Thanks for making this very valuable remark. It used to irk me as to how an amusement park can be touted as a secular growth story. I am sharing my insights from the numbers this company has generated since listing. I have to say that its a very easy company to analyze!

A few insights:

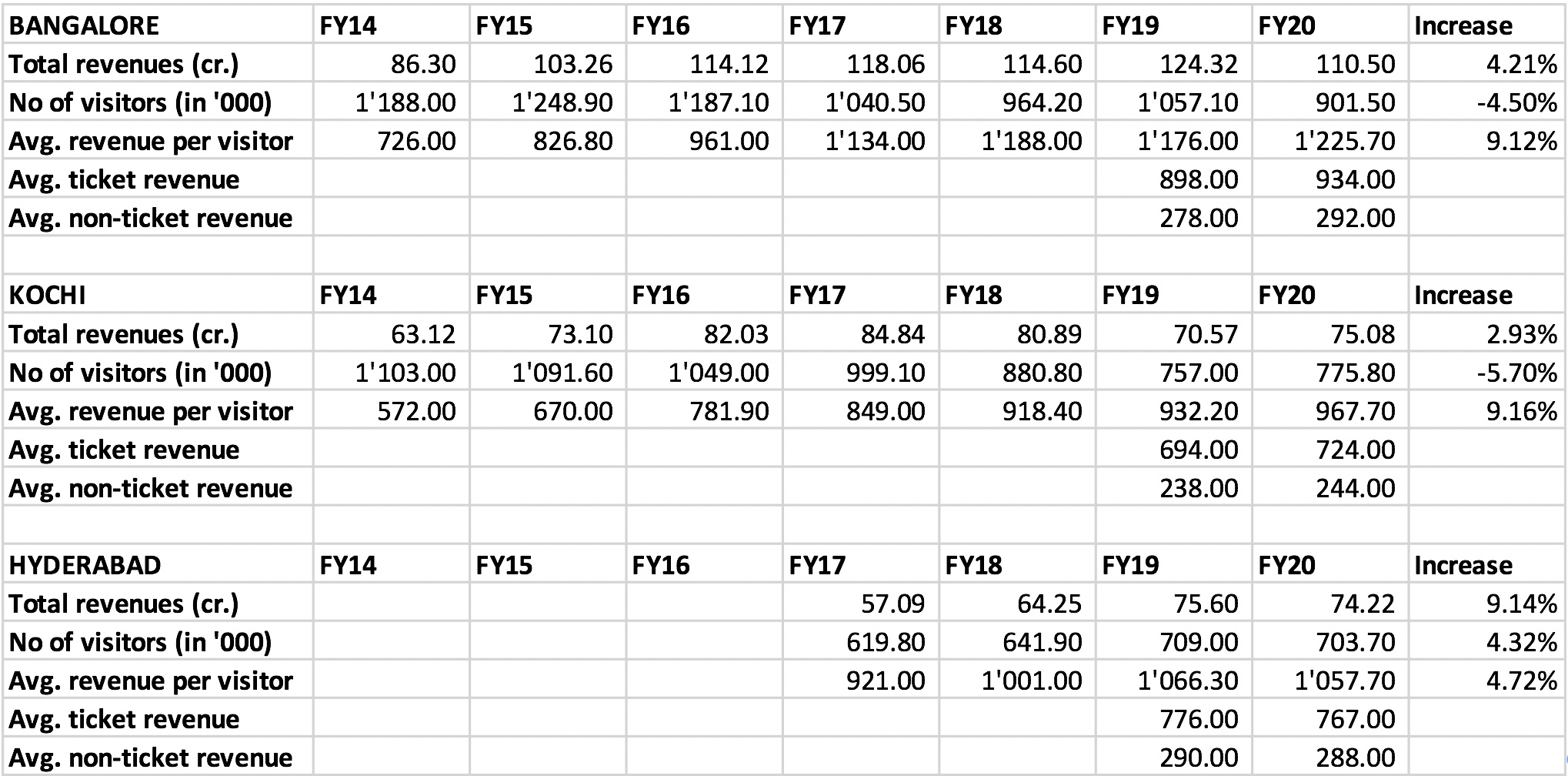

- Footfalls tend to stagnate at 10 lacs once the park is well discovered.

- Long term growth in ticketing is close to long term inflation (8-10%). In recent years, the growth in ticketing price has come down. This indicates that the company has some sort of pricing power atleast to pass on inflation to its customers.

- For a mature park, the growth in revenues will be low (4-5%), might simply cover inflation in staff prices. Mature parks make close to 100 cr. With long term PBT margin of ~33%, they should generate 25 cr. profits and should be valued at ~200-250 cr. (10-12% cost of capital).

- Growth comes from new parks. Now lets see if new parks actually generate ROE in excess of cost of capital. Hyderabad park required 250 cr. to setup and generated revenue of 75 cr. in FY19 and FY20. Lets say the sales will stabilize at ~100 cr. (PAT ~ 25 cr.), which gives a ROCE of 10%. Company can amplify their ROE by taking debt for CAPEX but its clear that ROE will not be >20%.

Seeing all of this, its clear that this is a business whose underlying ROCE is close to their cost of capital. Long term growth rates will probably be 10-12% (with 1 park being added every 3-4 years). Such a business should be valued relative to their tangible book value. In my opinion, the best time to buy these businesses is during recessions (like now) and sell it when economy is doing very well and company is trading at 3-4 times their tangible book value. These are my insights and I would love to get contrary feedback ![]()

Disclosure: Invested (detailed portfolio here)