Company is going to buy from the market. Many past instances of open market buy back did not firm up the prices. Buy back will take place over a period depending upon the supply. IMO, this may not be the escape route for DII. With the capex cycle reviving and economy is poised to pick up, Anup will do well hereon. As you said, management claim of achieving Rs 1000 cr turnover in near future is to be taken with the pinch of salt.

Very Immature comment. HDFC and Abbakus have been increasing stake. Very unlikely its for their exit.

please refer to this post.

About being priced in, the fall from 840 most likely was the bad result impact, not the buyback.Price being 8-10% up today most likely indicates that a shakeout of weaker players has happened.

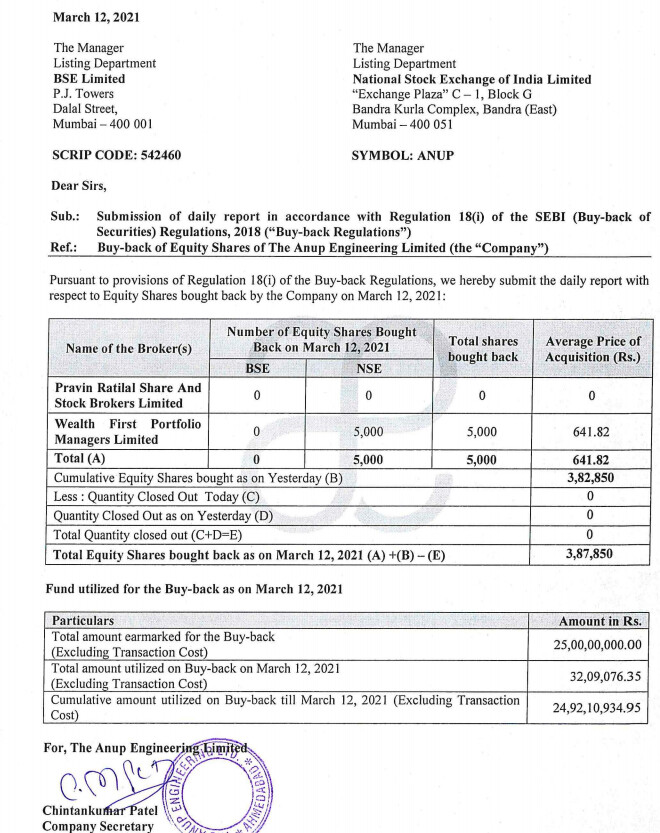

As per open buyback rules, it can go on for 6 months. price fluctuations will happen irrespective. Also as per rules, min 50% buyback has to be undertaken, in this case would be 12.5crs.

Buyback working like a charm. Accumulated most in the range of 635-645 price range. if the buying momentum continues, should cross 3.70 lakh shares buying atleast.

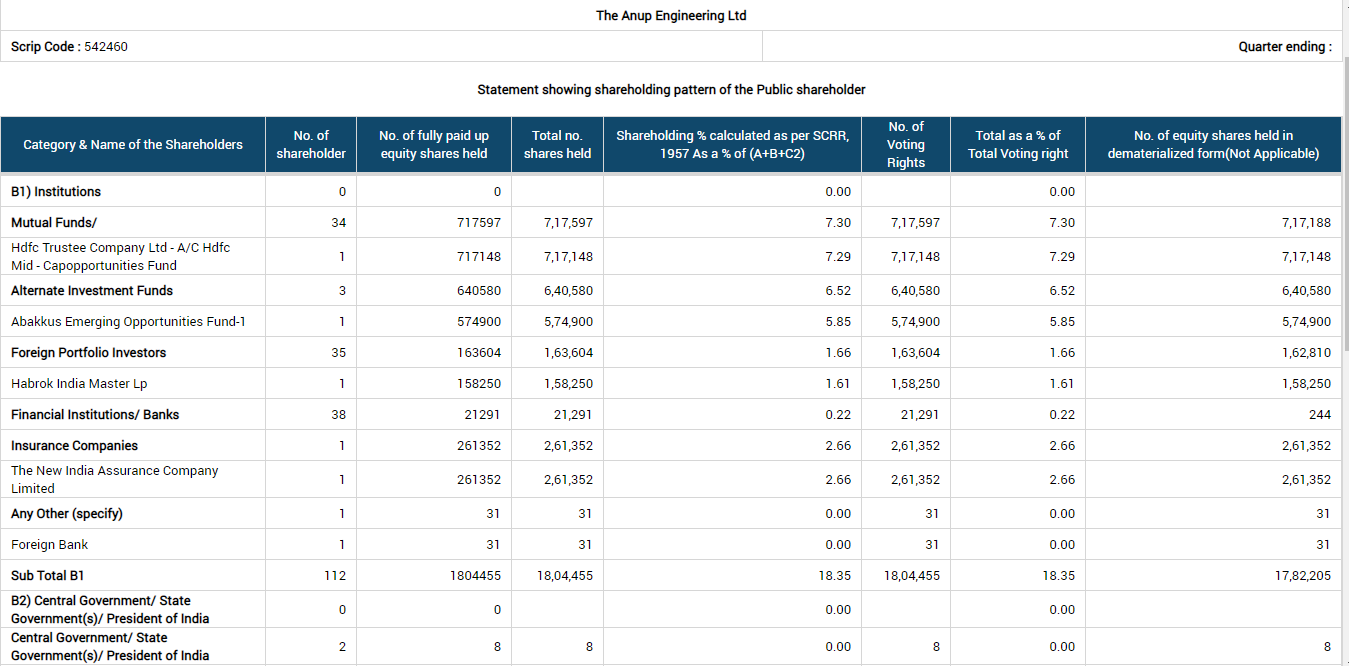

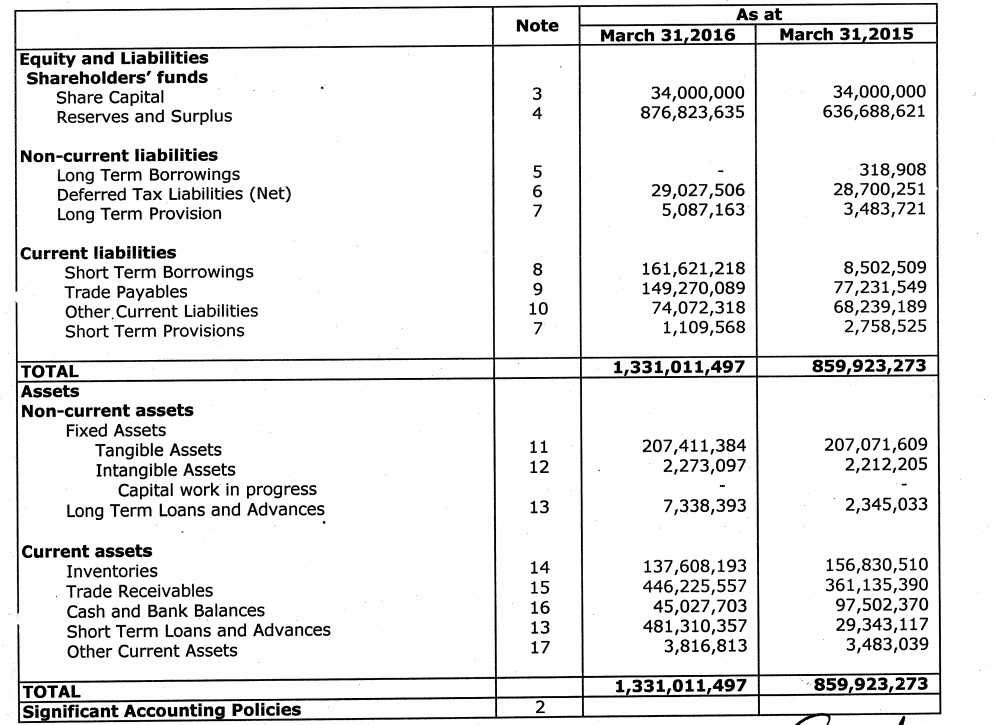

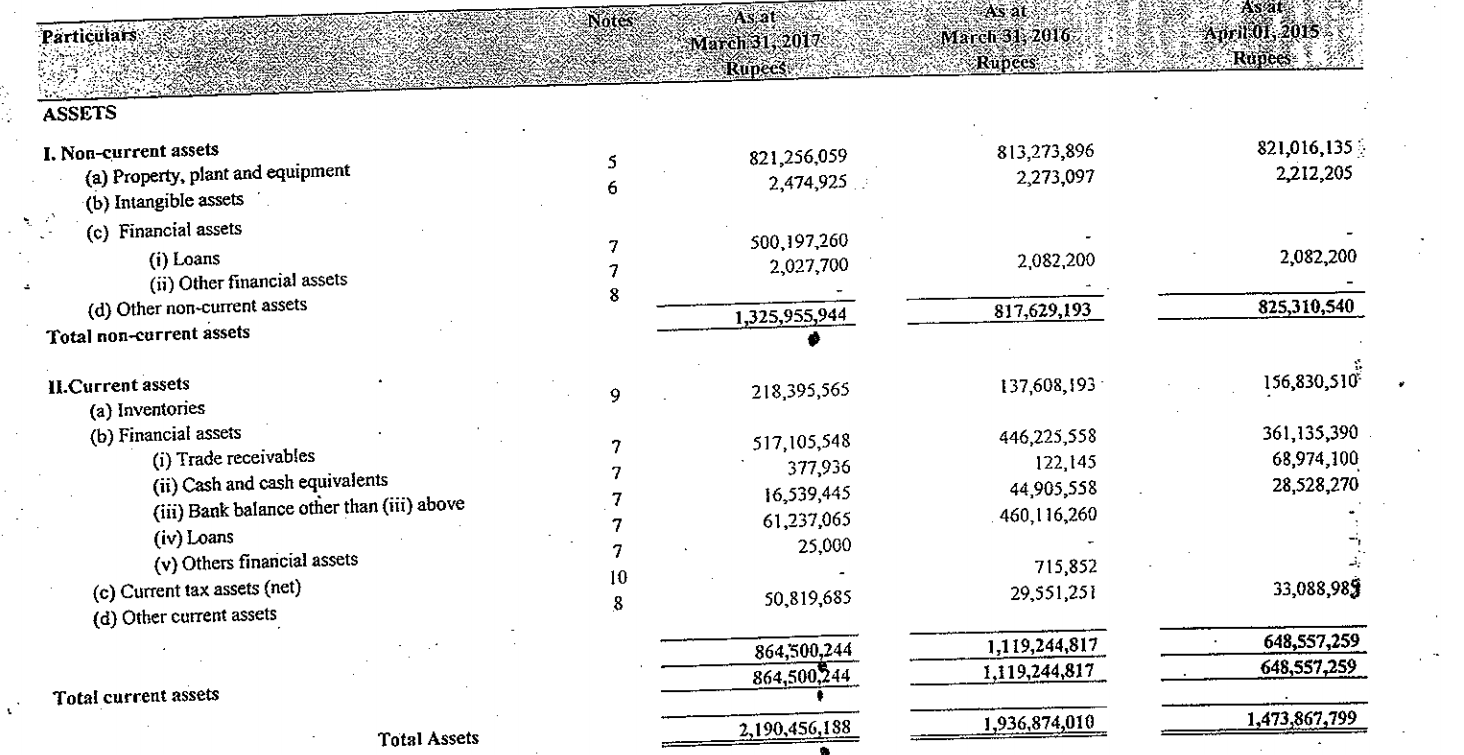

In 2016-17 there was a sudden changes in figs of balance sheet like Tangible Fixed assets increased from 20.74 crs to 82.13 crs. But if you check in the annual report the addition was just 4-5 odd crs.

In 2016-17 AR all last years figs were also changed. If it is due to IND AS then how past figs are comparable.

I am attaching screenshots of balancesheet of 2015-16 & 2016-17 .

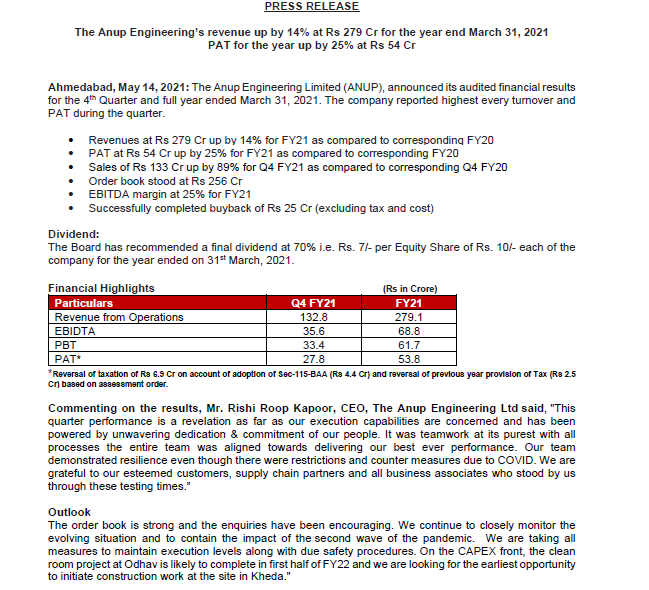

We have about INR 256 crores for the opening order book for the year. And since then, we have already booked about INR 46 crores. So that takes the number to INR 302 crore for the year.

Primarily, the order book comprises of about 14% for exports and 86% domestic. And the reason for that is pretty simple, is that the domestic demand continues to hold up, the lot of our traditional sectors doing very well.

Q4 of FY '21, has seen an exceptional performance and that performance has been actually a revolution, as far as our execution capabilities are concerned. And largely, in fact, I would say that it is completely powered by the kind of teamwork that our team demonstrated with a lot of dedication and commitment despite very, very testing times.

mentioned in the press release that the clean room would be ready in the first half. So by the end of the first half, the capacity of Odhav would be in the range of INR 500 crores to INR 550 crores revenue potential

On reaching revenue level of Rs. 500-550 cr.

going forward, the outlook has to be a little cautious because of the uncertainties which are being thrown up by the current ongoing pandemic, but I think pretty much our capacity is going to be at that level, the moment we commission our clean room. So we have all the necessary infrastructure in place for us to be able to deliver that number. So it will take maybe a couple of years before we reach the target. Maybe 2 to 3 years from now, we should be in a position to actually achieve that number.

On reaching revenue level of Rs. 1000 cr.

it’s a difficult question to answer at this moment because we have not been able to start the construction work at Kheda and to do that, we need to have a clean window where we can start and end on an interrupted fashion. Unfortunately, the way the events have stand out over the past 12, 14 months, we are not being able to get that window. the moment we get the clear window of about 6 months, 7 months, we will immediately begin the construction because for Kheda now, almost all the regulatory work are completed, all the approvals and the plans and everything is completed. It’s just about getting the work started at the site. So maybe it would be fair to say that sometime in the middle of next year, providing for uncertainties, that should be commissioned .

any impact of steel prices in margins?

See, what has happened is that we generally go for a back to back agreements and we take the orders. And typically, that’s one of the focus areas for us that as soon as we get our orders, we secure the materials. So to that extent, I think we are pretty well covered. But still, I feel this escalation has been pretty exceptional, and it might dent our margins by about 2% to 3%. So maybe about 22%, 23%, 24% would be the range.

Customer advances are 20% of order book.

We have added several new export lines in the previous year.

And also the technological product we have added, which is called EMbaffle, where we have tied up with an Italian company . And we have won the order sometime about March, April last year, and we have delivered it in the current financial year – in the previous financial year, that is FY '21. So that really opens the door for us for more such requirements. And the good part is that we are the sole kind of collaborators or sole partners for this particular technology in India .

I think the entire effort on improving the product mix will continue by adding more customers, by adding more kind of differentiated products to our manufacturing range. We have been able to add a lot of customers in the past year even in those times of – when we were just beginning the quarter, we were able to conduct virtual audits and – by global customers and we were able to successfully fare in those audits. And I think that kind of a market initiative will continue going forward.

in the coming year, I think as far as the ratio of the export order is concerned, maybe it is not going to be more than, let’s say, 20%, 22% going forward. But eventually, we would like to stabilize that 50% exports and 50% domestic. So that’s the direction in which we are working towards getting the necessary connects with our new customers in the overseas market. Fortunately, in the last 1 year or maybe 2 years, we have been working with the giant EPC companies who have the global projects across continents and across different countries. And they do have a very good and functional peer sharing model where every project, whether it is located in Australia or it is located in Canada, they are connected, and they are looking for best sourcing. And when we look at the fundamentals of this business, India is very well placed to service this – the global market. And I don’t see any reason why we cannot hit our target of 50% exports in the coming years, maybe in 2 to 3 years’ time. So that’s definitely there. And as far as the short-term or midterm opportunities are concerned, yes, there is – we have plenty of opportunities in the export market.

In Q2 our gross margins were lower. And that was perhaps mainly because of the kind of product mix that we had in that particular quarter . Barring that, if you look at the rest of the 3 quarters, it has been very much consistent.

As far as our traditional sectors are concerned, we still have – the demand is pretty much holding very well. I mean we talk about refining, and we see now the fertilizer sector is also picking up and petrochemicals. So these are the 3 traditional sectors that have been providing us with maximum opportunities. And that’s where we are not seeing any kind of a let up in terms of demand. So that is going to grow. But at the same time, we have been able to enter in a limited way in new sectors like power and chemicals and even in the water sector. So I think those are the sectors where we are looking to penetrate further and become – pick up some more substantial kind of order book from these sectors.

typically, our contracts are not coming with an escalation clause because that’s not there in the – it’s in the paring contract between our customer and the end users. So it’s not – it’s coming with a fixed price contract. There is no escalation clause there.

If you follow GMM Pfaudler as well, the management has quoted a significant demand in Heavy Engineering goods, mostly Heat Exchangers. So it’s very likely that a company like Anup, who specialises in Heat Exchangers, will benefit from this jump in demand.

Also, companies like IOC, HPCL have been planning out huge capexes, which would largely benefit Anup Engineering.

As it is a pure play on the heavy engineering segment, it is likely that a market leader, who works with a great margin will see a rise in demand, thus leading to higher profitability.

please note , we need to not look this as a red flag as there could be n number of reasons why they want to cash out …

But below sale needs to tracked with caution as Mr Rishi Roop Kapoor is CEO and would have been active member of capital allocation decision to buy back the shares which happened at 600 odd levels

Please note, there is no need to raise red flag. Rishi still owns 60k plus esops

upcoming AR should provide more insight).

Promoters have done a buyback at 640, given 7 rupees as dividend. effectively out of 54 eps, 31 has been paid back.

Rishi is just another employee cashing out a bit. He has been with the company for a decade plus and is excellent at his job, esops is a wat to incentivize him further.

yes, agree topline needs to be tracked. also the delay is capex needs to be tracked. hes gone on too long now. kheda capex.

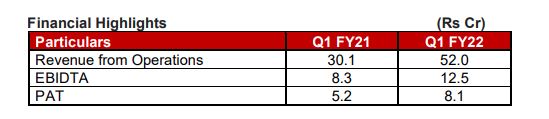

The Anup Engineering’s revenue up by 72% at Rs 52 Crores for the quarter ended

June 30, 2021 from 30.9 Cr (Y-O-Y)

*PAT for the quarter up by 55% at Rs. 8 Crores from Rs 5.1 cr (Y-O-Y)

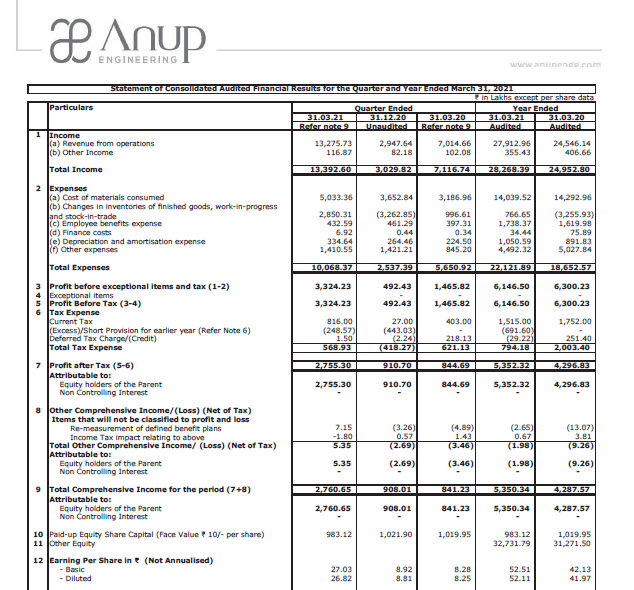

*Topline revenue for the Qtr ended Q4FY21 is 133.9 Lacs which in the management note stated as re balancing figures between the audited figures in respect of full financial

year and the published unaudited year to date figures up to the third quarter of the respective financial years which were subjected to limited review by the statutory auditors. In view of this, it may not be proper to compare Q-O-Q figures.

EBITDA margin at 24% for Q1 FY22

Order book stood at Rs 299 Crores for the first quarter. Furthermore, orders worth Rs.

51 crores were added in second quarter till date

Anup Eng Q1 concal notes:

Company recorded highest ever Q1 revenue of 52Cr with EBTDA margin at 24%

Business outlook:

Order book of 299Cr at the end of Q1.

Since beginning of 2nd Quarter company has booked another 51Crs of order and enquiries are very robust from domestic and international markets. (150cr orders are booked from the beginning of FY22.

Majority(68%) order book is from refinery, oil and gas segment.

Other sectors like chemicals (12%), power, fertilizer orders are improving.

Improving products mix, new approvals and new customers.

EBITDA margins will be maintained at 23-24% (RM impact for previous order book)

Expansion:

Odhav clean room capex will be completed by end of Q2(delayed due to covid) and from beginning of next FY it will be fully utilised. By Fy24 Odhav facility will deliver 500Cr of revenue.

Kheda facility: work to start in current quarter.

Expansion will happen in three phases over 3 years.

Each phase has revenue potential of 150cr.

First phase capex of 75cr and subsequent phases expansion cost will be less.

First phase to be commissioned in 6-7 months and full capacity utilisation will be in 6-

12 months.

Product mix will change with commissioning of Kheda facility.

Discl: tracking