Sir is it PB ratio on which you are saying that RBL is cheaper comparison to IDFCFB or any other parameter sir?

Correct, PE is more or less comparable. IDFCF has bit higher weight than RBL in folio.

1 Like

UPDATE:

Sold off Pix, bought Affle instead

Pix is at little below fair value, as stated before, was looking at 900-1000 target and kept selling off. Capex cycle will only give growth like Fairchem. Re-rating is definitely on the cards but that may wait for another cycle.

Affle is growing strongly via buy-outs, consensus broker targets provide 50% growth, bit better than Pix, and wanted to buy a “hot” sector ![]() Big majority of ad spend is digital and ad market will grow with post-corona biz growth, this is a decently competitive ‘desi’ roots international company, currently at a relative discount to past 2 year trend.

Big majority of ad spend is digital and ad market will grow with post-corona biz growth, this is a decently competitive ‘desi’ roots international company, currently at a relative discount to past 2 year trend.

Pix provided valuation comfort whereas Affle has risk of earnings disappointment. So, yes, this is a higher risk:reward tradeoff.

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

10 Likes

UPDATE:

Exited Optiemus infracom, bought MK Exim instead. Optiemus will need to grow >20x and that will take time and is risky. MK Exim is importer/distributor for some cosmetic brands which are used in salons, this is their new biz, used to be a clothing maker/trader, post-corona this new biz should grow faster. There is very little visibility into the workings of this micro cap, hence big risk. Must thank @msandip for whatever little I know. ![]()

Optiemus may fail to meet PLI targets, the biz can be very competitive and macros may become headwinds. It was my smallest position.

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

2 Likes

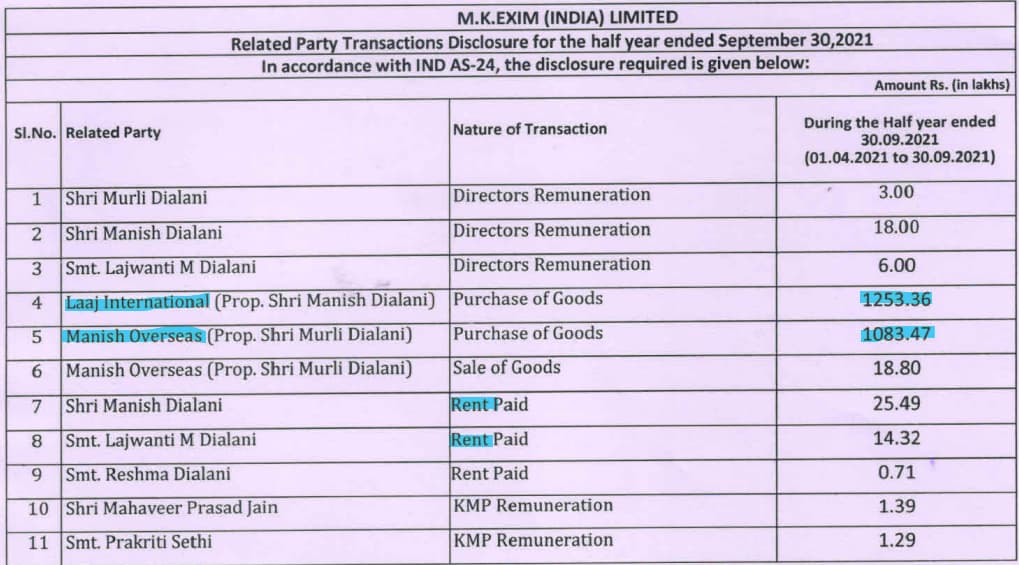

MK Exim seems to have 22 crores of related party purchase of goods in 6 months from 1.04.2021 to 30.09.2021 as reported in the exchanges . What do you think about it ? It is almost 22 crores out of 32.99 crores of sales i.e 66.66% related party purchase from promoters

3 Likes

Thanks! I followed this up, and one seems to be textile exporter and the other is cosmetics importer. Lets say this is a given risk with the small lala type firms, like there is no profit sharing via dividends yet. Promise of growth may override such risks, if growth is fast enough. BS is quite light and the distributorship needs no slow and heavy capex.

1 Like

UPDATE:

Sold off KPR, bought APL apollo, no good reason ![]()

APL apollo is merging to become bigger with Apollo tricoat, should happen soon since has been a year since plan was announced. They have been hit by steel price rise, so margins are lower, bet is on better margins, like a hedge against GPIL and Sandur. These guys are now owning 50% of indian structural steel market, they buy 10% of hot-rolled steel produced in india and have been setting up factories at points of sale.

The point is KPR will do well, but dependent on cotton cycle, margins may fall, india tried to stop cotton exports and encourage imports but people say it is too late and season is over. Like Pix this is may be bad call, but I do not want to spread too thin, so an entry means an exit also.

APL keeps doing continuous capex, while KPR is doing in piecemeal fashion, KPR claims china+1 means india will get demand, not sure after bangladesh’s leap over indian gdp. Bet is on faster growth and better margins

Sold little of RACL and Laurus, also tiny bit of Tips, added a tiny bit to MK Exim

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

10 Likes

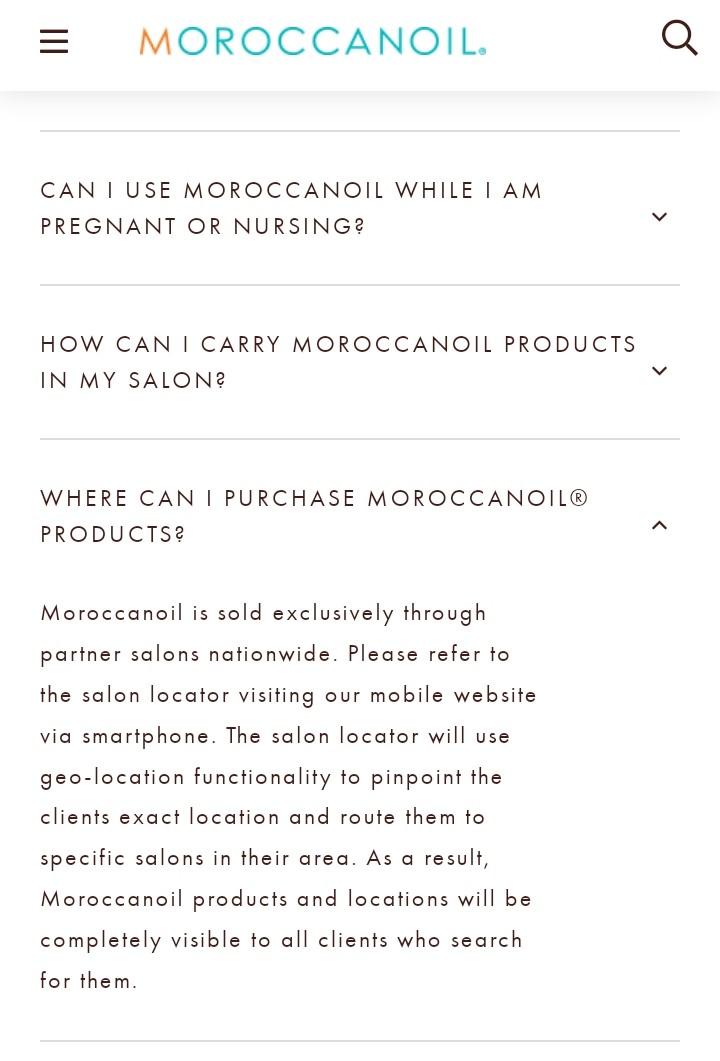

One of the salon products they claim to distribute is Moroccan Oil products .Moroccan oils site says their products are available only in partner salons and chosen retailers only.

Why would they need distributors if they sell via partner salons only(list is in the site).

Indeed it is available in Nykaa and Amazon etc but in amazon the seller name is different .Atleast it seems there is no exclusivity to the distributorship.

1 Like

The distributor is the channel partner who stocks the salons. The address somewhat matches one of the businesses owned by promotors. (Manish overseas)

2 Likes

There is quite a strong fundamental risk in distribution companies - and that is that these distribution agreements (especially exclusive ones) are often subject to performance linked renewals in short term time periods (like 3-5 years etc). Often, the entire franchise businesses hinges quite a bit on these agreements.

Whenever there is a down turn in the business or things do not work out or even to look more ambitious at times, the teams from the franchise brand side often have an easy scapegoat in terms of distribution strength - that the distributor is not right and it’s not that difficult to change if a brand has developed reasonable traction.

On the other hand I don’t think the above point is much of a worry, even if they have a distributor, a website is a customer facing interface and it makes sense to point out the salons to the customers and not direct them to the distributor. The distributor would probably be supplying to these chains and getting a margin in return.

Discl : Studied company as better half was using the product and likes it. But did not go ahead and invest basis above 1st concern + other business mix in the company. Not invested or tracking anymore

1 Like

Oh…I missed that section somehow. I had assumed that the company should be able to ship the products to the salons easily using logistics providers since all the endpoints are known and the size of shipment should not be large .For other FMCG companies (say for ITC ),distributors are a must because they do not know the roadside shops themselves.

Anyhow this point is moot since obviously they have a distributor .

I also was looking at this company a few weeks ago but just like Sumayaa and Ad-shop e-retail , their odd mix of business ventures and relative difficulty in doing indepth checks put me off.

Sinha sahib , I am a big fan and a keen follower of your updates. Just wanted to ask your view on how about coming into 50% cash if one feels that either amajor correction or a bear-market is coming ! The way US markets are cracking structurally, it seems we might also see major downside in coming days !

Correction is definitely due but don’t think there it will be more than 10-15%. That may not be significant enough to think of timing the markets. To begin with my bias is mostly to stay invested. The ideas of long-term compounders and good fundamental high-conviction picks should be enough to ride out the rough patches.

Personally my long-term is tax-free from the losses I’m carrying, so selling my mostly short-term gains is not at all wise at this point. So, I have not thought much about this situation.

2 Likes

UPDATE:

Though there might have been no great need to do tweaking, have sold off Tips today and bought in decreasing order IDFCF, RBL, Krsnaa, MK Exim, Ujjivan Fin, Kilpest, APL apollo, Affle, SSWL, Globus. Given that Tips guidance may not make stock move for another year and financials seem quite cheap, also wanted to reduce total holdings hence increase holding weight.

All of these are mostly around or still below their average buy prices.

Tips was celebrating 1st anniversary and hence tax-free. Already got message from CDSL about credit of Tips Films shares yesterday.

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

3 Likes

Long term capital gain is @10%. Am I missing something?

Yes, but due to accumulated losses, I have long-term variety only and quite large. This is forcing me to, at least as per tax definition, think “long-term”.

5 Likes

Hi @vikas_sinha - How do you see the impact of heightened competition/disruption in diagnostic sector on Krsnaa

Below snippet from the article

Tata 1mg’s disruption in the sector with a launch of B2C (Business to Consumer) segment. The company on a pilot basis in Bengaluru has launched crucial tests like Thyroid Profile, Liver Function, Lipid Profile, and Diabetes Screening at Rs 100 per test.

1 Like

Least bothered, very good details here.

If 1mg want to play a price-war then they should also really enter the govt tender biz. It gives them assured long-term contracts with volumes and price escalations built-in.

A price-war is the best scenario for Krsnaa, since they have demonstrated proof of running the cheapest diagnostics very profitably for a long time. It may hurt margins a little when they start trying to scale to B2C model as well. Though it may also help overall in positioning of cheap tests as being reliable.

4 Likes

Dear Vikas,

Any thoughts on Time Technoplast and the Tesla deal?

Thanks

Anto

This is some other Tesla and not the famous one, and it seems like any ordinary battery maker. Anyway Time techno wanted to get rid of the battery related biz. This order for 100 Cr hardly moves the needle for a 3700 Cr turnover company.

2 Likes