Results today, decent but not good enough, 20% eps growth YoY. I have sold out and bought Ugro Capital.

Disc: unqualified to advise, hence please do your own research.

Results today, decent but not good enough, 20% eps growth YoY. I have sold out and bought Ugro Capital.

Disc: unqualified to advise, hence please do your own research.

Rajesh Power- PBT grew by 34%. Higher tax meant lower OAT and EPS growth. Company reiterated 40% growth guidance for the next few years. Out of the ₹348-350 Cr receivables outstanding as of March 31, roughly ₹150 Cr was already collected by late April.

I have nothing much against Rajesh power, it’s just that my capital deployment is stretched too thin, it is still on my watch list. Something has to go out before buying new ones. Ugro trading near April 2020 lows just seems like a better option.

Sold out EFC and blue jet, bought aeroflex enterprises and bhagyanagar, aeroflex enterprises is the cheaper version of aeroflex industries.

EFC has done big equity dilution in favor of promotors, which is fraud towards other shareholders, even though it’s quite cheap now.

Blue jet has started to expand but it’s time consuming process, maybe 2 years or more, expansion is 3x, but again promotor is not quite transparent. I don’t like CDMO business because several are prone to be lumpy.

Aeroflex enterprises owns aeroflex industries, but is cheaper due to holding company discount, the subsidiary is getting orders for data center cooling hardware. Aeroflex profit is bit unclear, so better to buy cheap, the product used for cooling is not a big part of their revenues currently, need to see how big it gets. Liquid cooling is more of an AI requirement than for general purpose data center. The whole AI theme is itself in a frenzy. Aeroflex enterprises has other business like compressors, finance, plastic and venture funds, mostly doing OK.

Bhagyanagar is copper recycler, issues due to Iran war and copper ore in general is causing shortage of copper and there are new regulations to enforce recycling by copper users, though quite slowly. Iran war has caused sulphuric acid shortage, used in copper ore refining, apparently oil and gas production by product. Bhagyanagar still doesn’t have any concrete expansion plan just a 20% target and in spite of also manufacturing copper products, has low margins, and high debt, low cash levels. Demerging real estate part should be a positive outcome. Also hopefully the targeted fund raising is done sooner than later.

Thanks for much information by @RocketMan (also for Kalyani cast).

Disclosure: None of the above is investment advice, I am not a registered financial advisor, please do your own due diligence before investing

Why would you go for holding company when all the juice is in data center boom? Do you think they can monetize the shareholding somehow?

Not much change in overall status, XIRR improved little bit as folio rose post march end sell-off and mostly decent results season.

I have moved little less than 15% of folio value to US market, just following an AI megatrend. Randomly buying the host of well known names like Micron, SanDisk, Soxx etf, kospi etf, bloom, wdc, nvidia, Google, Broadcom, Coherent, etc nothing great. Quite risky overall due to elevated rupee, nasdaq and stock valuations. Plus the TCS paid added to the expense by way of temporary outflow of funds. I guess it’s all done for now.

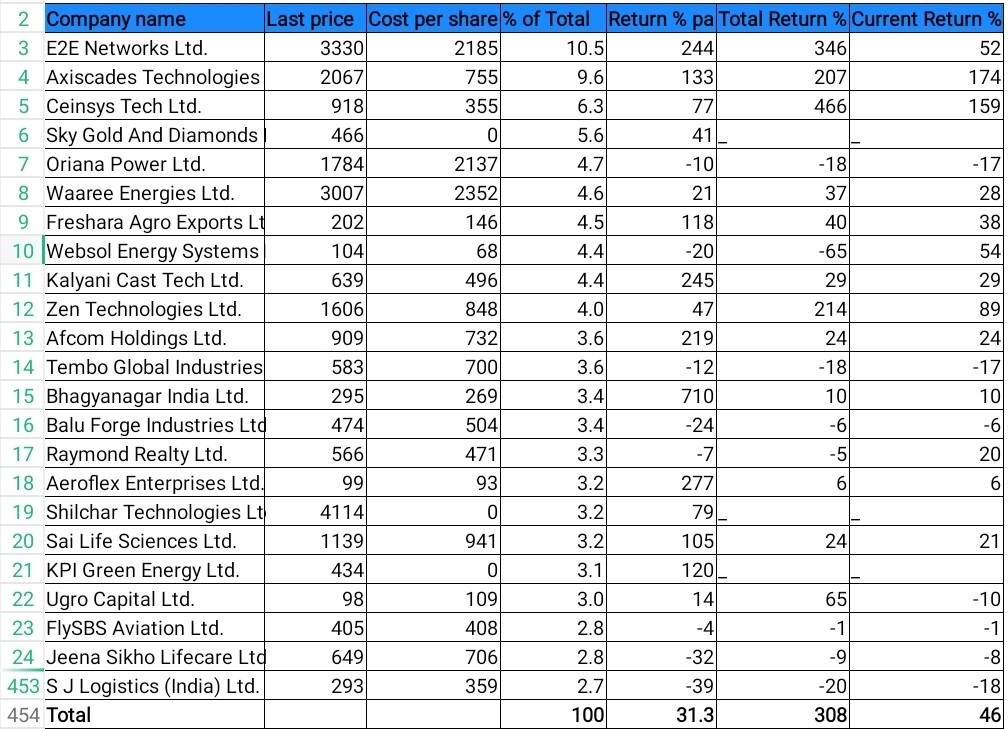

Mainly reduced from the big ones like KPI green, Shilchar, Ceinsys, Sky gold etc in that order.

Current folio status

Disclosure: None of the above is investment advice, I am not a registered financial advisor, please do your own due diligence before investing

Good to see much needed global diversification.

I used to also think about global S&P500 and NASDAQ100 index investing during corrections in 2020, but was unable to understand valuations at that time. Over a period, I have realized that, there are two main big markets in the world i.e. USA and China. These two nations have been leading some path breaking research and it is quite natural that, their market have created reasonable wealth for their investors.

It will take massive efforts from here to go back to 15%-16% NIFTY CAGR from here (2002-2010-2014 days) and it may need substantial time for that.

After reading through various high quality articles on Internet, it is worth while to see the future market trends, Per Capita GDP growth of various countries and align your investment portfolio accordingly. As per article in LOKSATTA (Indian Express Group) today, India is 16th in the rank as per Per Capita GDP growth, way behind many nations.

Though some geographies may have high valuations and some may have low, but the point is that, looking much beyond short term noise is very important. Which are the leaders over next 10-20 years in terms of innovation ? Which business themes will create huge wealth for next decade ? Which are those themes ? Which countries will lead pharma innovations ? Once we have answers for this then we may have to fine tune our investments accordingly.

I may or may not have Global investments from time to time, but believe in Global diversification as I do not personally understand Gold/Silver ETF much.Ideally, for any investor, earning good CAGR is important rather than opportunity cost of not investing in any market (global or local).

@vikas_sinha what are your views about mediocre earnings from axiscade, oriana power and kalyani castec? Are you holding or selling?

Axiscades I am not doing much, just trim by 10% for some cash or alternative investment, not possible currently due to circuit issue, mostly I am trusting their process.

Oriana I have reduced by 40% after slight loss sticking around for almost 2 years, it is similar to my action with KPI green, overall solar theme has been reduced, especially the EPC ones.

Kalyani cast I have reduced by 15%, it is just a time taking endeavour that they have set out for, may be nothing great materialises in this year, but CMAS may be a significant factor.

Disclosure: None of the above is investment advice, I am not a registered financial advisor, please do your own due diligence before investing.

@vikas_sinha wanted to know your views on soxx etf. Even after the current run what made you add it? Are you looking at it from a long term perspective or momentum play?

Secondly, did you by any chance compare SMH and SOXX? any specific reason for choosing SOXX?

I think it was suggested by stockanalysis.com or indmoney while searching for the usual semiconductor companies. Since I was randomly buying several anyway, it looked like a good basket. I would prefer it over SMH, which I hadn’t looked at yet. Performance wise SOXX has slight edge.

Sold out Aeroflex enterprises, it was not tracking Aeroflex industries, anyway I also own Vertiv in dollars. Bought prizor viztech, it’s mainly a cctv manufacturing company. It’s relatively recently launched business, they have opportunity to replace Chinese brands banned from India, cctv now need certification to ensure no Chinese parts are used. They have increased capacity greatly, is SME. Sarkari cctv have to be replaced by non Chinese. Prizor faces risk of competition from several brands, it’s not that difficult to outsource chips from Taiwan etc or even get Indian contract manufacture done for the Chinese brands.

Sold out Jeena sikho and instead bought Trishakti industries, they are crane leasing business, family business was reorganised and they claim to have lot of orders since they were in the business for long time, the reorganisation was bit delayed due to covid. They have invested a lot to increase capacity. The risk with trishakti is that it is asset heavy business though returns can be good, infrastructure growth dependency is there.

Disclosure: None of the above is investment advice, I am not a registered financial advisor, please do your own due diligence before investing.

What about the cash flows, while Aditya (CPPLUS) caters to Govt orders do you think a SME company will be able to manage the long working capital cycle from Govt orders effectively?

Funny story, I met the promoter on a flight to Mumbai. Had tweeted on the same that day : https://x.com/prudent_invstor/status/1975415094713766066?s=46

Just see their way of funding these assets is not very clean. Better move to Vision Infra in the same segment.

Cpplus has zoomed up a lot, risk-reward is as per personal preferences and I am more confident in prizor. As well established player, Cpplus naturally is handling government order well. But there’s lot of examples in the SME size range, who are active in government orders like the railways businesses such as Kavach tenders etc. Capital is getting stretched for prizor, it’s definitely a point of risk for the thesis. Thanks for pointing out!

Yes, I see in the sole post on the topic that they own something like minimum 60% of the operational assets. Finding it bit strange about the financial structure behind it. Need to dig deeper, but not sure if it is a flaw regardless. Thanks for the interesting tip, added to the watchlist!

From concall what they have mentioned is they have tie up with OEM financing for 2 years at lower rates around 5%. Post 2 year it will be transferred to Banks. That could be the moat v/s peers. As they generate 24% annually (2.2% net yield /month)on operating the asset.