cyclical industry and during this phase price of paper increased which put pressure on price perception. In future, CMP will go up (opportunity loss perhaps) but happy to commit type 2 error than type 1

Finally here’s my investment thesis for WONDERLA: (this is my 1st investment thesis I am sharing publicly. please help me if possible. want to do better job of this in the future, so that others can also benefit)

Business model:

WONDERLA is one of the largest Amusement Park Chains in India. It presently has 3 operational parks located at Kochi, Bengaluru and Hyderabad and 1 resort in Bengaluru. They are launching 2 new parks - one in Odisha (2024) and Chennai (hopefully by 2025).

The parks offers 2 type of attractions - land rides and water rides for 8-10 hrs (whole day) for typically family and corprates who are ready to travel 1-1.5 hrs from city to outskirts.

The primary revenue source of the company is through entry ticket fee with further sub-divisions between normal and fastrack tickets (2x cost of normal). Each park has various restaurants spread across the park which contributes around 30% of the overall revenues — rest comes from ticket sales (70%). Sources of revenues for the parks are entry fees, food & beverages (F&B), retail products, sponsorship and advertisements, resorts and other miscellaneous rentals.

Peak season for parks is the March to June and October to December months. Kids are the major target segment of amusement parks and school vacations and festivals like Diwali and Christmas are when kids would visit the parks. ARPU for Q2 FY24 increased by 9% to INR 1,440 (expecting ARPU to grow in line with inflation plus an additional 5-6%). Attracts over 3 million visitors every year (expecting footfall growth of 5-6% per year in the future).

Indian amusement park industry: The first amusement park in India was Appu Ghar opened in 1984 in Delhi. The Indian amusement park industry is 5000-6000Cr (approx) and there are 150 amusement parks in the country (Wonderla has around 10% market share) – although slightly old data. The annual footfall for the industry is 58-60 million. This is expected to grow 10-15% in the next 5 years. Parks like Wonderla, Essel World and Nicco park (been there multiple times) fall into the large park category.

Major drivers for amusement parks in India are demographic advantages

- 28.5% of the population lies in the age group of 0-15 years

- 63.40% in the 15-59 and 8.10% >60 years.

Primary investment rationale:

- rising income levels

- increase spending on tourism and leisure activities

- rising urbanization are the other factors that will lead to more people visiting amusement parks

sidenote: in 2016, I was chatting with a sr personnel from TenCent and discussing gaming and TenCent’s various media properties. I still remember, he mentioned “when people become rich, they tend towards hedonism”

What I like about the business:

- High entry barriers (in terms of buying upfront land and rides) - MOAT

- In-house manufacturing of rides (to keep costs as low as possible, visibile from the fact the Wonderla spending around Rs 350cr all inclusive to start a new park)

- multiple levers to grow revenues

- hike in ticket prices with inflation

- non-ticket revenues (F&B, over-night stay in their own resort like in BLR)

- increasing capacity utilization of the land holding in each park

- operating leverage (every percentage increase in revenue, there is scope for 2.5 times increase in profits)

- Leadership and first mover advantage as it’s promoter driven

- Unorganized to organized

- Longevity due to management’s conservation style of operating

- Negative working capital business model

What I don’t like about the business:

- One of the two core ingredients of the business is real-estate which isn’t my area of interest and is subject to regulations and litigations like Wonderla faces in HYD.

Trackable growth drivers: - Monitor the following key parameters every quarter:

- Increase in Footfalls

- Performance of New Parks

- Increase in Replacement Capex

- Hike in ticket price

- ARPU

Risk factors:

- Accidents on premise

- Land litigation (e.g. Hyderabad)

- Capital intensive nature of the business (if any park fails to garner interest, then opportunity loss of 2-3 yrs perhaps)

Valuation expectations (Jan 2024)

currently business is valued at ~30x PE which is 30% higher than 5y median PE of 23x but just below 10y media PE of 32 (so ideally this should be a 10y hold to extract value given business is simple and has imminent growth triggers).

So I am today valuing the business NTM with 20% earnings growth, then PE falls to around 24x. ideally would have loved the buy the business <20x PE but given business current and future growth triggers, I doubt if we can get it in the near future. Highest PE, business had touched is 65x PE in 2017, then COVID struck.

Sources:

- Wonderla Holidays

- https://www.youtube.com/watch?v=Q7313vRmViE

- Wonderla Holidays Ltd: Fundamental Analysis - Dr Vijay Malik

- Fundamental Analysis of Wonderla Holidays Limited

Disclaimer: I am not a financial advisor and nor a SEBI registered advisor. The content shared here is only for learning purposes. So please use your discretion to make any buy/sell decision and not use the above as a recommendation.