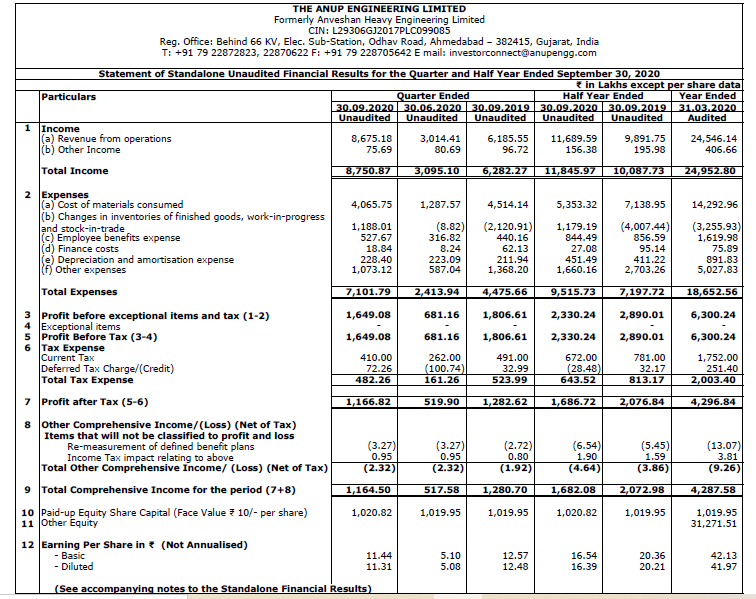

Company has announced Q2 numbers today.

Revenue at INR 86.75 Crores up by 40% quarter on quarter.

PAT at INR 11.66 crore (concerned on inventories) If negative it would have resulted in PAT of INR 22 crores. Awaiting views from learned members.

Company has announced Q2 numbers today.

Revenue at INR 86.75 Crores up by 40% quarter on quarter.

PAT at INR 11.66 crore (concerned on inventories) If negative it would have resulted in PAT of INR 22 crores. Awaiting views from learned members.

investor presentation.pdf (2.7 MB)

investor presentation on Q2 results. Strong client list is a positive sign.

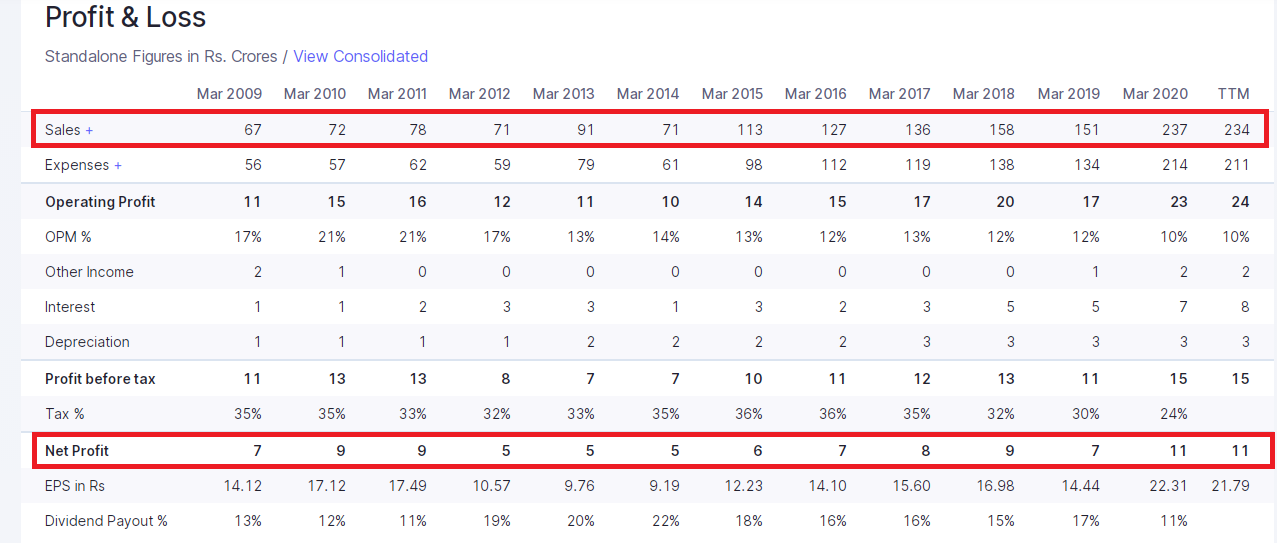

This is Patels Airtemp ( India) Ltd’s P&L

interesting thing here is revenue’s are consistently increasing but Net profits are stagnant for last 12 years.

Anup’s management guidance of revenue of 1000cr for FY2024, can we expect PAT to increase with same pace?

Why not!

being conservative, even if they manage topline of 800cr (against 1000cr as guided), and manage to do 12% PAT margins (against 15-17% last couple of years), gives you 95-96crs PAT and an EPS of 94-95.

a conservative PE of 20 times ( these companies at top of cycle and bull runs command well over 30-35 times), gives you a price of 1900 (95x20x)

being conservative all through out.

I may be wrong, but my point of view is :-

So, my views are that we need not enter into the stock by just going through rosy guidance being given by the Management.

Is 20 PE conservative for a low-tech engineering manufacturing company?

They are suppliers to like of L&T which has traded at PE of 15 in recent years and a market leader.

Does Anup has cost advantage over other competitive?

Does Anup had some technological advantage over it’s competitors?

Does Anup deliver the product faster then it’s competitor?

What is the raw material used by company? It will be great if we could talk a guy working in the industry?

Just came across the company and was interested because of below points

Revenues growth to come by with new Capex –

Customer advances funding the working capital

Net fixed assets would be more then doubled with 200 cr Capex over next 3 years

capex expected to be done completely from internal accruals

Margin pressure partially mitigated ::

Close watch

@Gaurav_Agarwal here is my take on your questions

Does Anup has cost advantage over other competitive?

Does Anup had some technological advantage over it’s competitors?

I assume yes ,coz

Does Anup deliver the product faster then it’s competitor?

— Not sure

What is the raw material used by company? It will be great if we could talk a guy working in the industry?

-----------Mild-steel as well as Stainless-steel

resource :: https://www.careratings.com/upload/CompanyFiles/PR/The%20Anup%20Engineering%20Limited-08-12-2020.pdf

Dics :: not invested

I work in Oil and Gas industry and I personally dont see any strong growth in this sector. There will be fundamental shift in the trend in this industry going forward.

@metallica.kyoto Can you please provide the justification for your thoughts? Management seems to achieve revenue of 1000 crores in next 3-4 years and pat margin of 20%. Do u think this is too ambitious in the current economic condition?

Bad Results

Poor results. Awaiting views from learned members. Looks like Management guidance of 1000 crores top line seems to be too ambitious.

@reacharjunr yes the results are bad …

but below are my considerations

Full Curfew 20th Nov 2021 10 PM to 23rd Nov 6 AM

Night Curfew phase 1 (till Dec 30th 2020)–every night from 9 pm to 6 am

Night Curfew phase 2 (From 1st Jan 2021 till JAN 30th no news after that )–every night from 9 pm to 6 am

Night curfew to continue for 15 more days in four Gujarat cities - The Hindu

I feel the pain would continue or spill over to next quarter as well based on the present quarter results …

Ans from Company — the company has taken permission to operate normally from mid of JAN 2021

major point to note

a. what are the working hours of the company does it always have night shifts

Ans from Company — manufacturing operates 24/7

b. Management should have informed the issue during the curfew time / have taken the opportunity in present investor presentation to notify about next quarter impact

then one of quarter due to curfew or external elements should not impact the long term prospectus of a company

Disc :: Invested in the company, so my view could be biased and my view points could be wrong

Board to consider buy back on 10th Feb. Glad that they are being proactive and taking advantage of the dip in the share price.

On a side note, the management should’ve been conservative while providing revenue and Capex guidance. They’ve become a textbook case of over promising and under delivering. Would request other VPs to check if the night curfew reason is genuine. I have visited their Odhav plant and it is located within Ahmedabad city limits but I am not aware whether there was any such night curfew in place during Q3 21.

Very well articulated Mr. Wagle. Indeed a good move by the management to go for buyback… 75cr + in cash reserves…

assuming even a 20-30cr share buyback @ 650 would be decent.

On your second point about execution, they HAVE TO now deliver. Qtr after Qtr, the excuses have to stop. Hopefully the worst is over and execution picks up.

About night curfew, someone has mentioned a few pointers above, in this post.

Another point, IOC ( one of their clients) is doing massive refinery capex in TN, approx 31,000crs.

Someone should try and find out if they have received any orders for this project…

@AdityaM …

Regarding the curfew i have spoken to one of the company representative and he informed me that normal operations would resume from mid of Jan …

It would great if some one could cross check and give a update

regarding the buy back the amount to used is not disclosed … but i am not very convinced for below point view

they have the 64 cr ( investments + ICD’s) money on books from Mar FY 19-20 and the stock is much cheaper before

I agree with you regarding the guidance…

Investors Please put in your view and correct me if I am wrong

Disc : Invested

25 cr buyback. 3,12,500 shares @800 - Open market buyback

This kind of open mkt acquisition will not be market cap accretive. Again buy back is not at Rs 800, but a ceiling. Company will buy at mkt rate not exceeding Rs 800.

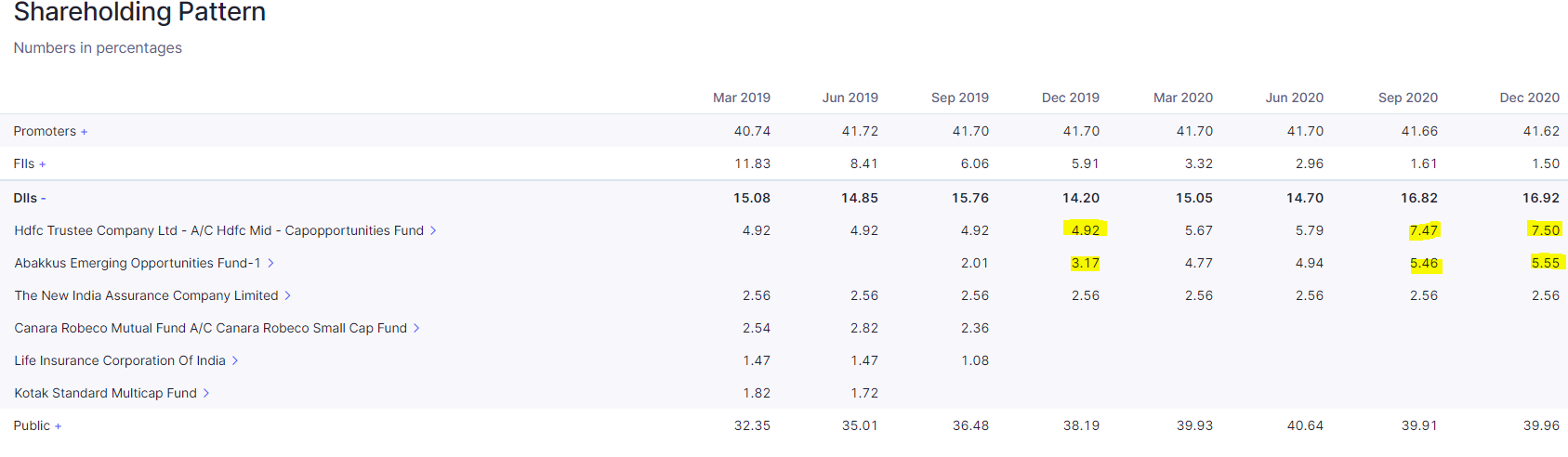

Market has discounted this buyback news. I am not sure whether they will be able to deliver the rossy guidance of 1000 crores by 2023-2024. I guess is this buyback for exit of DII’s such as HDFC and Abacus?