Thanks for tagging me. I’m bullish on the D2C business model and I follow the space out of interest, but I’m not an expert by any means.

On these new brands, it’s still too early for them to alter the Marico investment thesis. A quick search tells me both these brands are around the Series A stage, which means they’ve turned profitable but are yet to scale. If Marico stays focused on good social media, these brands have a runway to scale over the next 5 years.

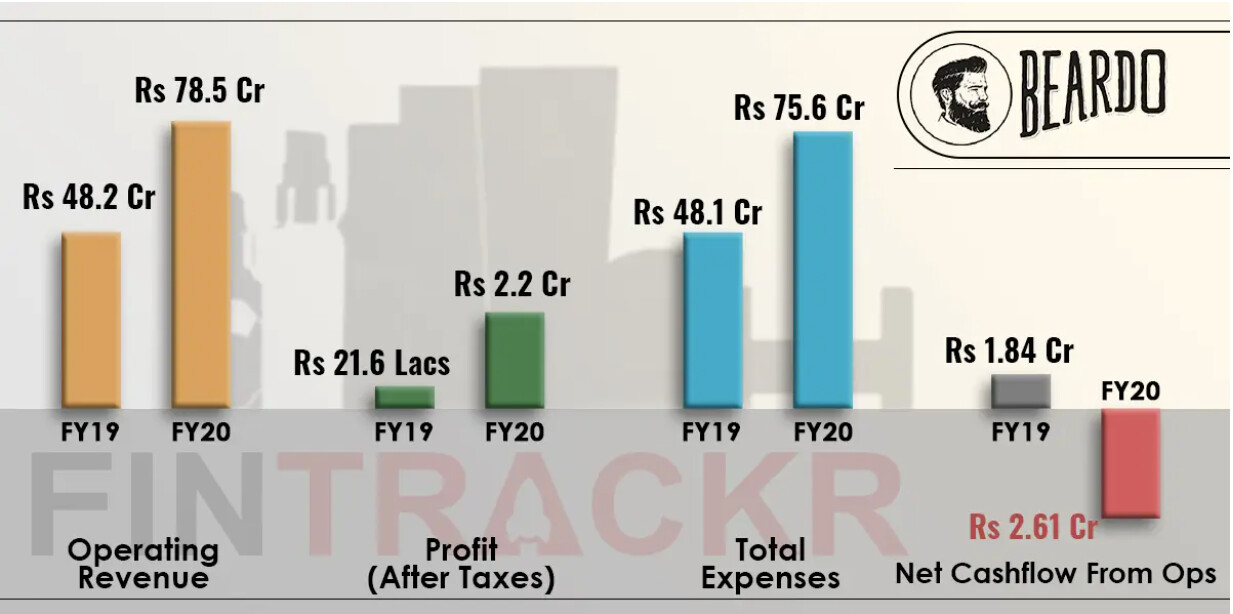

I’d wait for Marico’s latest annual report to learn more, but you can see both of these acquisitions are in the right D2C subspace. They’re purchased weekly/monthly, usually have high repeat customers, and over time have gross margins of around 60-70%.

If you wanted to understand the businesses in detail, I’d compare Beardo to the Bombay Shaving Company to understand what they’re doing differently in beard care, and compare Just Herbs to Biotique to see if they’re competing in the same price range.

At a higher order level, D2C brands are carving markets for themselves, with men’s grooming not really being a viable market ten years ago (aside from the usual shaving gels you’d see in the supermarket). Personally I see Just Herbs to be a lot more exciting than Beardo, and there’s currently a trend in the West with people promoting natural skincare, and shampoos free of sulphates. One has to think about what the addressable market could be for a Just Herbs, as Dr. Vaidya’s founder had a similar ambition to take Ayurveda global.

Here’s a snippet from Just Herbs:

Since they have Marico’s backing, the question is only if they have enough of a product range to justify an offline store. I’m sure they’ve looked at data from their online store to understand that most of their customers order from X city and have opened up a store there, but you’d have to look at the store economics if it’s there in the annual reports. Currently they have only two stores, so I’d also pay attention to see if they scale up or shut down, given Marico’s ability to command shelf space in normal supermarkets.

Here’s a really nice read that covers examples from D2C companies abroad that have opened up physical stores, and points out flaws that crop up at different points in the D2C journey:

A good example in India is Nykaa. They already have almost a hundred physical stores, and they’re planning to open up hundreds of stores in the next five years. You can read about this journey in various interviews, and we should know more through the DHRP.

I’ve covered the business cycle in detail in the D2C thread on Valuepickr, which will answer a majority of your questions. Please have a look here if you haven’t read this already.

Cheers ![]()

Disclosure: Not invested