Pokarna will not be able to get good figures, I guess simply by looking at the Stone-update website, given imports from India have hardly changed QoQ. Yes, even this will be very good YoY and support the stock. I guess shipping crisis and competition is choking ramping up of sales to the US markets. The strong housing trend will last more than a few quarters, but this will take some patience.

Reasons for Expleo and Tips have been enquired beforehand! GPIL needs no introduction, the thread on this is tremendous, the company is awash with cash to grow! This shows management acumen, they have the opportunity to strike when the iron is hot

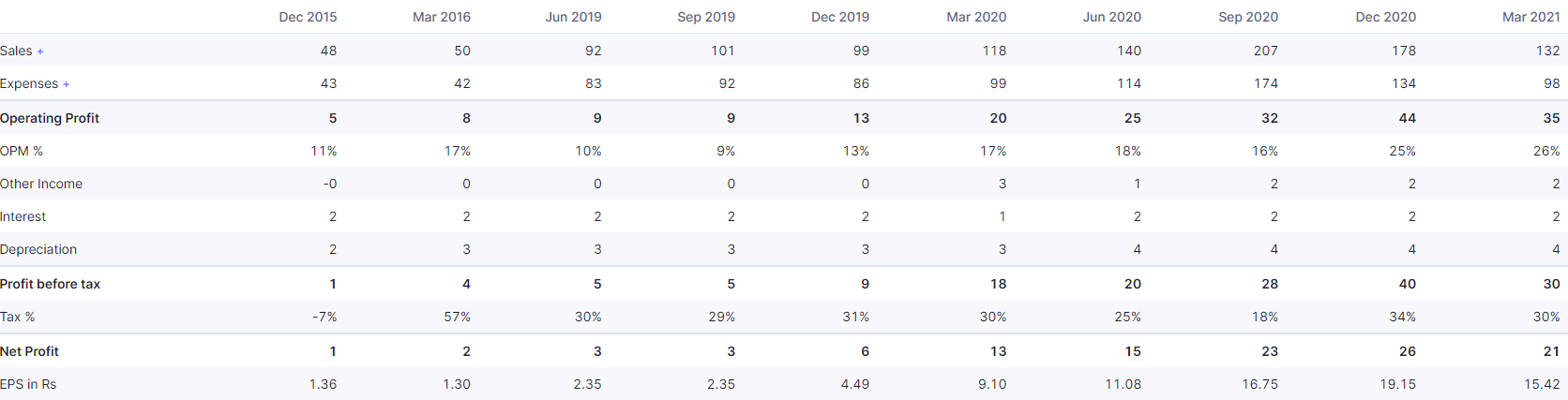

I think focus should be on 17% higher sales value QoQ, input materials cost is lower. But rest all expenses are higher, and tax is also higher. Depreciation will naturally escalate at a snail’s pace. Main diff is Other Expenses, which reminds me of RACL results yesterday. Freight and fuel can be higher, and input cost escalation is passed on with some delay. Others are not that significant. Containerized Exports/Imports are facing severe shipping crisis. Domestic focus will do better in such scenario.

Sab changa si!

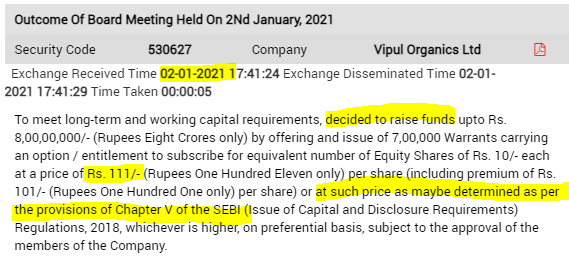

I also didn’t like the fact that they alloted preferential shares at 111 rs in feb when price was 140 something

Still will hold it for 2 more quarters ,sales as you said have risen coupled with lower material and employee cost march quarter in the past have not been the best as well looking at past records lets see what happens.

Announcement under Regulation 30 (LODR)-Preferential Issue

Security Code 530627 Company Vipul Organics Ltd

Exchange Received Time 23-02-2021 18:46:52 Exchange Disseminated Time 23-02-2021 18:46:58 Time Taken 00:00:06

Pursuant to the provision of Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, we wish to inform you that the Board of Directors of the Company at its meeting held today i.e. 23rd February, 2021; inter-alia, allotted the 7,00,000 Warrants convertible into equal number of Equity Shares of Rs. 10/- each of the Company at an issue price of Rs. 111/- per warrant (including premium of Rs. 101/- per warrant) on preferential basis to the promoter and promoter group upon receipt of 25% of issue price from the allottees in accordance with the provisions of SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018.

The above warrants entitle the allottees to apply for and be allotted equal number of equity shares for each warrant held by them on payment of balance 75% of the issue price within 18 months from the date of issue of these warrants.

No, I find it difficult to time markets. Am satisfied with bit lower gains, but do not want to bother playing the 10% lower buying game with 10-20% of folio value etc.

Thank you Vikas,

I have different question now. You had earlier faced a drawdown (probably 60% or so - I read it somewhere earlier in this thread) in your investments. Do you have any plan to tackle that now? Like stop loss? Exit if a stock falls 10% or something like that? Sorry if you have already mentioned it somewhere in this thread.

Thanks,

Anto

I have faced the small/mid-cap carnage, the ILnFS/NPA derating, DeMo/GST issues, 3% growth rate, and above all terrible stock picking like 8K miles etc. a long list given at the beginning of this thread.

This reduced the PF value by 50% by Oct 2019 (starting with a lumpsum invested in Sept 2017). Thankfully, I added an equal amount of fresh capital. (equal to the reduced holdings)

Next drawdown, happened in March 2020, by when the PF had hardly recovered. It again reduced the value by 50%. I was hence left with approx. 30% of entire investment. Since then it has become 8x. I did no sell no buy, nothing, the market just came back. The earth kept turning, nobody used missile launch codes etc. If something really bad had happened money would not be of any use anyway.

If the world keeps running it is just a matter of time and I had no need for the amount, had more than enough to cover my needs as regular cash flow. It just postponed my targets by 3 years I reckoned, assuming no more bad news and bad actions. Did not foresee a record bull run indeed.

Now, I have enough to even fantasize of a 50% drawdown without issues That would still leave me with CAGR better than FD.

Hmm, all you asked was sufficiently answered by:

Yes, I do have GTC for all holdings at a certain stop-loss ~30% below latest price. But I forget to update it for weeks

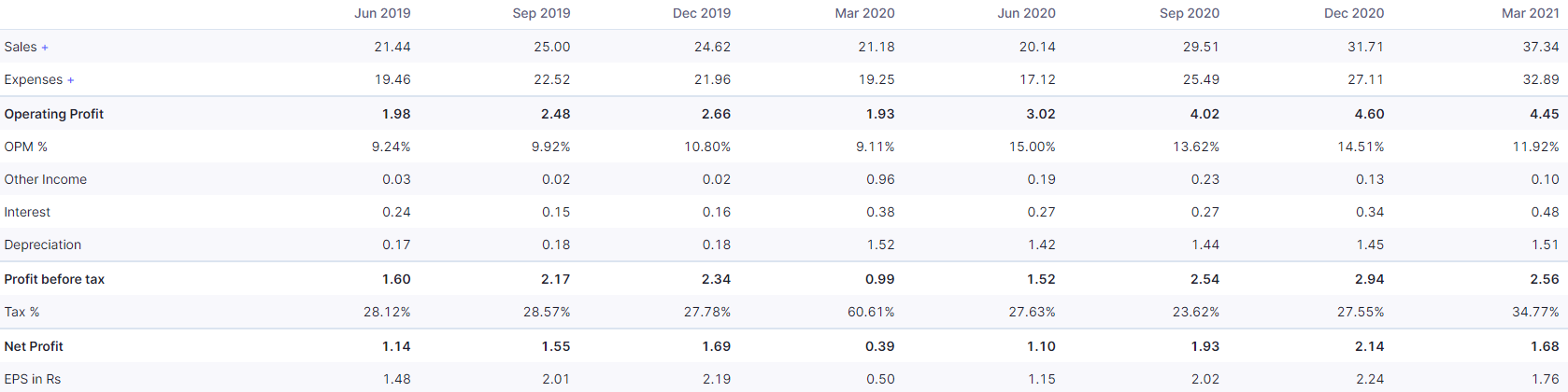

Vipul is doing fine, IMHO!

Q3 was best ever, Q4 is not bad!

QoQ Operating profits are down 3% only

Sales are highest ever, QoQ up 18%

QoQ PBT is down 13% and PAT 21%. Mainly interest and lower OPM made the difference, likely they should go back to recent quarterly averages. Hopefully, debt gets paid back with increasing cash flows. They have maintained the dividend rate.

Bajaj Healthcare is not doing that great, expected a big positive given management bullish commentary in Q3 media release. Need to wait for 1-2 days for the next release and see what details are disclosed.

Valuation wise still comfortable, given a great quarter expected for Q1 FY22.

OPM is highest ever.

Best quarterly PBT ever, leaving out Q3.

Dividend yield improves a lot to 0.5%.

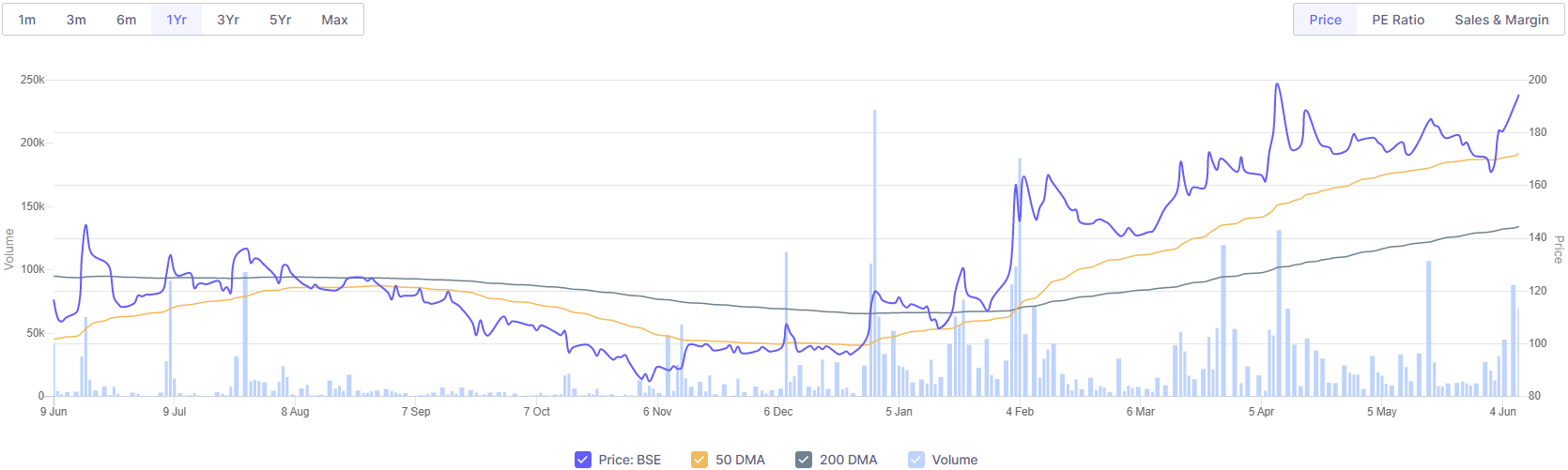

Watched the circuit, but looking at buy-sell proportion waited for the circuit to open, average buy around 9:40 am was @79. Yes, it does feel good to make some instant gain, but 4-5% is hardly the point!

Bajaj healthcare media release/discussion on results with no mention of the issues faced in the past quarter! Guidance of 20% growth for FY22, stable margins, very possible if the corona related medications make a dent in the market.

I like cheaply valued finds, hopefully not well discovered, value picks. Except Laurus, all the 3 pharma stocks I hold are in the 10-15 PE band. Marksans I would rank better on most parameters than Kopran or Bajaj healthcare.

I was bit doubtful of continued growth but fresh funds raise from an eminent player in the healthcare domain shows promise. It may take a while for growth to pickup, but comforting valuations offer peace of mind! Mostly quality of management, level of engagement/disclosure and scale of biz demands a re-rating!

These guys are hitting above their weight, showing tremendous growth maybe because of being small or better focus targeting the exact same developed markets as the large-cap pharma heavies. A great comeback from their crisis days!

Did you look at Makers Lab. They are Ipca group

Makers Lab hold 45% of Resonance Specialities

Resonance Specialities is valued at 187cr, Makers percentage would mean 84cr

Assuming holding company discounts of 30% probably purely based on holding company could be valued at roughly 59cr

Makers are valued at 110cr on consolidated business. So stand alone is valued at 51cr

Makers themselves have done a capex of 16cr for opthalmic drugs which went live I think around Feb

Just finished quarter was a loss largely on account of interest and higher depreciation.

I think new plant will take another quarter to generate some meaningful revenue

That would still leave me with CAGR better than FD.

That would still leave me with CAGR better than FD.