UPDATE:

Medium churn of folio given opportunities provided in the fall.

Total transaction worth 15% of folio value

Sold off Marksans, Vipul organics, Meghmani organics and Bajaj health, also trimmed several holdings a little bit.

Bought Mirza, Krsnaa, Sapphire and Ujjivan financial.

Reasoning:

Better to buy good, well-discovered, long running biz at a decent price and get peace of mind, even if there is short-term issue, so shoes, pizza, bank etc.

Sell

Vipul organics was facing issues due to exports related problems, cannot put a timeline on resolution. Anyway utilization is 65% and valuation is expensive. Nobody is tracking this, all this info is thanks to @kalpesh4430

Meghmani organics is expanding relatively slowly, max 50% in 2 years, valuations provide comfort but are historically permanently de-rated due to lack of ‘sanskari’ promotors.

Marksans/Bajaj health does not inspire much confidence, as stated before, covid elevated profits of most pharma and it will be difficult to match unless there are growth plans underway already.

Now, Laurus and Kopran are my only pharma holdings.

Buy

Mirza is splitting leather and non-leather biz, latter is fast growing and money making while the former is lossy, it is very cheap for a profitable shoes and fashion retail brand. Maybe bit late entry as always. Thanks @sahil_vi for tremendous details! Also for Kilpest! Thanks to @msandip too.

Ujjivan financial will merge with Ujjivan bank and hence should gain from price arbitrage, and if the bank gets back to decent profits then the upside is ~3x. Thanks @amey153 @KP2018

Krsnaa is amazing diagnostics chain, mainly out-sourced biz for hospitals and just got contract for 10 districts from UP govt, for a decade, Krsnaa is the only listed player tendering for govt. Thanks @Chins @Dev_S

Sapphire has decent metrics and cheaper than exact direct competitor Devyani by 50%. Thanks @Vivek_6954

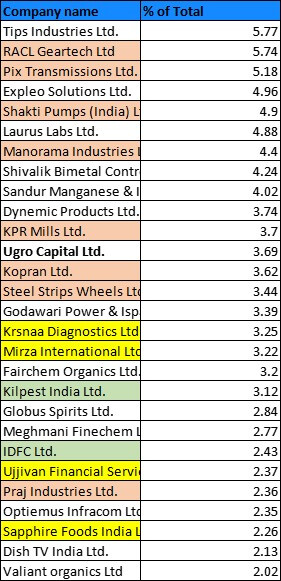

Overall folio status:

Reduced from the red-colored ones and added to the other colored ones.

Reduction in decreasing order Shakti, Pix, Manorama, Steel strips, RACL, Kopran, KPR and Praj.

Better to book some profits, even if some look like long-term bets, when seen at fair valuation and upside seems to be taking fairly longish time.

Gains are a time value function, very rare to have the foresight and patience to wait for it.

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

and then paracetamol supply from china starting up again, and the promotors are constantly selling off!

and then paracetamol supply from china starting up again, and the promotors are constantly selling off!