For the benefit of anyone wanting to look at the D2C model in greater detail, I’m updating this post over time. It contains a full breakdown of the FMCG / Personal care sector, and sheds light on why RPSG has chosen these specific avenues.

It’s also worth pointing out that the RPSG fund is an extremely small fish in the VC space in the country. It has funded 7 deals in its life, compared to Sequoia that’s completed over 40 this year. This means their hit rate has to be near perfect.

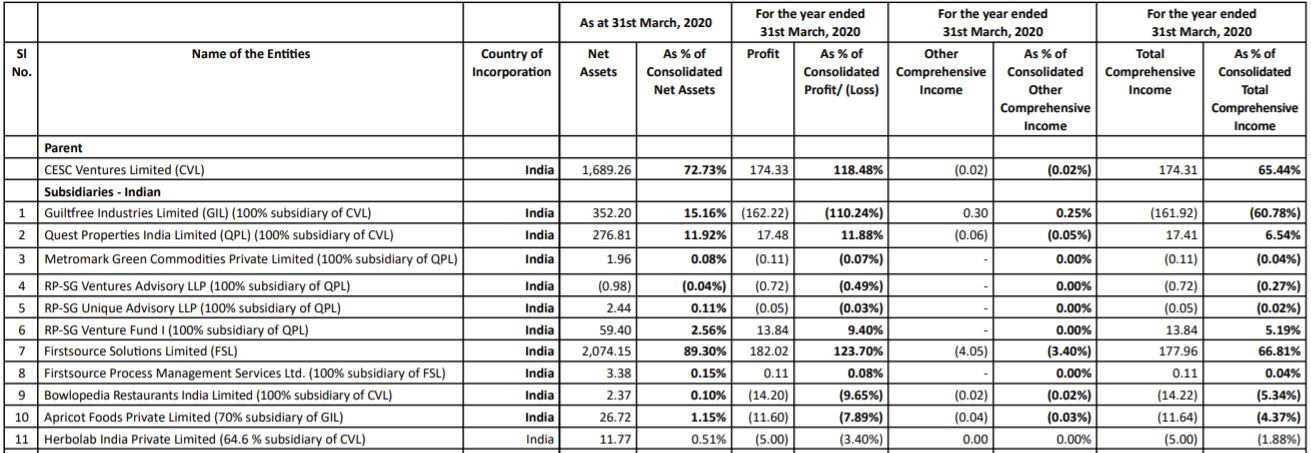

The revenue/profit for Too-Yumm, etc have been documented earlier in this thread:

What’s annoying me is that a further subset of really interesting ventures such as ShopG, mCaffeine and IncNut fall under the RPSG Venture Fund, which itself is listed as a subsidiary of the real estate subsidiary, QPL.

Which means when we look at the quarterly revenue, what really should come under FMCG would be classified under real estate. (If I’m wrong about this, please give me a shout) There isn’t a full breakup given in the quarterly reports, so we’ll have to wait for the upcoming annual report to see how they’ve fared. I’m highlighting some of my readings on a few of these ventures below.

Dr. Vaidya’s

Founded by a 24 year old, this interview tells the whole story of the company.

- Came from a family of the biggest Ayurvedic doctors in India, grandfather saw over 250 patients a day, didn’t ever charge for consultations. Difference in ambition in the family. Younger generation wanted to turn this into a business from hundreds a day to lakhs.

- Went to the US for undergrad, and saw how Yoga became a multi billion dollar industry. Why can’t we do the same with Ayurveda?

- Came back to India, worked in a fund that looked at B2C businesses like PVR, got to understand the best brands in the country and how to build a brand.

- Grandfather passed away, left behind an empty clinic, a factory in Silvassa that produced the medicines. The patients didn’t let them close the clinic, they kept it open as a dispensary, and slowly decided to turn the family legacy into Dr. Vaidya’s.

- Bootstrapped the business, focused on disruptive marketing. Started with one product → gave away 2,00,000 samples. After a year, decided the business can only run with more SKUs. Came back with 27 more SKUs (November 2017)

- Saw growth in the online / e-commerce space. Started with a few orders on the website. Wife worked at Nykaa, built their own website and took time to curate the content on the website. In November 2018, first milestone was 50 orders a day.

- Since that day, scaling and growth haven’t stopped. From 50 orders a day, they’re now at 5000 orders a day. 95% of sales are online. Saw people in Trichy, Jammu who don’t have access to doctors, but want Ayurvedic products. Where do they go to get them? 84% of our demand comes from outside Tier 1 cities. This is the real value add.

- Most important thing for us it to be close to our customers. First product was LIVITUP, an Ayurvedic hangover cure. We did customer service ourselves on Sundays, this allowed us to engage and know them. Packed thousands of orders ourselves at the office.

- The next step for us (FY22) is to improve customer experience and build more value in the chain, and scale up customer engagement. We constantly look for feedback on the products, the instagram page, etc. Want to take the company across 5 countries now, doing groundwork for this.

| Financial Year | Revenue |

|---|---|

| 2017-18 | 86,83,525 |

| 2018-19 | 2,04,17,905 |

| 2019-20 | 16,33,16,371 |

Dr. Vaidya’s success can be attributed to the family legacy, smart decision making with respect to distribution and marketing, but also the care that they put in to the brand. The big question is whether the new management changes the anatomy of success, and how this story transforms.