Net profit 35 L vs 2.98Cr QoQ

I could not find any investor release yet on their website or any statement from management. Stock is locked at 20% lower circuit

Can we trust the management justification?

3 Likes

A naive question, how does the NBFC liquidity situation affected a logistics business ?

Tigeer selected as logistics provider for maruti and another auto company

1 Like

In addition to being a voracious reader, going on treks he is also great with the culinary arts

http://www.tigerlogistics.in/uploaddata/Notice%20of%20AGM%202017-18.pdf

2 Likes

Had the chance to get some replies from the company:

How is the foray into the domestic market proceeding? How has COVID hampered domestic expansion plans?

At this moment we are not looking to expand into domestic market as that would need additional funds to set up the whole structure. We feel time is not right for the same due to this pandemic.

Is the company into cold chain logistics? and will the company get a COVID vaccine distribution deal?

Yes, the company is in the cold chain logistics handling grapes/fish etc. and as far as COVID vaccination deal is concern we will disclose it at public platform, if any.

In the last phase of revenue growth, sales increased along with receivables! Hence cash generation was not strong and debt had to be raised. Why did receivables increase at such a fast pace then? Was tiger giving unrealistic credit terms just to grow? Is the market too competitive?

You yourself understand that market is very competitive, in order to tap new client base, the company adopted the strategy to give a bit more credit period with proper cautions. This is the reason why our debtor velocity ratio has got effected. It was well strategized move and factually during COVID times we managed to recover approximately 60% of our total CC limit.

In the latest results the company has given out, the cash generation has been very strong while the company has posted EBITDA loss. Seems like the company has collected past dues. Can you please explain this?

Just reversing the earlier strategy (as mentioned in the above reply to offer more credit period), Now in the COVID times we have enunciated to reduce credit period and started to recover our receivables with full pace. We have already explained the rationales behind the EBITDA loss at BSE.

Currently the debt on the books is around 20Cr. Once growth comes back again the company will have to raise working capital debt? What is the guidance on debt?

After recovery we have paid our bankers and now utilizing only 30-40% of total cash credit limit. It has reduced our finance cost and yes , since it is a CC limit in the form of working capital loan so we can use it depending upon the future requirements and profitability of business.

Fixed assets have gone up in the last few years because the company has bought a new office it seems. What was the reason for this? How is it adding value to the company?

Now we are in the new office premises, sitting all together. For the betterment of company, It is always virtuous to provide better employee friendly space cum environment.

Why are we confident about a new growth phase emerging in the coming years for the company? How is the company preparing for growth from here on?

The economic conditions of our county is well known by all. Export is only one available remedy to stabilize it , to do any such transactions the requirement of freight forwarders will immensely increase positively. it is just the matter of time, after the fear of COVID we are expecting situation will improve completely for all of us.

8 Likes

Revenue is meaningfully down. How do we plan to get back to 60-70 cr of quarterly revenue run rate?

These days our management is choosing business with mindful reasons. We are not having the scarcity of orders so its just the matter of time. After the issues of Covid, situation will be improved.

What is the strategy to scale the business and get more good quality clients who give the company sticky business? As stated in the above answer, we have the business . Our almost (all) big clients are still with us so management is hoping for the best. Further we are regularly participating in various tenders to get new clients.

4 Likes

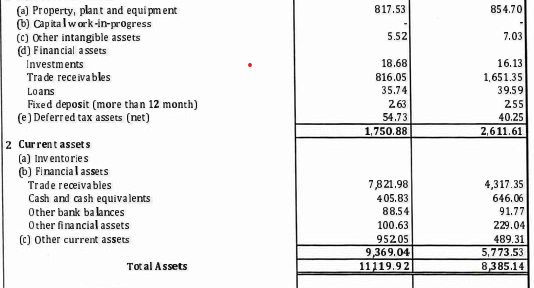

@KB0707 @bheeshma Are you still following the company? Revenue has doubled QoQ and YoY… But they have accounted trade receivables under current as well as non current assets, more over trade receivables increased 35 cr (current) during last 06 months…Any reasons??

4 Likes

Trade receivables classified as non-current may be due to the Project Logistics segment wherein retentions from invoicing are common practice. Retentions could be long term or short term depending on the completion stage of the project.

In any case, the net increase in trade receivables in this quarter is 21 cr on a turnover increase of 89 cr which is quite reasonable considering the heavy influx of business.

Best part is the results are the reflection of strong under current in the economy that was hijacked by covid world over for 15-18 months.

However, the ocean freights that witnessed nearly a 3 fold increase has come under severe pressure and are already down 50% from 6th Oct level.

Hence the topline can drop sharply in Q3, but volume growth can partly offset the price pressure.

As the stock has got beaten down badly from its all time highs in 280s , still there is good steam left in the current rally.

1 Like

baltic index is wrong index to look at for freight rates. have to look at drewry index. chart is below.

3 Likes

I have not come across this index before and hence thanks for referring. Holding this stock for over 5 years now and kept adding heavily in 35-60 range as I somehow felt the leadership was strong enough to sail the company through the troubled times especially during covid.

With an upcoming first time dividend announcement in Nov, there seems more interesting times ahead for this company.

3 Likes

Another interesting aspect from H1 presentation:

Company expects 575 cr turnover for FY22 which means 324 cr for H2. At a conservative 4% net profit margin, we can see 13 cr added this year taking full year EPS above 25.

Similar buoyancy was witnessed 5 yrs ago, but given the industry head winds & global pandemic, all expectation were quashed. However this year, recovery has been pretty sharp.

Interesting times indeed ahead! Good stock to be in at current prices.

3 Likes

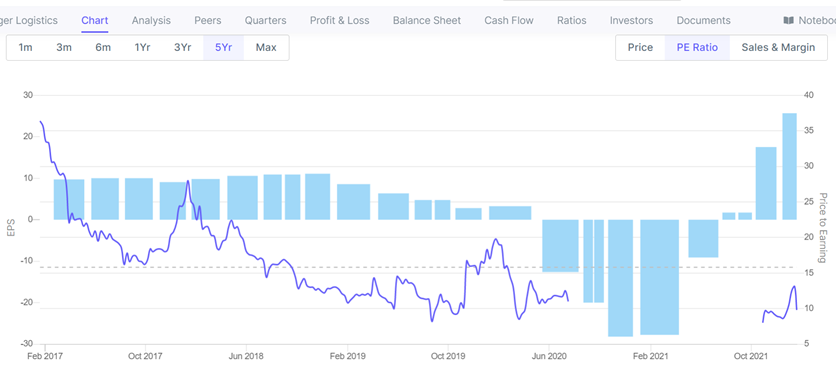

The PE ratio is five year low, It looks very attractive. @Lakshmi_Narasimhan_B has the business by the company improved significantly? Could please comment on the future prospect of Tiger logistics.

https://www.screener.in/company/536264/

1 Like

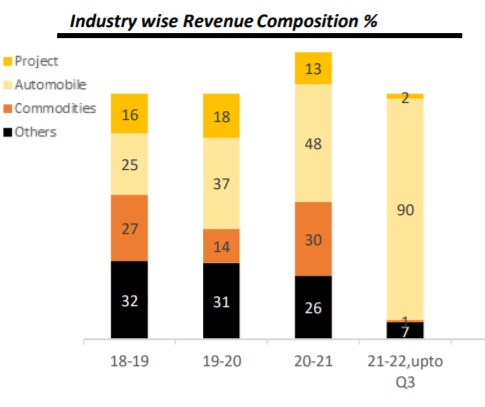

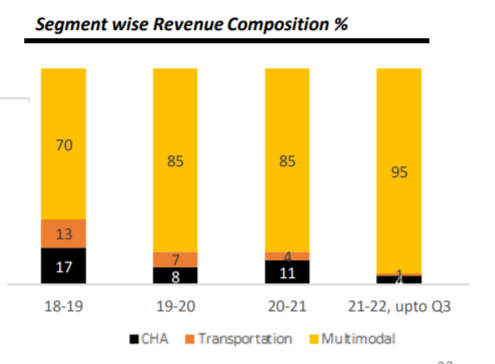

While going through the presentation, couple of points I felt could be a bit of risks are -

- Concentration of Auto has dominated other sectors -

- Segment of Multimodal now dominating other segments -

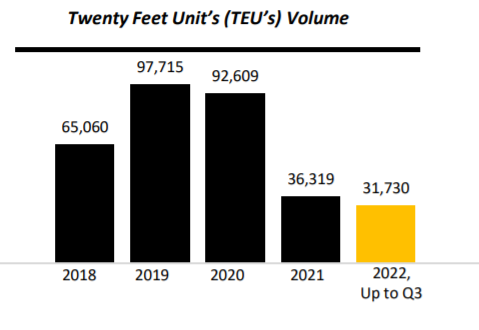

- Volume of TEU’s seems to have reduced drastically -

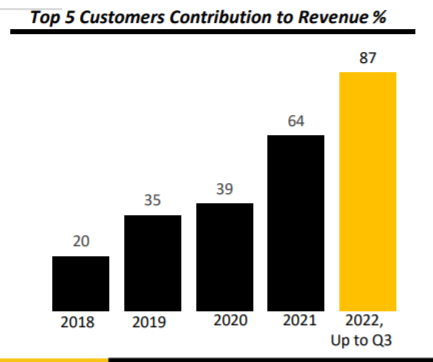

- Customer Concentration has also increased -

If any one can highlight what I am missing here. In the past, if company has changed its course of focus or if there are any signs of healthy volumes in any other business segments. I can see the results have improved but not able to understand the base of the improvement.

Discl. - Not invested, tracking closely.

4 Likes

@jaman_valuepickr, I have offloaded 25% off late without any plan to add further.

I strongly believe the performance will only keep improving going forward as long as the company is in control of its debts and receivables.

500 levels in next 12 months is a distinct possibility if current performance is maintained with a baseline annual profits of 25cr.

3 Likes

Based on an interview of management, I am trying to give answers.

→ Tiger had stopped all business where customers were not giving advance, all credit based business had stopped. Result was loss of customers except few auto and ancillary cos who were ready to give advance. So top client contribution went up and TEU volume went down.

→ Freight cost went up anywhere between 5x-10x, resulting higher topline compared to volume.

Typically freight forwarding is high topline low margin business where company doesn’t own any ship or container. Historical opm between 3-6%.

Hope this clears some doubts.

6 Likes