•TARSONS is among the top 3 plasticware laboratory equipments manufacturing companies of India. As of March 31, 2021,the co has a diversified product portfolio with over 1,700 SKUs across 300 products used in various laboratories across research organizations, academia institutes, pharmaceutical companies, Contract Research Organizations (CROs), Diagnostic companies and hospitals.

• End consumer:The end customers of our Company’s products mainly include research organizations, academia institutes, pharmaceutical companies, CROs, diagnostic companies and hospitals (Indian Institute of Chemical Technology, Dr. Reddy’s Laboratories, Dr. Reddy’s Laboratories and Dr. Lal Path Labs.)

•Scuttlebutt notes- Thyrocare using Tarsons products.

•Tarsons has a large network of distributors of over 141 distributors on 31st March 2021; ~75-80% of the total distributors have been with Tarsons for over 20 years indicating a strong supplier and distributor relationship and a stable distribution network.

•33% of total revenue came from overseas market in FY21 vs 26% in FY20. Tarsons sell products to more than 40 countries and has plans to export to ~120 countries in the next 5-10 year.

•Revenue from sale of goods to top 10 distributors was representing 37.33%, 39.97% and 43.49% of total income from sale of goods for Fiscals 2021, 2020 and 2019, respectively.

•Trade Receivable (cr)= 15% of total assets.

Net proceeds of the IPO to be used in 2 ways:

Co’s expansion plan- The net proceeds will be used for expansion at Panchla for current products as well as new products.

Repayment of ₹75cr of borrowings.

Opportunity size:

Global healthcare sector is expected to grow at a CAGR of 8.9% and medical devices & technology sector is expected to double by 2025F.

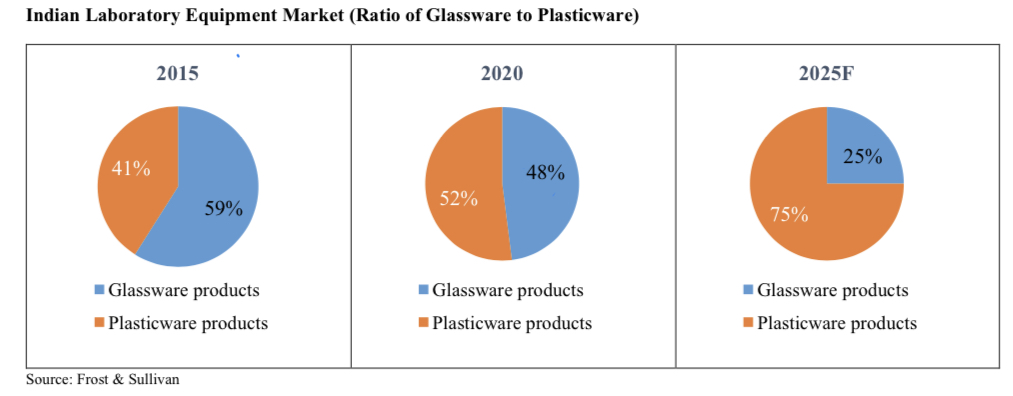

Shift happenning from glass consumables to plastic consumables as they have a long shelf life in addition to being unbreakable and inexpensive as compared to glass. Indian plastic labware market is ₹1225cr. Market share of Tarsons is around 12%. The domestic market for plasticware lab equipment in India is expected to grow at ~16% given the huge adoption of plasticware products over glassware products.

Debt equity and overall gearing ratio improved at 0.09x and 0.17x as on March 31, 2020 as compared to 0.37x and 0.46x respectively as on March 31, 2019.

Tarsons has 5 manufacturing facilities in West Bengal with the sixth facility under development. The latest facility that is to be developed in Panchla has a capacity and area equal to approximately the combined capacity and area of all its other facilities. This will allow the company to manufacture double of its current production effectively providing a potential to double its revenues as well. This facility is intended to be funded from a combination of internal accruals and proceeds of the Offer.

The Make in India initiative is aiding Tarsons to bring in affordable consumables and reusables by making them in India at 15- 20% lower prices than imported products.

Tarsons is aiming at venturing into the development of new end products with high realization and higher value and transitioning itself from a Life Sciences company to a Bio-Tech company.

Tarsons’ upcoming manufacturing facility in Panchla will enable the entry and expansion of the company into the new product segment comprising of PCR, cell culture, Serological Pipettes among others.

Risks:

Around 75% of raw materials are imported. However, the prices these high-grade resins (despite being a crude derivate) are not as volatile as the crude prices, and are generally passed on down the value chain. In Fiscals 2021, 2020 and 2019, cost for raw materials was ₹44.8cr, ₹38 cr and ₹42.2 cr, respectively, which accounted for approximately 19.16%, 21.18% and 22.86% of total income, respectively.

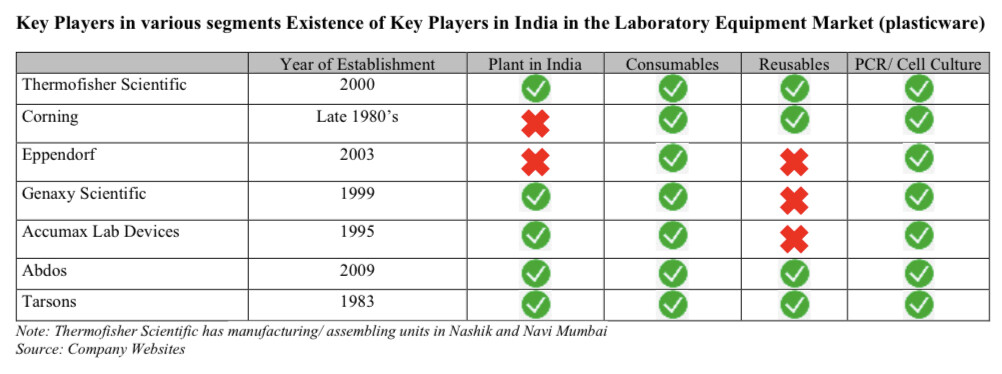

Competition from large companies like Corning, Thermo Fisher and Eppendorf have dominated the market due to their strong R&D facilities and brand name.

(Thermo Fisher Scientific have increased their production for PCR based detection kits.)

The approval for conversion of majority of the Jangalpur Land from agricultural land to non-agriculture land is yet to be received. For Fiscal 2021, Jangalpur facility contributed 58.00%, of the total consolidated sale realisation of theCompany.

Speaking from personal experience + scuttlebutt, their lab products (especially plasticware) do not stand up well compared to their competitors. My lab and I have used their vacuum desiccators as well as micropipettes and found them of poor quality, so prefer Finpipette/ ThermoFischer.

As for reusability- hardly! Plasticware, like Pasteur pipettes or centrifuge vials, is one-time use only and cannot be reused due to contamination.

Only 6 employees in R&D & Quality respectively . If quality & customizing products are so critical for customers in this industry ,how do they take care of them with just 6+6 employees out of 480 employees in total ?

2 The top & middle management seems all related so there are too many related entities leading the business . Though this could be perceived as skin in the game but it also could lead to some issues such as - a) taking non-consensual /difficult decisions

b) management increasing their salaries disproportionately to corner profits as they grow

c) currently no track record of sharing fruits of business with other shareholders . So one would have to take them on face value that they would reward shareholders as they grow . Some of smaller compaies such as DHP india has similar margins but >50% of their market cap is parked in mutual funds .SO Difficult to judge the capital allocation record

3 The financials are only for 3 years .Having burnt my fingers in some SME stocks in the past where last year numbers showed significant growth compared to prior year (again just 3 yr data ). I did the error of projecting those growth rate to arrive at apprimate intrinsic value

Open to feedback from fellow members & incase someoen could throw more light on promotors & medium/long term track record on this company . It would be really helpful

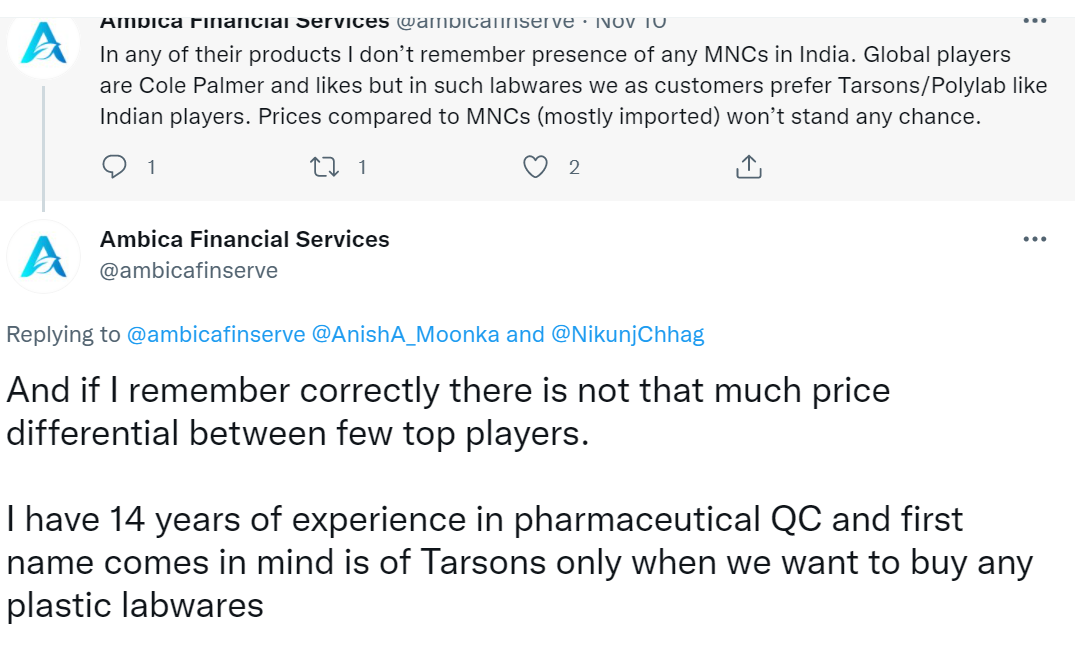

Saw these 2 reviews on a twitter thread on the company and now, quite confused as to what is the quality because these guys are saying, its actually good and even indicating mind-share of customer.

Also, Pipettes and vials come under consumables and not reusables so management has never called them reusable at all.

Im not sure how the quality of the product is…it would be a bit in the dominating side from the stand point of Indian context compared to the large players due to pricing.

The only red flag I see is the geographical presence only in Bengal.

They have large customer base in south side…could have extended it there…making it more diverse.

Bengal has a prevalence of calamities from flooding to political instability.

What do you guys think?

I was part of that twitter thread but didn’t get an answer… as all where confused as well.

Is laboratory glassware better than plasticware in terms of entry barriers ? trying to compare if Borosil Ltd a better idea compared to Tarson ( also other parameters are better in terms of valuations , management and business/brand quality)

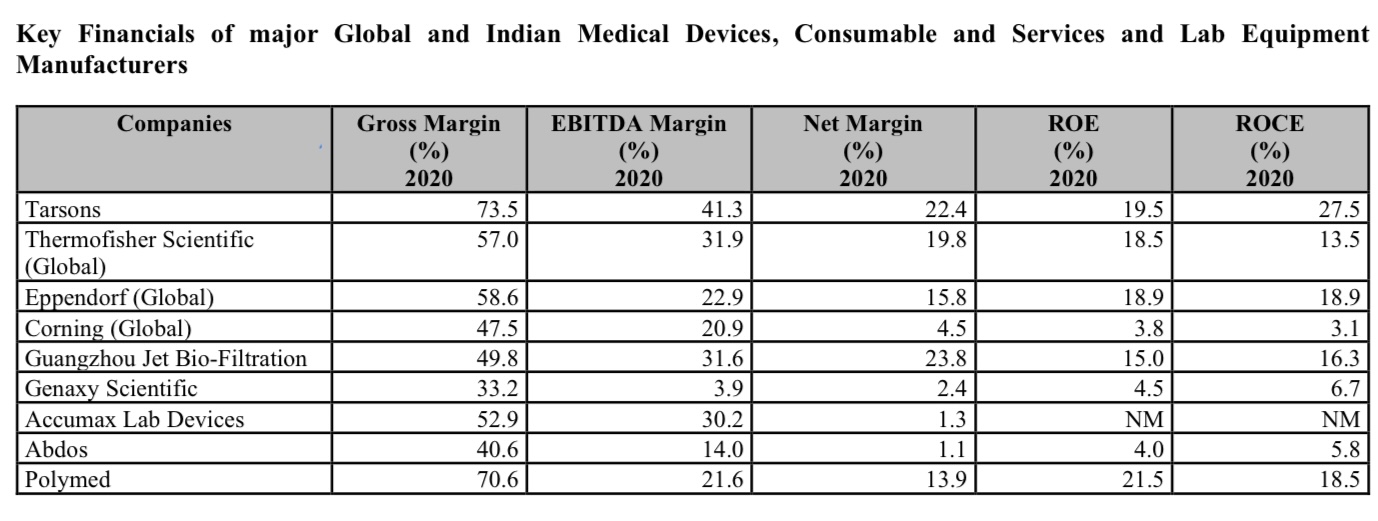

Global plastic laboratory product market is estimated to grow at 10.5%, while India at 16%, which indicates good sectoral tail wind. Gross margin at 73%. Net Margin at 20%, RoE at 20%, RoCE at 27.5%. SOIC video is good to understand. Need to collaborate with VP people to dig deeper.

I am studying it and find good for investment.

Entry barrier is similar in both cases as both kinds of labwares need quality certification.

Glassware has more wider usability as it can be used even with organic solvents, but for most other purposes plastic-ware is quite capable.

In Glassware Borosil is gold standard. They even have strong pricing power.

Tarsons’ products are good but there are better products. However, they definitely have the best low cost products. Their products are also more widely available, but this can be a subjective experience because I researched in a Kolkata based institute.

In lab instruments, Borosil has just initiated its presence through Labquest brand. I personally haven’t had any experience with it yet. Tarsons instruments have already a good market share. Here also I can say that their products are not top-notch but still gets sold because of lower cost.

The above snippet is from RHP of Tarsons Products (Page 114) and is actually extracted from a report by Frost & Sullivan.

I just wanted to understand what exactly will happen so that the end markets will start growing at 1.5x-2x rates, and how reliable is that projection. It is important because the investment thesis in Tarsons is partially based on that projection only.

75% of raw material is imported subject to price and forex volatility. 31% is raw material cost.

All plants are in one Indian State, West Bengal.

Though company have good growth prospects, I do not have any info. about promoter quality.

I am thinking based on current information available, this is case of where blanket hide gems. Now market consider IPOs are priced high and avoid.

May be a good opportunity hiding here.

Disclosure: Invested and thinking to add on dips.

Indian pharma industry getting more business and as an indirect beneficiary, they stand to gain.

If they are able to reduce the imports and gain more domestic share due to plastic shifting trends.

The growth might have been exaggerated a bit by 1 or 2% though.

One doubt I also had regarding to this was how to value Tarsons. There might be no domestic peers but it’s not fair to value them according to megamoths like Thermo-fischer etc. They have years of refining and higher spends on R&D. What multiples should they really get ?

IMHO these projections can be achieved. From the above we can derive the end market CAGR is 15.38%

If the end market is growing at this rate then we can safely assume the labware will go either at the same rate or more than that ( in my view the labware market can grow beyond this )

Check the gross margin, though they depend on the imports but their gross margins are very consistent.

One of the raw material that they use is a bi product of phenolics production (Deepak Nitrite ) , since the market size / demand for these material is very low , none of the Indian chemical players are producing any of these.

Lot of noise around

It is a plastic, government can ban them - What is the alternative ? (We moved from glass bottles for beverage drinks to plastic , this is the case everywhere , we are now replacing the steel gas cylinders with PVC cylinders - Read Time Technoplast ) , look around us plastic is everywhere , so far governments not able to implement (including developed nations) plastic bag ban.

We cannot compare this company with Thermo Fisher etcc… and both are strong in their own way. I have checked with many people the common response is " Tarsons is the go to brand for them due to cheap pricing when compared to glassware " , quality wise they kind OK. But again if you compare the like to like glass vs plastic of the same SKU then obliviously glassware is better product.

This is a very good proxy play for the entire healthcare sector.