Harsh

I must say there are few conflicts which I observe in your portfolio. First I would like to compliment the way you analyze in depth the value of a given company/business. Mostly you are trying to buy mispriced bets which might be of higher value in the future. But I fail to understand why do you have more than 25 stocks in your portfolio, what is stopping you from keeping it focused to say around 10-15 stocks and you can further classify them as core/opportunistic/cyclical/value… This might help you in two ways …1. you will have less moving parts to worry about and also you will have more time to read and observe the current names. With your thesis playing out on a story you can evolve from their and replicate it elsewhere with high conviction.

Also do read about how a portfolio starts replicating a indexs performance once the constituents go north of 10-15 … I did read a long article on the same with decent size data …will share if I find it.

Regards

Divyansh

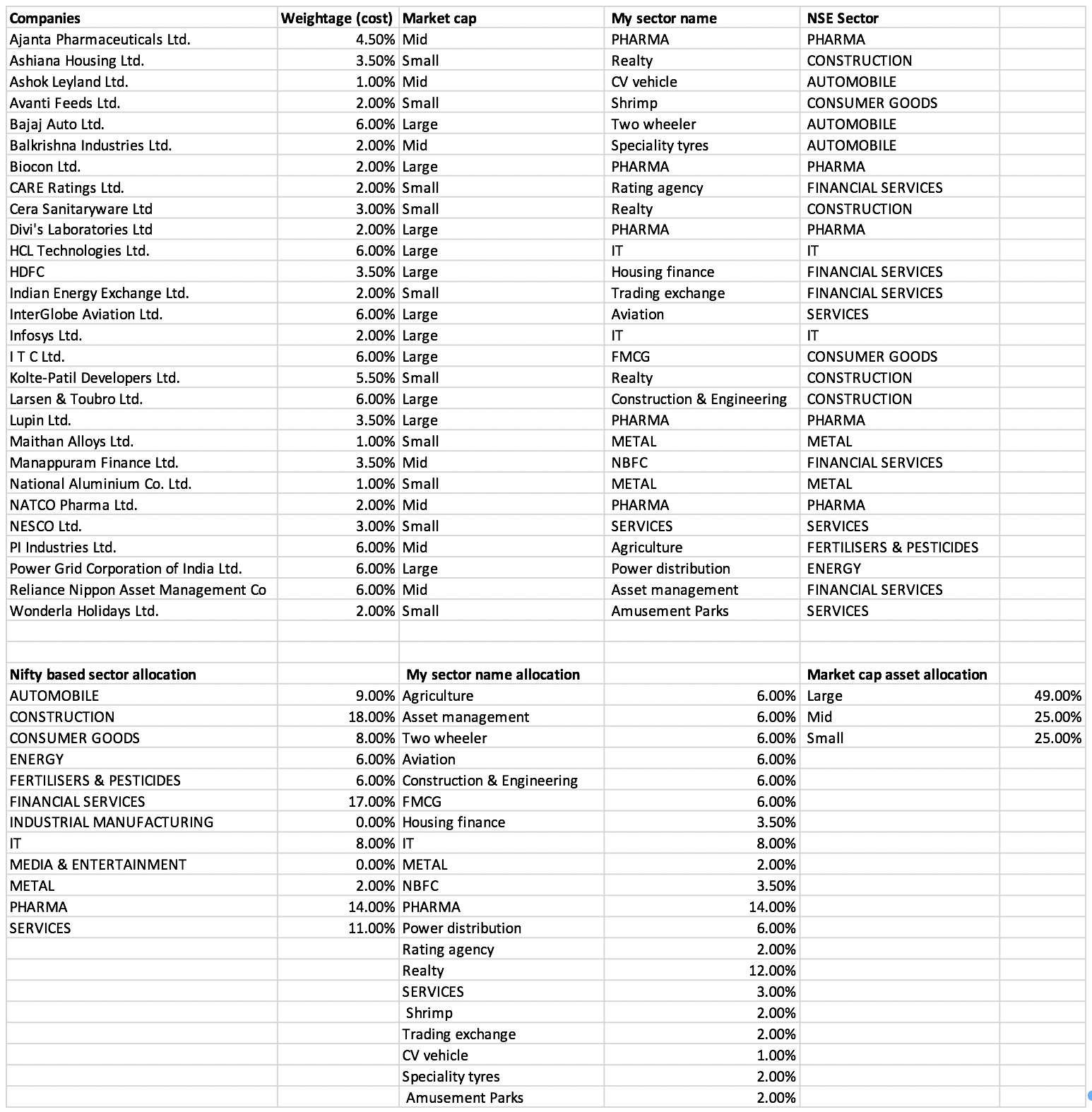

It will be very useful for me if you can tell me the conflicts that you see. I maintain a very detailed account of the kind of bet I am making (shown below). My corpus size allow me to be flexible with my investing decisions i.e. I don’t need to own only high quality businesses. I am happy with lower quality if risk-reward is in my favor.

I haven’t come across any research that shows owning a large basket of stocks leads to market performance. What you are probably referring to is the number of stocks an investor needs to have adequate diversification, which is very different from tracking error. You can have a 1000 stock portfolio and have a large tracking error from the underlying index. Past academic research have identified a few factors such as quality, company size, valuation, etc. that can help explain excess returns. In order to harness one factor, we need a large basket of stocks (atleast 100), that’s the fundamental attribute of long-short strategies that try to harness a given factor.

Coming back to reality, my thumb rule is to keep 20-30 stocks with largely diversified cashflow (geographic, industry, etc.). This provides adequate diverification and I can track them reasonably well. Plus, I will be glad if you can help me identify unidentified risks ![]()

Hi Harsh,

Keen to know what updates you’ve made in the last one month to your portfolio since the last update.

Also are you looking at any other cyclical opportunities apart from Nalco like Paper which could have a quicker turnaround?

I have made no updates to the model portfolio since the last update. There are two of my portfolio companies which are more than fairly valued (PI Industries & Divis Lab). I might bring down their weightage and increase weightage in certain other companies (details below). I will update the page once I initiate a transaction.

About the paper sector, I haven’t studied it. I have been studying metals (both ferrous and non-ferrous). At appropriate valuations, I might consider adding Sandur Manganese and/or Vedanta. Other companies which I have been studying are Syngene (which can be a replacement for PI Industries), Cochin Shipyard, INOX Leisure and Vedanta.

This is somewhat surprising. You already have 14% exposure to pharma. You already have Divi’s which is somewhat similar to Syngene (I may be wrong). PI is into Agri/speciality chemical space. Especially, agriculture/farmer/rural is the focus of the government now. Monsoon forecast seems to be good. Why are you thinking of replacing PI with Syngene?

I haven’t done it, so lets not jump guns. Syngene is a contract research organization and is not exposed to the usual vagaries of pharma. However, it is in a more regulated place compared to PI. If I had to choose between Syngene and PI as a business, I will go for PI because there is no FDA, plus the fixed asset turnover is higher for PI making it more capital efficient. However, this is also reflected in valuations, with PI trading at a large premium to syngene. Also, I may start trimming down my position in Divis (at a given price) and Syngene can be a replacement. However, given the limited listing history of Syngene, I am unable to convince myself to pay a fair price for this business. I generally like to buy a business once it has seen atleast one full market cycle to know how the manager behaves in tough times. Given that we have a long history of Biocon, I am somewhat comfortable with the management.

I cannot care less about this. I bought PI a few years back not because I had a view on monsoon or the government focus. For me, PI is a decently run business with a large tailwind of outsourcing of drug/chemical manufacturing by innovator companies to places with labor cost arbitrage. However, I also respect valuations. My general rule for a decently growing company is to start cutting positions if I cannot envisage decent returns over a 5-year period, assuming my growth assumption fructify. That’s why I might cut some positions in PI.

Thank You Harsh. I am new to investing. I asked because I am tracking Biocon, Divi’s, PI and some other pharma stocks. Booking profits and investing it in other companies which may give better return in future is an important part of investment - which comes only with experience - I guess.

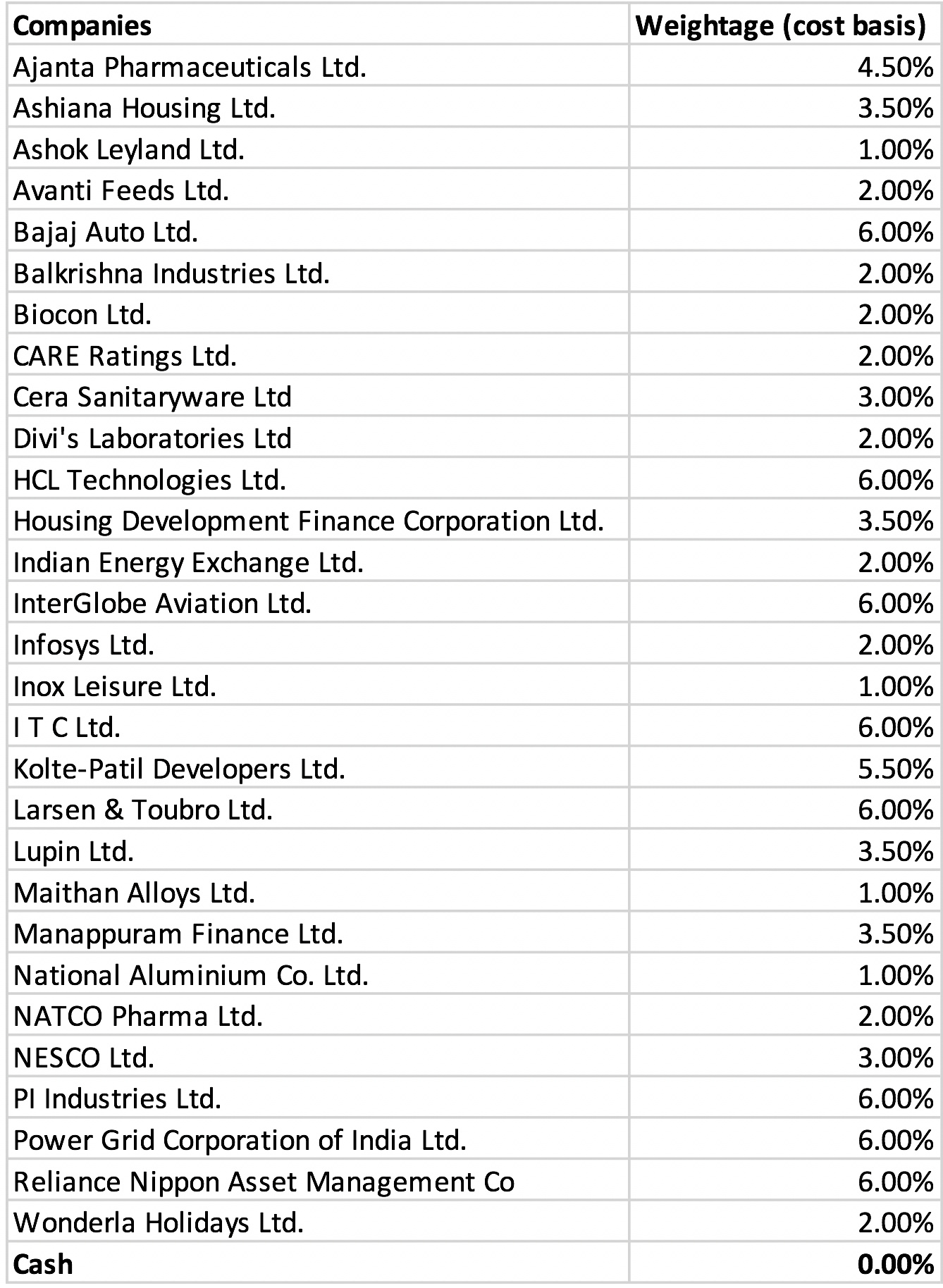

As of today, I have added 1% position in INOX Leisure which brings the cash back to zero.

Rationale:

My long term growth projections for INOX is about 15-18% over the next 5 to 7 years based on data below:

- Plan to add 830 screens to the current screen count of 574 in next 5-7 years (increase in screens: 13.6%)

- Long term ticket price increase: 4%

- Premiumization: 1-2% (based on increased contribution of F&B sales and advertising revenue)

The normalized OPM are ~14% which gives me an fair enterprise value of ~2.2 times based sales. Lets do some crystal gazing!

FY19 revenues were 1664 cr, FY20 revenues will be close to 1600 cr. (taking COVID into account), FY25 revenues at 15% CAGR ~ 3200 cr., Enterprise value ~ 7040 cr. (P/sales: 2.2, share price: 685). The current share price of 190 gives an attractive risk reward. As company is unleveraged, there is a low likelihood of bankruptcy.

Key risks:

- Rapid expansion will lead to repeated equity dilution (in my estimate the SSG ~ 12-15%, anything more than that requires dilution).

- A shift to OTT

The updated portfolio is below:

What’s your opinion of files getting directly to homes through digital or the cinema halls not being used? Hope you aware of a dispute between producers and exihibitors going on currently.

No firm opinions. The digital threat has been looming for a while, but it doesn’t seem there are too many entertainment avenues for urban people. Anyway, company reports footfalls and I will much rather look at that in a normalized scenario before coming to any conclusion.

Hi Harsh,

Is there any reason you are not looking into HDFC AMC rather than Nippon as an investment option

While Nippon group does bring some credibility, Anil Ambani run companies have fared poorly in the market wrt corp. governence .

Hdfc AMC is run by Prashant Jain , who has a great track record and name in the market

Thanks for this very useful comment, I used to own HDFC AMC a while back and sold it when its dividend yield fell below 1%. I completely agree that HDFC AMC has a stronger distribution network in terms of banking parentage, but Nippon has a stronger network in B-30 cities. Nippon has the highest retail AUM coming from B-30 cities, which is advantageous as this allows them to charge additional expense ratio. Also, this makes their book less chunkier.

Overall, AMC businesses are superior in terms of being asset light along with strong operating leverage. This comes at the cost of more cyclicality in profits. Nippon management has clearly stated that they will focus on profitable growth and gain market share in debt which is already bearing results (see slide below). Plus, they return most of the profits in terms of dividends giving a nice dividend yield (current trailing dividend yield ~ 2%). I will add back HDFC AMC to my portfolio at a given price (~1800 probably).

Thanks for pointing this out. Definitely with the recent drubbing , Nippon has entered the buy range.

But what about the management quality?

Management has changed, its Nippon not Reliance now. They are returning most of the profits as dividends, no intercorporate deposits, etc. Plus they are trying to leverage the Nippon network to provide advisory services to their international clients. Do you know something about the nippon management in terms of bad capital allocation?

Two main updates as of today:

-

I sold my 2% position in Balkrishna Industries which leaves cash of 2% in the portfolio. I bought the stock on 23th March 2020 (at around 700 level) and the stock has surprisingly re-rated very quickly. My fair value estimate was around 700 level (EV/sales of 3 times). Currently, it is trading at an EV/sales multiple of 4.5 which is on the higher side (based on past traded history). My projections for the business were 15% growth in revenues for the next 5-years which gave a fair value of 1400 in 2025. With the current stock price of 1162, the risk reward is no longer favorable, that’s why I have sold the position.

-

With the sharp re-rating in PI industries, I have sold some shares at 1600 level to bring the position size back to 6%.

The updated portfolio is below:

Nice portfolio. Ajanta results are good after a long time. What about the product pipeline?. Do you think they can sustain the growth?. Due to some reasons, they dont do con calls. We cant hear from management.

Also, I am surprised at the muted market reaction on good numbers. Usually I dont like discussing about the price movement. Recently, I started giving importance to these two events. 1. Muted or -ve response on a good result 2. Good response on a bad/average result.

Their US growth was earlier guided at 20-25% over the medium term (link), plus they keep on gaining market share in India in all their segments. In the last couple of years, they ran into roadblocks in Africa (specially the institutional business) which seems to be coming back. In essence, it seems that they are well poised for reasonable growth over the next 3 years.

Your question about ANDA pipeline: management plans to file 10-12 ANDAs and launch upto 10 products in the coming year which is what they have also been doing historically.

I am not so sure about this, prices have gone up from 1000 to 1500 since mid-March, plus their price got re-rated sometime last year (around August) when market got clarity about medium term growth prospects.

Here is a brief commentary of my actions during this market meltdown and the following meltup. For the first half of 2020, my portfolio is down by -9.53% against a nifty return of -13.8%. This is not something I am particularly proud of. The outperformance has mainly come from my pharma basket, PI industries and the new positions bought in March (details are posted in the thread above).

My reasonably large bet on pharma which made my portfolio lag in the past couple of years has started paying off . I am happy on that front. However, I also made a few blunders in March.

During the market fall, I sold out Reliance Industries at ~900. I first bought my reliance shares in February 2018 because I knew that Jio and Retail will be value unlockers in a 5 year timeframe. However, corporate governance always made me doubt my decision to hold Reliance and I finally craved into my fears at an inopportune time. This is my second biggest investing mistake so far, the other one was selling Bajaj Finserv at 4200 in 2017 and using the proceeds to buy Lupin at 1400. Bajaj went on to double from that level and Lupin halved, that was quite a nasty experience! I have been incredibly lucky to match nifty returns in the last two years despite making such horrific errors (also lost quite a bit of money in Zee and Shemaroo in the past 2 years).

Overall, I sold Reliance (6%), Mahindra Logistics (2%) and used the proceeds along with the 5% cash to buy biocon (2%), Balkrishna (2%; which was later sold because of sharp rerating), Maithan alloys (1%), Ashok Leyland (1%), Avanti (2%), INOX (1%), Wonderla (2%), NALCO (1%), 1% addition to Real-estate positions (Ashiana and Kolte).

In essence, I added to the deep cyclical part of my portfolio which might look stupid right now (eg: CV player, INOX, metal & real-estate companies, etc.) but these might play out when we go back to an economic expansion. I have started these positions at a small position size because I plan to add to it if my thesis turns out to be right.

It took me time to read through the entire history from start but very interesting thought process and thanks for sharing

Excellent details… One advice is to prune the portfolio to keep it simple and easy to track.

I always support consolidation and <10 stocks which has been picked up after proper analysis.

All the best

Note: instead of INOX , have a look at PVR as i feel its expected to go up more in 2-3 years.