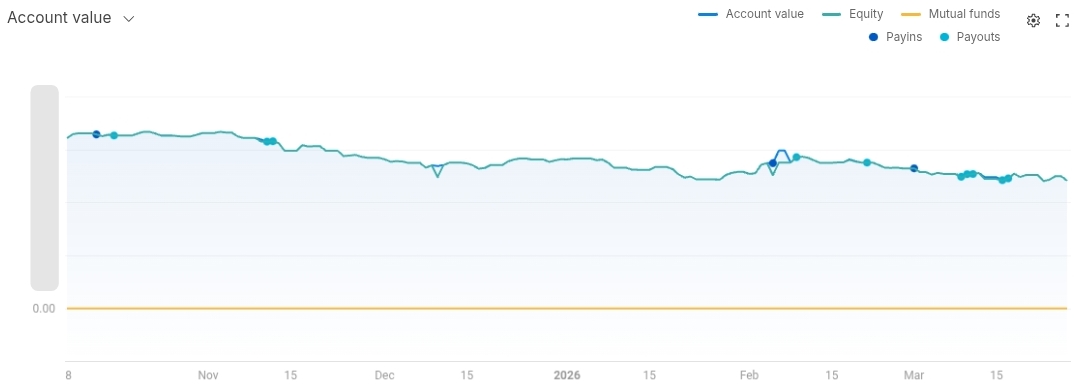

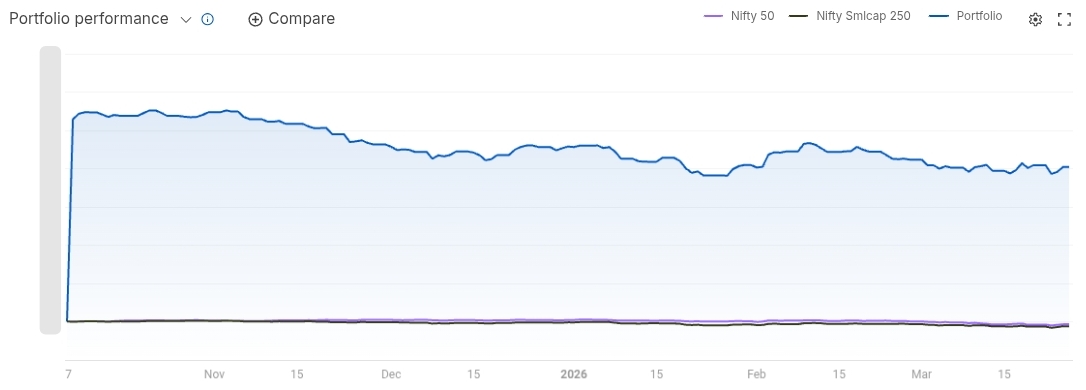

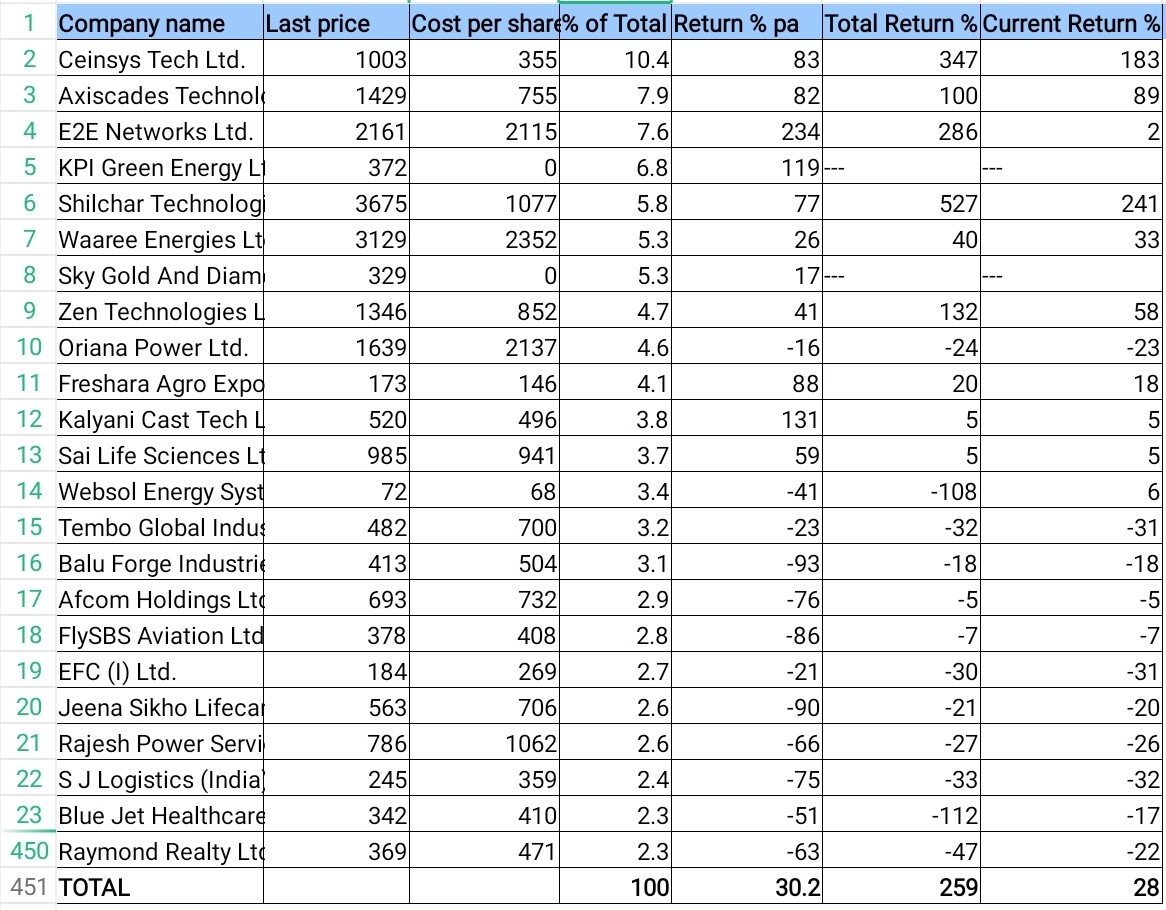

The current list is a product of the prolonged correction. Some of the biggest holdings faced issues. Ceinsys was hit by JJM corruption related panic and perhaps AI related issues too. Around 25% of folio was solar focused, there the decadal theme started to turn sour. Zen couldn’t keep up to targets even though defence was booming. Shilchar exports dampening and wait for growth was slow. E2E was also progressing slowly.

The overall market correction provided many alternatives, hence the churn in past month. I simply don’t have the depth to build outsized positions, like the ones listed above (only Axiscades kept positively surprising, even then a little pruning is prudent). So, I started spreading the risk, going from 17 to 23 stocks.

It started with the trigger of special situation in Raymond realty. Then Rajesh power, because solar etc required grid capacity (even though the basic issue is minimum base load factor of old coal generation is ~60%, not flexible enough to give room to solar peak output). S J Logistics simply because it was cheap. So, my thought process was to look at high growth and cheap stuff. Freshara was somehow down even after news of acquisition, perhaps lucky here, time will tell.

An exception to the trend was Sai life sciences, strong business with high valuation. Perhaps Balu forge, Kalyani cast and Jeena sikho are not explicitly cheap but then the SME discount is a factor too.

I see the situation as a great buying opportunity, great business still have higher valuation, but they are not my choice actually.

I even doubled down to buying the same business twins in the Afcom and FlySBS. So, most of my buying, churning is done, even though it’s a literal feast in the markets. I don’t want to be spread too thin.

Trying to make sense of what I see, valuation is still not in momentum zone for a strong rally. I estimate another year’s stagnation. All stocks are not alike and the current crisis may impact international logistics shipping and aviation, perhaps worse than others. I am willing to buy lower quality, trying for higher returns with higher risk. Hence position sizing is relatively small to manage losses.

My belief is that small cap are in a better position than in the past, SME listings have provided good opportunity to pick some good ones. Patience may be required and short term crisis may arise. As a famous investor said, something along the lines of: regardless of market conditions etc, keep focus on business earnings growth.