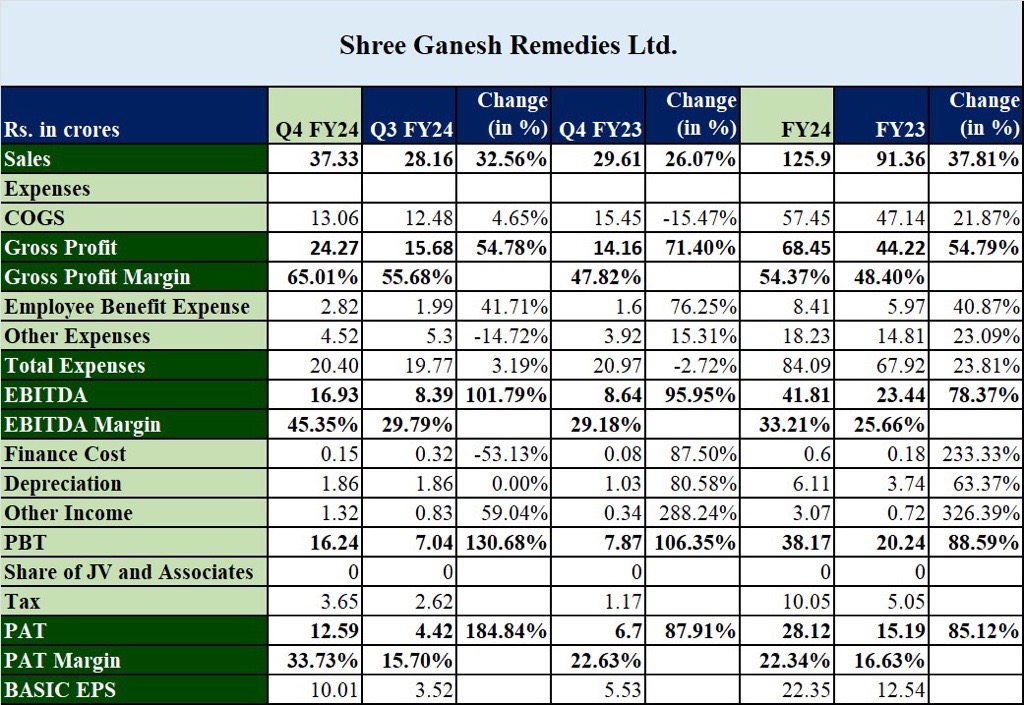

SGRL coming in with blockbuster results.

7 Likes

Hey @harsh.beria93 , For PI Industries do you think the annoucement of capacity from Chinese companies around Pyroxasulfone becomes a risk for PI ? Your inputs would be helpful as you have been tracking this one. Asking coz Pyroxasulfone fortunately/unfortunately is one of the key molecules for PI + the capacity that chinese players announced is strangely above world market demand.

5 Likes

Hi Harsh, I understand you are into research related to climate science. Also you have an excellent and unique investor mindset, thus would like pick your brain on below thought I’ve been having when investing stocks related to agri sector.

With the acceleration in climate change effects, agriculture is going to become much more complex. I anticipate major disruptions for economy like India where the farm ownership is very fragmented. But at the same time I have feeling that there is a big opportunity for innovative companies that can work closely with the farmers and can adapt their products quickly. How do you see this panning out over next few years and how it may impact stocks serving this sector like Fertilizers, pesticides etc?

8 Likes

Massive and abrupt climate change which is evident in India and across the world can have both positive and negative impact on companies producing agricultural products.

Some of the earlier assumptions while investing in such companies from long term perspective may need to be re-looked. Erratic monsoons may have impact on their earnings in earlier high earning seasons. Also these companies may have to invest more in R&D to produce new products. Companies having exposure to IoT may able to work closely with farmers and understand their needs better.

I believe this could be an area of good research for investors as well.

I may be wrong in my analysis as have no expertise in this domain.

1 Like

Hi @harsh.beria93 Do you still hold Chamanlal?? Got through my screener. Hasn’t run a lot. Showing decent return ratios along with acceptable growth. Wanted to know your rationale?