Hello @vikas_sinha

Why did promoters of “Fairchem Organics” have sold off roughly 16% of their holdings despite posting decent results. Am i missing on some bad news ?.

Please share your insights as you also follow this company closely.

Thanks !!

Hello @vikas_sinha

Why did promoters of “Fairchem Organics” have sold off roughly 16% of their holdings despite posting decent results. Am i missing on some bad news ?.

Please share your insights as you also follow this company closely.

Thanks !!

Hello @vikas_sinha sir ,

Can you please share your views on Titan Biotech , Fairchem Organics and Pix transmission on current valuation for 5-7 yrs investment horizon.

Regards&Thanks!!

Titan bio, not that familiar, but seems to be a one horse story with only viral transfer medium used for covid testing. Tough to take a bet on nano-caps which are not that well discovered.

Fairchem organics, has 2x capacity utilization ramp-up story to slowly play out in the coming ~2 years, now that the full capex has become operational. Their products seem to be well in demand and process has an advantage over competition.

Pix has reached fair valuation based on the future projections of the facts known currently. It is now more of a re-rating kind of bet now, which will only happen in next ~2 years, based on consistent earnings growth due to stable/improving margins and ramp-up of sales with the capex about to become operational, together with continued longer term growth capex.

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

Thanks!

No, not working full-time since almost exactly a year now. Was never that ambitious or bothered about societal pressures. I have no issues in not being loaded like a donkey in order to perform. Am perfectly capable to enjoy time by myself. Life is too short to focus on anything other than life  Something like IBM Pollyanna Principle - Wiktionary, given my background in computer science and automation. I think about investing about 2-3 hours a day.

Something like IBM Pollyanna Principle - Wiktionary, given my background in computer science and automation. I think about investing about 2-3 hours a day.

My current corpus is 3x my savings. Savings alone may be enough, but it would have been tough, depending on a very thrifty lifestyle, it is always better to err a little on the side of safety. My expenses have actually increased considerably with this greater buffer, since I do not include family/ancestral wealth etc. in this computation at all, just my own earnings. And thankfully I also happen to be the poorest of the lot

Perhaps at a later date

Promotors of Fairchem may have very different investment objectives from us. It is like reducing a position to fund another opportunity they might have found. Yes, it is never re-assuring when promotors sell but we do have a fairly objective set of facts, to have some amount of conviction in the story. Also, Fairchem was never a too big position for me, it is in the middle 30% of the folio, towards the lower side. The share had indeed run up to considerable valuation too fast and any sales ramp of such great size would naturally take years going forward.

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

Hi @vikas_sinha … thank you for your regular inputs on the thread.

Wanted your views on these — as these stocks seemed to have a decent financial performance between Q1-3, but it doesn’t seem to get reflected in the share price…

GMM Pfaudler, HDFC bank, Dabur, Confidence Petro, PI ind…

Also, how do u value a stock like Oracle Fin, Serv ? Topline going down for some time, but Bottomline /EPS + Nett profit is getting better… since IT industry trends are quite clear, personally couldn’t assess this stock .

Your views would help.

thanks

@vikas_sinha Looking forward to your views on IT sector, especially the service organizations. Everyone talks about TCS, Infy, as IT being resource intensive industry big players have that edge. How about the small players like Birlasoft, Zensar. Happiest Mind went through a good correction. Please share your perspective on IT Industry.

hey vikas ji whats your views on inox and pvr merger ?

10 inox shares(469/share) will be converted in 3 pvr shares (1821/share) i see a arbitrage opportunity of around 14% gain . (if you buy 10 shares of inox today total value=4690 , you will get 3 pvr shares total value =5463 ) plz correct me if i am wrong .

( just a query not a buy reco to anyone)

Hi Sameer, welcome to VP!

Thanks!

I am not tracking most of these, maybe one or two for a while but not anymore, but will share my ideas anyway if it helps.

GMM Pfaudler, has a complicated mix of conditions! I personally chose HLE Glascoat but exited bit early! Both are extremely highly valued and risk of downside is always there since capacities will take considerable time to grow, the safety in long-term is the moat and strong demand.

GMM faced mis-pricing allegations at time of QIP and also it bought slow growing overseas biz., but it has survived at a good price level even after becoming 4x between sept 2019-20. So, it was bound to consolidate for a while, and actually looks bullish going forward.

HDFC bank I have repeated before, it is a good financial biz, maybe compounding is bound to slow down with the huge size, so it should be bought at a decent price, and should hold for long term.

Dabur, in general I do not like the general consumption theme, FMCG is no go for me, due to huge valuations and great competition with low moat. Management is good and business is good, but price is too much to provide decent upside.

Confidence petro is again bit complicated, people say it is a bull market company, it depends too much on relations with govt entities, I am myself not a big fan of CNG story anymore after converting my car (limited range, loss of power, added weight, loss of space, slow-filling+long queues, safety concerns), since price differential with diesel has narrowed greatly after excise re-structuring and rise in CNG prices. (also diesel to CNG retro-fitting seems difficult)

PI ind, little expensive, it seems to find support at 2.5k level for a while and rise depends on future growth which seems will take a fair bit of time.

Oracle fin is bit like Dish TV where I am invested (smallest position, that depends on management coup though), yes it seems to be losing top-line but improving margins, I do not think it deserves any higher valuation given that almost entire IT pack seems roaring and the biz can be quite disruptive. Simply, the trend can reverse soon enough.

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

For IT, mid and small caps the valuation has run up quite a bit and we might be at the fag end of the rally, since there might be slower growth going forward. I fail to see the consistency in the earnings, it seems to happen in waves/cycles. Hence, indeed better to stick with the big boys at these valuations, happiest mind looks like in bubble territory to me, though in short term they may ride the favorable exchange rate.

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

True enough, likely the overall entity gets stronger and higher valuation. Sorry for being too late to reply. This was more an early morning or day trade, but worth it if you had cash.

Hi @vikas_sinha,

I am big fan of your business analysis. Do you have any view on Lux ind. particularly in the present scenario as the valuation looks very attractive ? Do you think insider trading can kill the business model of it ?

Please also share your view on '‘Narayana Hridayalay’ if you track it.

Disc. I am invested in Lux ind. with very small portfolio allocation (2 percent)

Hi Sourav,

Thanks!

Lux seemed to be drawing strength directly from GST and pandemic killing off smaller players. But up move was a bit overdone, and again the sell off is bit over done, and it can go back to 3-3.5k easily but personally I would avoid such promotors. Though there was money to be made around 2k mark.

Narayana Hrudalaya I kind of like, it appears decently priced, seems increasing scale is helping hospital biz, the promotors are well reputed too. I have not much understanding here though. The rising tide of hospitals may be the twin factors of high pandemic cases and the normal cases delayed by pandemic and now appearing to flood the system. So, I am taking precautions here.

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

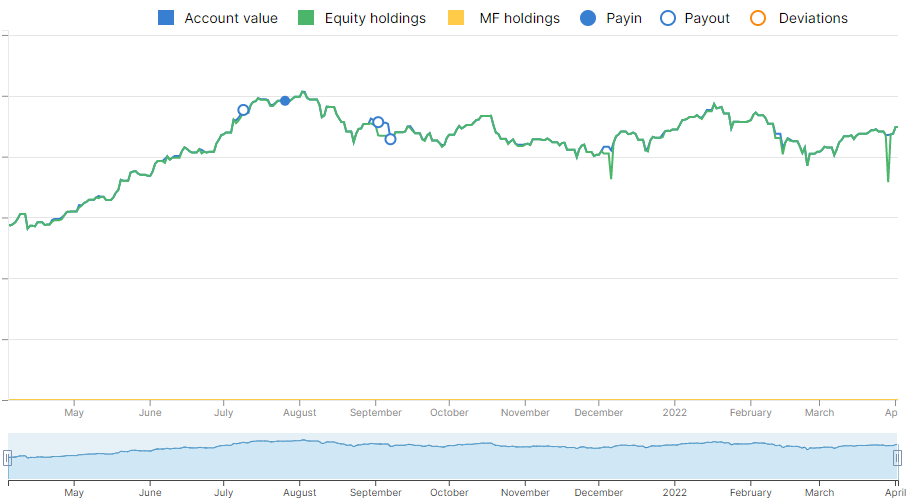

Latest folio status:

3% below ATH peaks of Oct 21 and Jan 22. (not accounting for withdrawals)

Performance by FY:

68% up in FY22.

425% up in FY21.

45% down in FY20.

32% down in FY19.

10% up in FY18 (starting in Sept 2017).

Approx. CAGR of 35% in past 4.5 years, given that various sums were added in lumpsums at 2-3 times in various years (but mostly mid FY20, added ~30%, around same time started to actively follow VP forum ![]() ), but largest was the starting corpus itself.

), but largest was the starting corpus itself.

7% taken out till-date, of which ~5% for taxes (all short term, so ~45% of PF was churned) and 2% rest (living expenses etc.) in FY21.

Most recent spike seen in the chart below is the loss-booking, post this, will need to take-out 4% mostly to pay the taxes for FY22. (all short term, so again about ~45% of PF was churned). Mostly will snip one or two holdings for this, from the lossy tail of the PF.

PF churn will likely fall severely going forward to almost negligible, given positions will stagnate or grow little and most have a ~2 year timeline for story to playout and valuations to get in sync. Unless more attractive alternatives are discovered, also less likely with a side-ways market.

PF value curve for the year:

Note – Table sorted by “% of Total"

| Company name | Last price | Cost per share | % of Total | Total Return % | Current Return % | |

|---|---|---|---|---|---|---|

| 1 | Tips Industries Ltd. | 2265 | 863 | 6.0 | 176 | 163 |

| 2 | Expleo Solutions Ltd. | 1675 | 632 | 5.4 | 188 | 165 |

| 3 | RACL Geartech Ltd | 601 | 256 | 5.4 | 179 | 135 |

| 4 | Sandur Manganese & Iron Ores Ltd. | 3513 | 1998 | 5.1 | 76 | 76 |

| 5 | Laurus Labs Ltd. | 597 | 326 | 5.0 | 309 | 83 |

| 6 | Pix Transmissions Ltd. | 862 | 454 | 4.6 | 117 | 90 |

| 7 | Mirza International Ltd. | 169 | 154 | 4.4 | 10 | 10 |

| 8 | Shivalik Bimetal Controls Ltd. | 519 | 294 | 4.3 | 78 | 76 |

| 9 | Ujjivan Financial Services Ltd. | 114 | 106 | 4.1 | -6 | 8 |

| 10 | Manorama Industries Ltd. | 1198 | 746 | 3.9 | 132 | 61 |

| 11 | Dynemic Products Ltd. | 608 | 395 | 3.9 | 76 | 54 |

| 12 | Godawari Power & Ispat Ltd. | 390 | 248 | 3.9 | 27 | 57 |

| 13 | Kopran Ltd. | 293 | 144 | 3.6 | 162 | 104 |

| 14 | Steel Strips Wheels Ltd. | 848 | 848 | 3.5 | -3 | 0 |

| 15 | Krsnaa Diagnostics Ltd. | 526 | 496 | 3.4 | -22 | 6 |

| 16 | KPR Mills Ltd. | 627 | 315 | 3.4 | 117 | 99 |

| 17 | Globus Spirits Ltd. | 1570 | 1276 | 3.3 | 26 | 23 |

| 18 | Shakti Pumps (India) Ltd. | 496 | 478 | 3.3 | 40 | 4 |

| 19 | Ugro Capital Ltd. | 171 | 168 | 3.2 | -22 | 1 |

| 20 | Meghmani Finechem Ltd. | 1003 | 772 | 3.1 | 30 | 30 |

| 21 | Kilpest India Ltd. | 349 | 389 | 2.9 | -12 | -10 |

| 22 | Fairchem Organics Ltd. | 1577 | 1574 | 2.8 | -1 | 0 |

| 23 | IDFC Ltd. | 64 | 64 | 2.6 | -1 | -1 |

| 24 | Praj Industries Ltd. | 395 | 372 | 2.4 | 5 | 6 |

| 25 | Sapphire Foods India Ltd. | 1444 | 1511 | 2.4 | -4 | -4 |

| 26 | Optiemus Infracom Ltd. | 325 | 317 | 2.3 | -18 | 2 |

| 27 | Dish TV India Ltd. | 16 | 16 | 2.0 | -35 | 3 |

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

Thanks for the update on the portfolio, and the motivation that comes along  …

…

Quick Question.

Are you adding to your position in Dish TV in the last 2-3 months ? Any feelers for people on the thread, considering there are mixed views on the Stock, and the fundamentals that are visible on ticker tape or any other platform, it doesn’t give too much confidence … TIA…

UPDATE:

Booked some gains in this rally and also exited Sapphire foods (20% biz is in sri-lanka which will take time to come out of deep crisis, my mis-timed thesis was based on tourism picking up fast).

Sold off little bits of Pix, Tips, RACL, Laurus, Manorama in that order, and tiny bits of Expleo, Shakti, KPR, Globus, GPIL, based on correcting holding sizes and the prices running bit ahead of fundas.

Mostly needed money for taxes. Sapphire 2.5% and rest 1.5% of folio value.

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

No, not adding, it was a really special situation play, based on lenders (now majority owners due to default), successfully ousting the current promotors. There is a political angle, with the promotor group comprising representatives of the current central govt. And media control being a hot topic. So, the coup looks difficult, hence there is quite a big element of risk.

The company is in declining biz but nothing stops it from adding some growth through alternative biz plans (such as watcho). The cash is real and it is huge, the worst news maybe behind us.

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

hey vikas ji hope you are doing good, have few for you

1 as the markets are in correction mode or can say is range bound how you manage your pf and are you finding some value in some stocks or sectors ??

2.after you told to look at gpil i started reading abt the co. and find it very cheap also their eps is doubled from last year and the topline is growing extremely well . but i didnt bought it as i was studying and the price today has gone up more than 50% but still it trades at a single digit pe . i am confused abt the good time to add onn can you throw some on light on this ?? like how you time the stocks ?

3.your view on bororenew and apcotex (valuation wise as one is ath and other is at 52 week breakout )

lastly thankyou for constantly updating here

one more add onn

4. what are the things you look before buying a co. (your most imp. criteria’s)

Hi Bhavya,

Thanks!

Normalization is a theme to play in sectors badly hit by covid, where the valuation has yet to recover, coz I have the conviction that covid is over. Financials may be worth a look, it is just a waiting game for the quality players to make a come back. Personally I find financials a bit risky because of leveraged lending. My situation is quite comfortable, think I have a solid set of stocks to sit back for the next year or so for their stories to play out. Perhaps a churn of 5-10% of folio if something more attractive comes along.

I never did time GPIL three times in a row, got fourth time lucky. First was the buy in mid 2018, then selling it at a loss in end 2019, and then failing to buy it in mid 2020. Finally built the current position in mid 2021 and that has managed to make more net profit than all the size of the loss. Recent developments are bullish, they focus more on ore revenues than capital intensive steel making. This is conviction bet on promotor sensibility and the long and rich mines they have. Commodity cycle may not cool down for several years since covid recovery has just started, I don’t think liquidity has pushed speculative pricing. But I would not buy a large quantity and may need a little patience, think bit long term.

Boro-renew is bit risky at this point, yes they beat Chinese/ASEAN sourcing, with help from duties, and have a world-beating product and that might be enough to gradually build a position, jumping in head first seems unwise on the other hand. Not sure about the dynamics of the QIP announced recently. Apcotex I do not follow much, high ethanol blending means engines cannot have rubber based products in contact with the fuel. Isn’t rubber very cyclical due to supply chain?

DISCLAIMER : this is not investment advice, I am not a sebi registered investment advisor

please do your due diligence before investing

Rest all is negotiable, numbers only matter so much, if the price is right given the narrative.