Very insightful analysis by SOIC on Tarsons Products.

From a valuation POV, it is fairly priced at a PE of 40x and the company will be approximately valued at 3500 Cr Mcap.

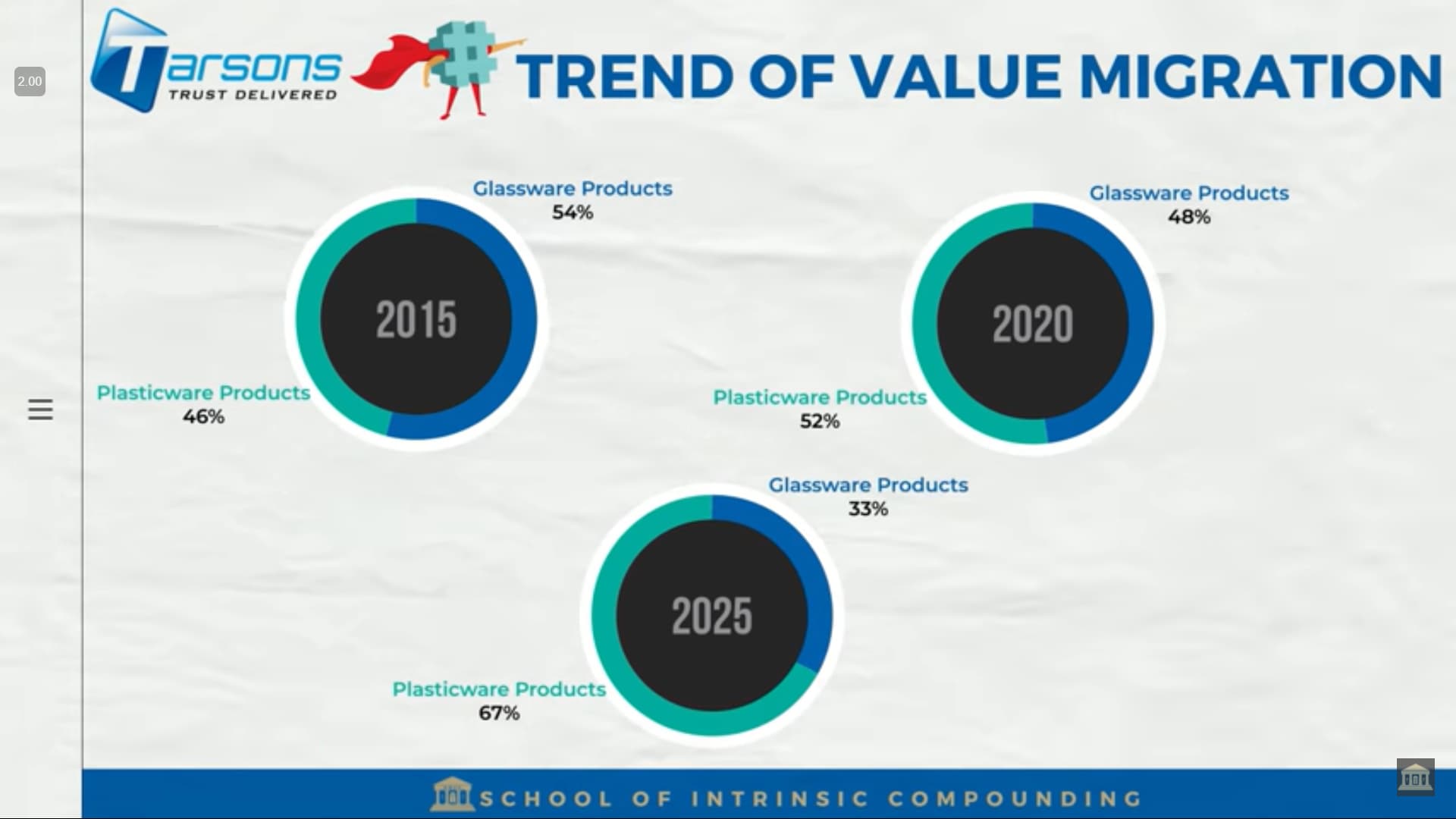

The lab equipment industry is currently experiencing value migration from glass equipment to plastic equipment as plastic is easier to use and recycle.

Source: SOIC

The Indian plastic equipment industry is expected to grow at 16% CAGR (10.5% CAGR globally) and Tarsons Products can be a direct beneficiary due to the tailwinds in this sector. It can be an interesting bet for the next few years.

Key Risks:-

- Geographical concentration risk (All the plants are in West Bengal. Any adverse event or a natural calamity can impact their operations)

- 75% of raw material is imported and fluctuating prices can dent their margins.

- PE firm holds 49% stake pre-IPO and post IPO holding is around 25%.

- No history of relevant experience of Promoter Group.

Disc:- Not SEBI registered. Still doing research.