@Anand6 Ji, can you please share the source/link of where you found about Tiger only continuing with advance payment business?

Disc- no holdings as of now.

@Anand6 Ji, can you please share the source/link of where you found about Tiger only continuing with advance payment business?

Disc- no holdings as of now.

I was fascinated by this company due to its high high ROCE, 59.2 %. The ROE is also quite good at 57.8%.

If you compare with some others, the ROCE of Alcargo is 26.41. The much touted Mahindra Logistics is not anywhere near it. A PE of 97.40% would be for me, a strong deterrent. To cap it, Mahindra’s ROCE at 8.26% is not much to sing about.

So many famous investors like Peter Lynch are votaries of undiscovered gems. In fact, Lynch ignores stocks which are in the kitty of some Mutual Funds already.

So, Tiger has so much going for it. Personally, the find has been good to me. (To an investor quite often a find clicking gives a sort of glow.)

Then I saw this post on moneycontrol today, " Its running not due to already declared results, but due to recent Chairmans interview in which he mentioned about the digital platform for logistics they are launching in couple of months which is expected to be a game changer for the company." So I decided to look for the Chairman’s interview. I have found one here: Interview : Tiger Logistics to launch one-of-a-kind logistics digital platform which will be a game changer for the industry - India Shipping News

How reliable do we consider such interviews?

By way of disclaimer, I am a novice, and it should not be construed as a recommendation.

Tiger indeed has been ferocious ever since publishing Jun’21 quarterly results, choosing to move in consecutive circuits from 55 until peaking at around 280 in Jan’22. In terms of performance, nothing much has changed in 2022 however the stock strangely started bouncing up from 220 to 340 in just 2 week’s this Nov.

I have been riding on this tiger since mid 2017 attracted by a sharp correction from 292 to low 200s. My bet was on the overall logistics industry back then with huge potential for growth. From my entry price at low 200s with 4000 shares, I was accumulating heavily through its fall at 30-70 levels and brought down my average to ~ 65 with 10x initial quantity.

Have offloaded nearly 3/4th of my holding at an average of 250 and never been tempted to add after accumulating until Aug’21

Although I still continue to bet heavily in the logistics space, Tiger’s ride will most likely be bumpy and I doubt there will be any strength left in the current rally. I see the price consolidating at 250 to 350 levels for next 12 months before making its next directional move.

Last time the fall was more to do with its heavy debt and high receivables, both of which have been taken care pretty well in the last 18 months. As long as the strength in this aspect continues, the tailwinds in the industry and company’s aggressive growth plans will continue to drive its price well in the long run.

Its actualy come down to around 67%.

Q3 results are not backing the rally witnessed in the last 3 months. Sharp pullback is more likely. Sub 300 could be a good level to begin accumulating.

A Tanla moment?

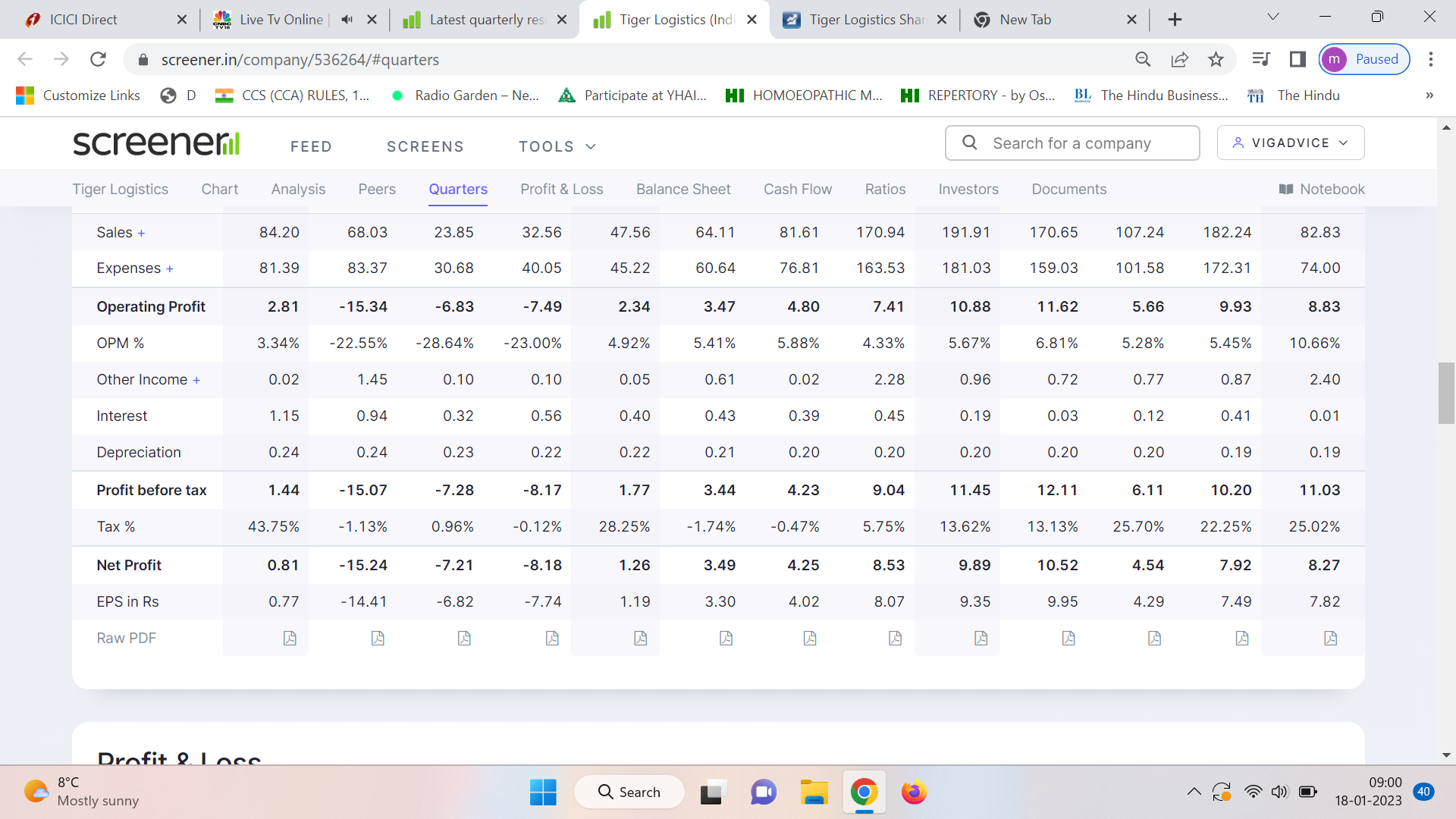

The sales are down to 82.83 cr from 182.24 cr from the last quarter, but the profit before tax is up 11.03 cr from 10.20 cr in the previous quarter. Even net profit is up to 8.27 cr from 7.92 cr.

Have overcome the initial panic. As a novice at this game unable to really understand the results.

What do the veterans say?

Turnover of Tiger is a pure play of international freight & container rates which has been cooling off largely over the months. Its profits are pure play of its ability to pass on other operating costs to its customers which has been improving in leaps and bounds over the months. Quality and cost efficiency of service, customer satisfaction are key attributes that help improve its bottom line.

What i understand is Tiger’s volume almost halved during pandemic, but the unit spot rate shot up so high that the top line didnt show it much until last qtr. Now that the rate has normalized the top line showing it, last qtr sales halved. But since they were able to get higher margin, profit is holding up.

Correction was imminent since the q-o-q sales growth was declining. But i guess since the profits are holding up, it didnt crash so badly even after halving sales.

But at the same time they are improving steadily. They were bold enough to keep tight check on credit and margins even if it means taking a hit on volume. And after all that, they are able to generate better margins. Looking great to me.

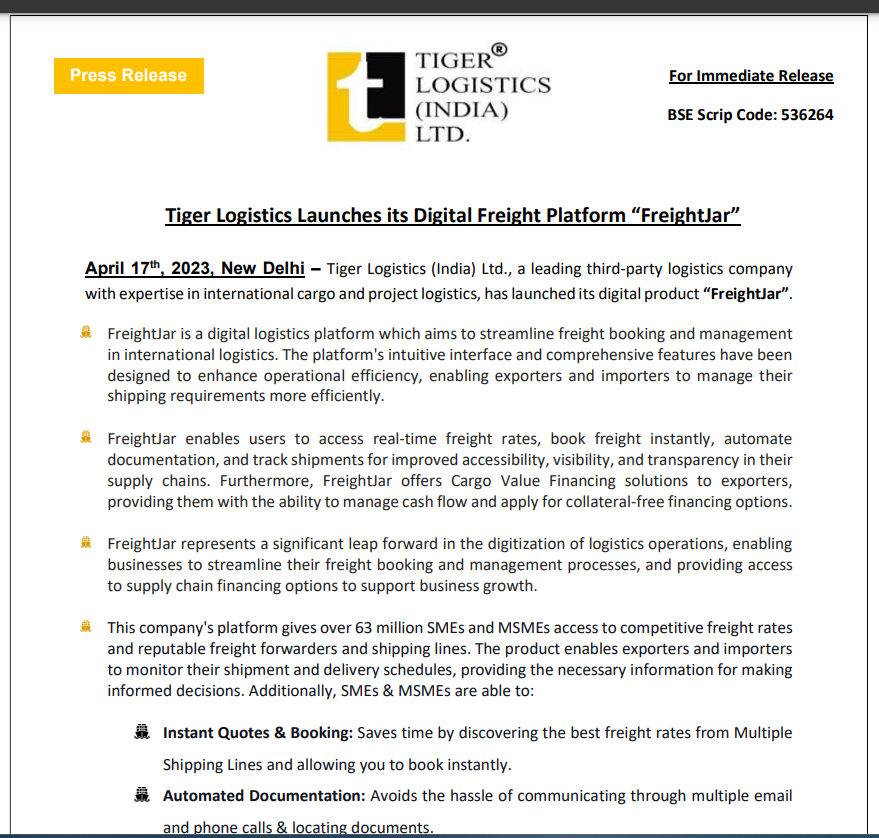

Freightjar – New launch from the company looks promising and considering the wave of the recent multiple SAAS companies in the segment havin great success, I am quite bullish on this product - provided how are they able to cater to the demand esp. the growing market of D2C brands which has huge potential.

Company EPS reduced in last 1 year.

Sales consistently going down since Sep 2022 quarter.

then why there is sudden upside in share price in last 2 months?

what is working for them? any big news?

Anybody tracking Tiger? It looks attractive after the fall?

My observation for Tiger Logi are:

TIGER LOGISTICS; Jindal Stainless Renews Trust in Tiger Logistics for International Steel Shipping

Under this extended agreement, Tiger Logistics will oversee global logistics for diverse steel products, ensuring uninterrupted shipment from India to over 30 countries. In FY24-25, Tiger Logistics managed more than 3,000 containers for Jindal Stainless.