Thank you very much

I am invested from rs 78 levels - bought it 3-4 weeks back

Did not looked into the technicals but books looks good

Thank you very much

I am invested from rs 78 levels - bought it 3-4 weeks back

Did not looked into the technicals but books looks good

Have also been tracking Marksans for a while now… the company has come a long way from where it was in 2016-17 and if the last two conference calls are anything to go by, the runway for growth looks promising. Promoter participation in the capital raising (albeit with a smaller amount) helps reinforce the conviction.

Hi Edward,

Thanks for your input! Hmm, barely 100 Cr cap, cannot see much results data on screener (hence using trendlyne instead), seems to be alternating between loss and profit every year/quarter. Holding company discount is quite correct. Historically, best ever EPS was 7.5 (median is 5) and even with a figure of 10, PE works out to be 23! Currently fixed asset base is 32 Cr and adding 16 Cr block to it can possibly do better than EPS of 10. Even after considering holdings, it seems to be priced fairly, given it is quite inconsistent, IMHO.

Cheers!

Vikas

Thanks Vikas for that

As usual much appreciate your views

Your observations are correct

However the ophthalmologist plant has just gone live and I am hoping they could use Ipca contacts to push sales

If the new plant gets utilised this quarter profitability could be consistent

Besides Ipca could have directly bought resonance. Probably easier for them to grow a small company into another big one using their experience of growing ipca instead of growing ipca into a bigger company

Makers didn’t advertise the plant earlier probably ipca management wanting to surprise the market

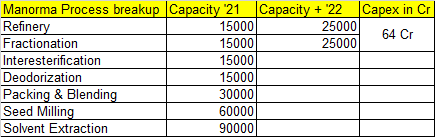

Manorama Ind. slightly better results QoQ and YoY, further 3x expansion planned to be completed within a year.

Previous expansion was from 5k MTPA to 15k MTPA.

Now, total will be 45k MTPA.

Current capacity use at 66%, maybe other bottlenecks are causing delay in ramping up of sales.

Investor presentation:

Results with commentary at the end:

Hi Vikas, Manorama Ind had equity dilution during IPO in 2018, even then raised huge debt by 2020, and is now going for big capacity expansion even though the utilization is low. These appear to be red flags. The share itself is expensive at more than 60 PE ratio.

I read your earlier comments regarding the company. During the time of its IPO, I read the prospectus, which mentioned a number of high-value litigations with a related company. Therefore, I never believed in this company. Fortunes seem to have changed within a short span of a few years. Is the risk-reward ratio of the stock still favorable?

Manorama Ind. is increasing its capacity in some areas like Fractionation & Refinery by 25000 MTPA each.

They have reduced debt to 84.8 Cr compared to 119 Cr in 2020 .

Debt/Equity has come down to 0.59 in 2021 compared to 0.9 in 2020.

Improved Cashflows. Also inventory has come down from 15 to 10 Cr, cash flow form operations are 37.9 compared to -60 Cr last year.

EBITDA margins have dropped due to various factors contributing , like container shortages , underutilization of facilities & suspension of operation in lockdown.

EBITDA should improve going forward with optimum utilization of plant .

Company is setting up office( maybe an warehouse) for storing and transportation of RM from Africa.

But I am still not clear why a debt of 119 Cr was raised last year. ![]()

UPDATE:

Sold off half of my Pokarna holding and bought equal amounts of KPR and Praj (3% and 2.5% of folio respectively), shipping crisis is pulling down margins to historic lows and this will last for years, and there was too much concentration.

Vikas, whats your take on Asian Granito. Seems highly undervalued and the business is also doing fine. Promoter selling is a major overhang but that should stop soon. Do you think Asian Granito deserves a buy on dip ?

Also let us know your take on Globus Spirits. Seems a long term structural story with higher % of B2C which led to margin increase and tailwinds due to ethanol blending. In recent concall they have announced a major capex as well

Hi Vikas, Can you please advise…how this will be last for years?..i mean shipping crisis for pokarna…

Please advise

UPDATE:

Sold off more of my Pokarna holding, 70% sold off in total, added Time technoplast, 2% of folio.

Hi @vikas_sinha ! What are your views on Precision Camshafts, in terms of long-term growth potential, financials and fundamentals? Thanks!

Latest folio status:

| Company name | Last price | Cost per share | % of Total | Return % |

|---|---|---|---|---|

| Shakti Pumps (India) Ltd. | 764 | 533 | 11.8 | 43 |

| Bajaj Steel Industries Ltd. | 974 | 451 | 7.5 | 116 |

| Manorama Industries Ltd. | 1449 | 683 | 7.5 | 112 |

| Laurus Labs Ltd. | 671 | 170 | 7.0 | 295 |

| Vipul Organics Ltd | 170 | 120 | 6.1 | 42 |

| RACL Geartech Ltd | 346 | 252 | 4.5 | 37 |

| Pix Transmissions Ltd. | 616 | 454 | 4.4 | 36 |

| Tips Industries Ltd. | 1426 | 861 | 4.3 | 66 |

| Bajaj Healthcare Ltd. | 817 | 475 | 4.2 | 72 |

| Filatex India Ltd. | 97 | 75 | 4.2 | 30 |

| Kopran Ltd. | 233 | 135 | 4.2 | 73 |

| NMDC Ltd. | 185 | 156 | 4.0 | 18 |

| Asian Granito India Ltd. | 185 | 157 | 3.8 | 18 |

| GNA Axles Ltd. | 457 | 401 | 3.6 | 14 |

| Dynemic Products Ltd. | 456 | 391 | 3.6 | 17 |

| Godawari Power & Ispat Ltd. | 1325 | 977 | 3.5 | 36 |

| Expleo Solutions Ltd. | 803 | 631 | 3.3 | 27 |

| Marksans Pharma Ltd. | 86 | 80 | 2.9 | 8 |

| Praj Industries Ltd. | 371 | 373 | 2.7 | -1 |

| Pokarna Ltd. | 340 | 163 | 2.6 | 109 |

| KPR Mills Ltd. | 1547 | 1573 | 2.3 | -2 |

| Time Technoplast Ltd | 90 | 86 | 2.0 | 5 |

Changes update given here in almost real-time as done over past 3.5 weeks. Total 11% gain in that time. 22 stocks in total.

The past year trend: (4.5x, thanks to VP forum ![]() )

)

UPDATE:

Sold off NMDC fully and reduced little from Manorama, RACL, Vipul, Shakti and Kopran in descending order of weightage.

Added in equal amounts, Valiant and Fairchem organics, based of course on VP Forum threads.

Another trigger for bajaj healthcare.

3 approvals in 2 month for covid use.

Sir

In a world swarming with fake investing gurus’ it’s difficult to find anyone as authentic as you. Thanks for the regular disclosures about your investment and positions; it’s helped me to dip my toes in the uncertain but inviting ocean off equities. I have been able to generate decent returns over the last quarter - not as much as you have, but reasonably good and satisfactory as per my standards!

Thanks & power to you!

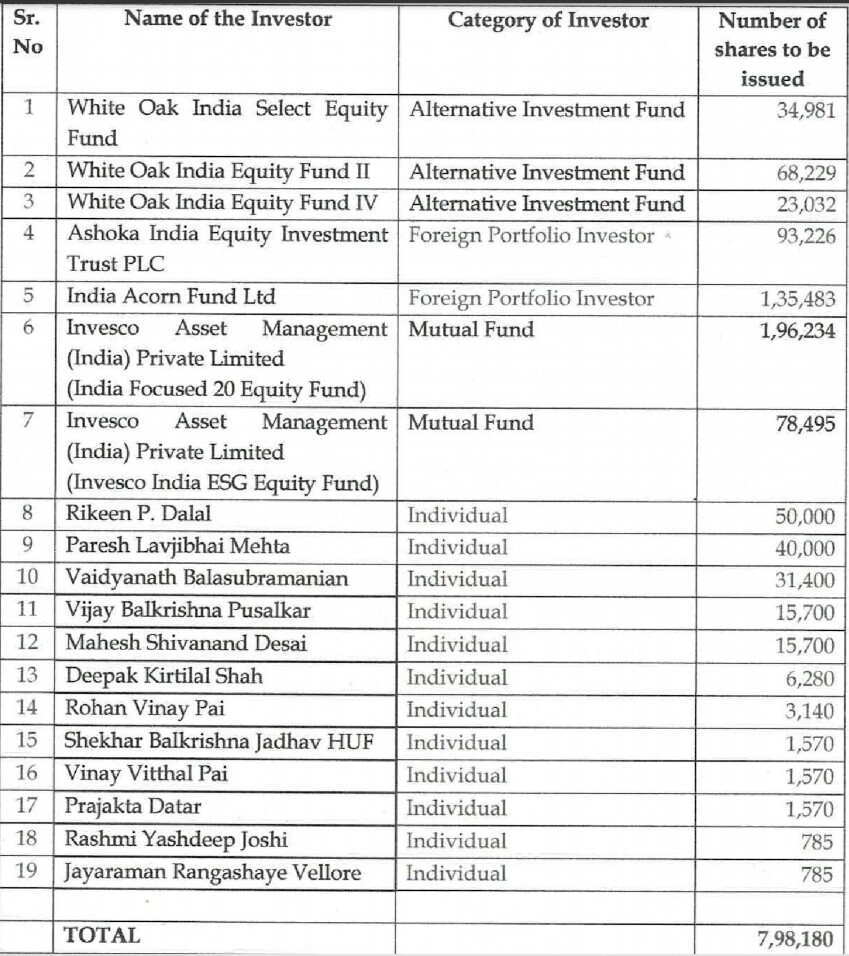

Manorama Industries announces QIP done to AIFs, FIIs and MFs.

The expanded capacity plans will approx be 6x the past quarter results, since new plant was not fully functional for various reasons related to covid. It also leaves room for more downstream processing expansions and also an earlier promised expansion is still not detailed.

Share has been flying, now ~1600 but QIP is done at ~1300 for raising ~100 Cr, mota moti ![]()

Thanks bro! Full disclosure is the idea, and timing is important in a flying bull market. Your picks have been helpful. The tip on Tips industries helped, though I missed picking up Deepak fert and chem. Your timing was impeccable, I doubt you were a market maker for the stock which took wings 2 days after your reco. With quite good hit rate of 2 in 3, so you will do well I hope. VP forum helps even a mediocre investor to get educated enough and raise the game to an entirely different level.  Keep messaging on DM.

Keep messaging on DM.

Hello @vikas_sinha sir, what is your latest folio status. Did you make any changes.

Indeed, I have made some tiny adjustments only, sold off some of Shakti, Expleo, Bajaj Steel and Vipul, am trying not to get position size too big proportion for one single entity, added to Praj, Valiant and Fairchem, total transaction worth 1.5% of folio size

Bought Sandur Manganese, transaction worth 1.75% of folio size.