Fair point @praky. Looking at the Q1 Inv PPT, we can clearly see a drop in content costs for FY24. On average it is ~25% of revenue over last 3 years. So, yes, we should expect a moderation in bottomline for FY25 as content acquisition picks up.

Importantly though, do you expect a moderation in revenue growth for FY25 as the content ages a bit and sustaining this level of 30+% revenue growth might be a challenge until new content acquisition resumes?

The movie arm of the business is Tips films. And there was 30 cr revenue from netflix from the movie plus some for the satellite rights and music. Net net it would be no profit no loss. I was previously tracking tips films

Well I will defer to management on that. I believe they have had the luxury to not acquire overpriced content because they saw they were growing still as per their targets of 30%. At some point that will wear off. Probably not for the next 3 quarters as the new revenue should kick in from the recent deal for YoY results.

However, i was more concerned about the margins and the bottomline. So far have stopped tracking the stock closely since it is compounding nicely without effort.

However, because of the elevated margins, I would like to see what kind of returns I should expect for the next year.

Saregama used to trade around 60 p/e with a worse business model (because of writeoff strategy and other lumpy businesses) when it was delivering 30% growth. So there is still some room here for peak valuations.

The company has brought in seasoned management. They have invested in software upgradation.

The company’s moat is a library of 30,000 songs, which will help them earn for the next 10 years. The major money-makers are 90s songs. The growth will continue to come from revised contracts/ new deals. 30% growth looks unsustainable beyond the next few years. Ultimately, they will converge to the industry growth rate of 14-15% plus or minus 2%.

With new management, I hope they are taking an analytical approach to content acquisition, making sound assumptions on music’s ability to earn Vs acquisition cost.

The company’s acquisition cash flow is quite less because they are bound by 30% topline and accruing everything in the same quarter. Whereas, Saregama is aggressive with cash outflow on acquisition. Being conservative, you can be picky on good music. Whereas, being aggressive can lead to a “spray and pray” approach.

I hope that the company should master their ability to forecast music success. I will be happy if they invest in AI/ ML technologies to do the same.

The other good thing I am hearing is comany’s focus on quality Vs quantity. You attract more audience with one superhit song Vs multiple flop ones. Also, superhits help you position your portfolio in front of the downstream players.

I am quite hopeful for aggressive growth in next 3 quarters due to Warner deal. What will be next year’s catalyst? That is the question. If they keep on finding these catalysts, the stock should do good.

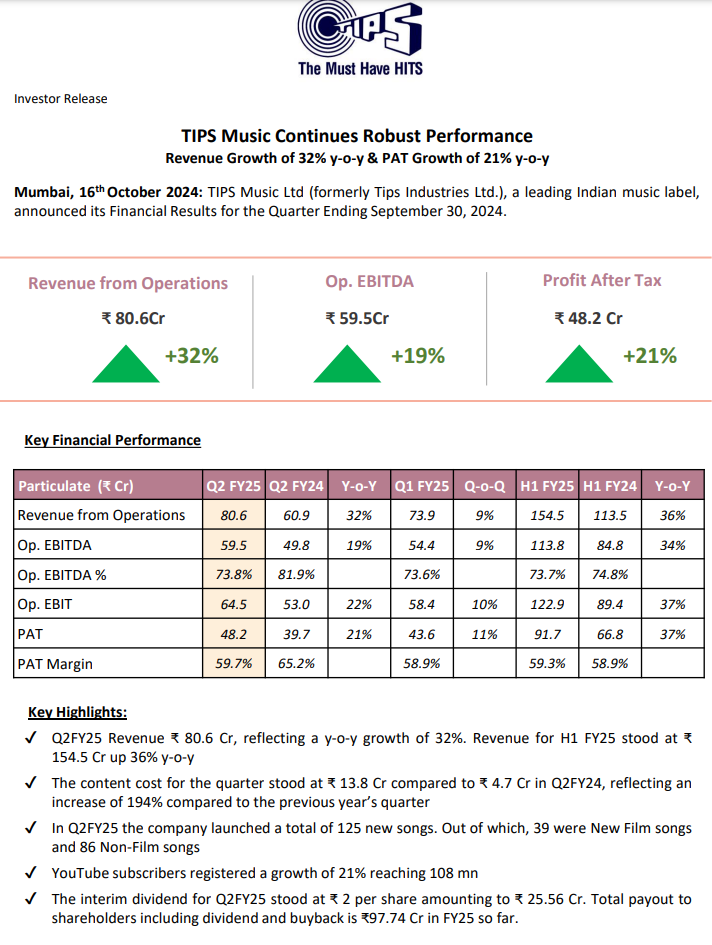

Guidance is conservative as always, ~30% though it might probably be elevated for FY25 looking at Q1 results.

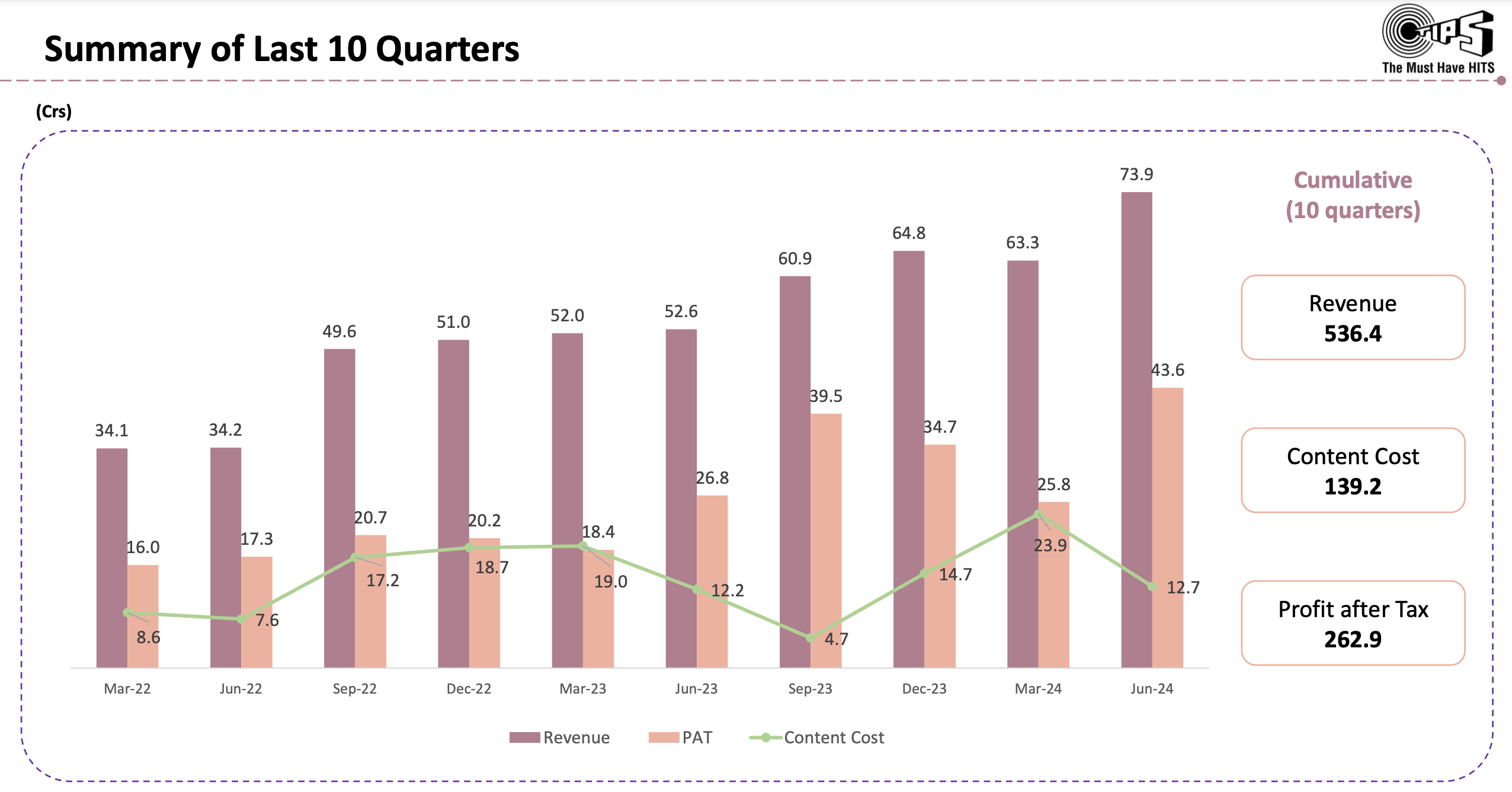

Count of songs released: in Q1, ~100. Target for FY25 is 300. This number was around 900 for FY24 and 700 for FY23.

Content costs target for FY25 is 80Cr. This number was 55.6 in FY24 and 62.4 in FY23. Essentially back to 30% YoY (from FY23 number) in line with topline guidance.

Overall, yes, partially agree that there might some more room for peak valuations. There also appear to be enough avenues for growth in coming quarters to sustain the added content cost jump. My take is we might see time correction if this doesn’t align. That will allow earnings to catch up to valuations.

This is due to a broader shift in investor sentiments towards consumer stocks.

However, this is a great business for the longer term. At least, till the growth continues.

A great business requires very little capital to pursue its growth. Tips has a very high RoE and RoCE.

The company is prudent about capital allocation. They do not unnecessarily reinvest in business and believe in returning the extra cash to investors.

This company is decreasing the number of shares outstanding through buybacks. Typically, companies do the opposite and dilute equity.

I will refrain from commenting on the present valuations. They can correct also. But for a long-term investor, this is a great business to hold.

Globally, the music label business is getting investor attention. 2 years back, Bill Ackman took a significant stake in UMG. Also, select global PE firms are buying music libraries, because they act as an annuity.

Wonder how are they able to generate higher profit margin than Shemaroo given both being in similar segment, any one who is tracking the business can answer.

MCap of Tips is now bigger than that of Saregama. Saregama used to be very popular back then thanks to big words of the management while Tips was not so popular due to not so professional management. Tips gave 400% returns since then as compared to 50% returns in saregama, not counting the Dividend and buybacks of tips.

I went through the recent concall to make sense of the valuations, lately this had become more like a passive investment.

The stock trades at 75 p/e now. There are several brokerage reports covering the stock like Arihant capital etc. The DII and FII % are approaching 5%. Management as always have promised 30% growth and maybe only now the market has started believing. I am not an expert on valuations but 75 p/e for 30% growth looks expensive to me.

Concall wise, quite bullish.

Content acquisition is still going slow.

But their warner deal would provide a step up in grwth for the next 3-4 quarters. Warner was still ingesting content.

They are trying for brand sync deals. Signed one with motorola. Value not mentioned, more to come. No idea on how meaty this could be.

Yet to decide on events business, maybe next quarter there may be an update

Wynk app shutdown may impact for 15 days, management thinks users will move to other platforms

Yes its at a 75p/e and I am contemplating selling out as well

But here are a few thoughts on why I am in a dilemma on this

1.The capital intensity of this business is very low so we get back a lot of the cash flows in the form of dividends and buybacks so its not an apple to apple comparison with other business on p/e alone

2.If their guidance of 30% is met for next three years the stock is at a 35 p/e then and added bonus of people moving to paid subscription could play out for a long time to come so could still be a good hold even then

3.The management is usually conservative on the guidance and they seem to be doing better than what they promise so hoping they keep doing so. They seem to be rewarding shareholders with buybacks and dividends so hopefully they keep that going too. EPS has basically tripled in 4 years due to earnings along with buybacks excluding the dividends

4.Their profits are bit understated because of the write off policy so 75 p/e is a bit overstated here. Rougly TTM PAT is 150cr and content cost out of that is like 65cr, so we might have to adjust for this. Also besides the content cost rest is payed out to shareholders in terms of dividends and buybacks

Would love to hear thoughts on this dilemma

Since my issue with the company is only the valuation, I am hanging on but dont know what I would do if this rally keeps going

Really interesting and most relevant point you have covered here

Prakash and Manoj.

Adding on to your discussion I personally believe that TIPS might even trade near 100 PE

Here’s why

The 30%CAGR PAT and sales growth is a very conservative guidance given by the management.

They have been giving same guidance since past 3years and easily managed to grow way beyond that.

Also I have watched many interviews of kumar taurani he has been very confident that in next 3-4 years the industry size can easily grow to 12-15k crores which is 4-5 x of current industry size

So you can get an Idea about next 3years of PAT and sales of TIPS considering a 10% market share.

Also if we look at the paid subscription not even 1cr indians have shifted towards paid till now. So you can imagine how much scale is possible in next 10-15years.

2 Music is an integral part of any Indian wedding and currently we Indians hardly pay for the music public perfomance rights and this segment has the potential to generate 10-20k crores of revenue alone - kumar taurani mentioned in a podcast.

now look at all the consumer facing businesses in India like Nestle,britannia etc

Their past 10yr median PE has been around 50-75 and their 10 PAT and Sales growth has been around 8-10% CAGR only

But why such high PE ? When they are hardly growing at double digits

Because of extraordinary high ROCE and ROE

That too with high FREE CASH FLOWS.

This is what I believe

And now comparing TIPS which is also a consumer facing business

75 PE at 30-40% PAT growth is not too high and also even when the growth phase stops after 5-10 years still I believe it will trade at around 50-60-70 PE range.

The music label business is not a usual business, where people understand cycles.

I feel this is an unchartered territory. The difficulty in valuing Tips is understanding how long this growth can last. Tips will do 30% topline and bottom line in FY25 for sure. But can they repeat this in FY26 and FY27?

If they can, this is a fair valuation.

If the valuation goes excessive (90-100 PE), one can definitely exit. Because the company will be a 15000 Cr company at that valuation - assuming very bright future in times to come. Risk reward will be quite lopsided.

In any case, i am not contemplating selling more than 10-20% of my holding. As I said before, the stock has started garnering attention only now, bROkerages, fii and dii.

I 100% agree that the company is unique. I have always maintained that it is even better than Saregama for me due to consistent growth, Pure play music and conservative account practices. I do see a lot of growth levers available to them like brands, events etc.

But I would remain on the lookout for valuations as well. 100 p/e is not far actually just needs a 33% jump from here before next result.

Seeing people discussing valuation of Tips Music on PE matrix. In my opinion Tips Music is a pure play music label which cannot be valued by just calculating PE by seeing profit alone. Tips is charging content cost in expenses of P&L account and not capitalising it and the content cost is kind of not a raw material for top line of the same period, it is more like a capital expenditure for future growth. Suppose, if Tips gets an opportunity of buy very good music at good deal and they spent almost all the revenue for the particular year in buying that content then the PE will be very high or in negative but the company will save good amount in taxes apart from ensuring solid growth. Content cost can be a problem if the company is not spending prudently, however, having observed the strategy of Tips for last 4-5 years, I thing they are quite conservative and prudent in buying new music.

If I have to value the Tips of PE matrix alone, I would calculate based on top line and not on profit. For instance, TTM Sales are Rs. 283 crores which results in operating profit of Rs. 268 crores (assuming 95% OPM, ex of content cost). Now, lets assume there is tax rate of 25%, the PAT works out to be Rs. 200 crores. Now calculate the PE, it is less than 60 and not 80-90.

Having said that, I understand if they don’t do content acquisition, the growth will slow down but I feel most of the growth is coming from their legacy content coupled with structural shift of paid customers and ads revenue of music platforms.