When I am not working, studying or sleeping, I am researching into my companies. This is my hobby, past time, second career, second job, whatever you want to call it. Sometimes I spend more time in a week researching and reading than I do at my actual job.

Do not concentrate then, its not for everyone. Stick to what makes you feel better, nothing in this life is worth losing sleep over.

I am confident in my thesis and have a great capacity to suffer. Only buy a company if a 50% draw down will also not shake me and cause me to lose sleep over. That’s why I didn’t buy many names discussed earlier in this thread like Gujarat Gas, Acrysil, Hindustan Copper, SAIL. All Multi baggers since I mentioned them in this thread.

Booked profit and exited anything less than 4% of the portfolio, as I keep moving my portfolio towards more concentration. It was really hard and painful to let go of these positions as I believe in the companies and all of them are fantastic companies.

Exit Reasons Syngene, Biocon, Divis I added the proceeds from these to Laurus. Traits of all these companies are present in Laurus and I have far more conviction and can see the growth of Laurus beating these companies for the next 10 years.

Vinati and Navin Too expensive for my taste and I find companies like Deepak and Jubilant to deliver faster growth than these two over longer term.

All of the 5 are amazing top rated companies and I do expect them to keep rising.

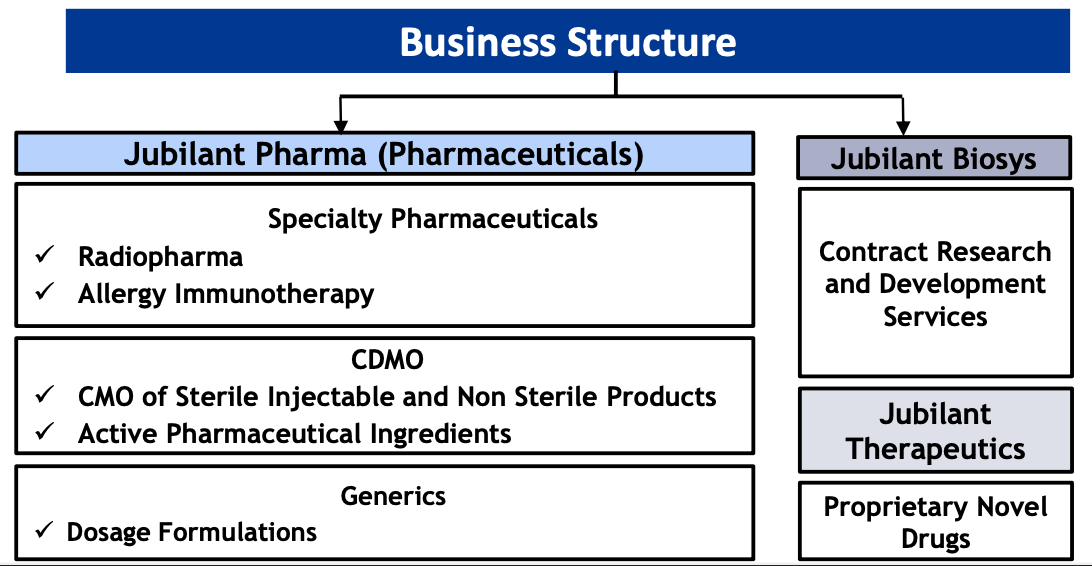

Hi @Tar seeing you’ve invested in Ingrevia. Would love to hear your views on Jubilant Pharmova which has quite a diversified business (maybe more potential demergers !!) and is available for a very attractive price.

I know very little about Pharmnova other than that they are leaders in Radiology and no one can compete with them in that field. They also do innovative drugs and honestly it’s too diversified a business.

I am invested in Ingrevia as I see a commodity chemical business transitioning towards speciality chemicals (major portion of revenue for Ingrevia is derived from speciality chemicals). I believe the company will re rate in future as street still believes this to be a diversified commodity business which isn’t really if anyone looks at their current revenue pie. I see the commodity nature of their business today more of a strength as they can really backward integrate to even some raw materials and thus get a grip on better margins in future. 5 years from today Ingrevia will be a backward integrated speciality chemicals company with superior margins.

Pharmnova’s Biosys business is very small today. If they are able to scale it up to a size of Syngene then maybe yes they will demerge, but that’s a story that will take at least 5 years and by that time Syngene will be way ahead of them.

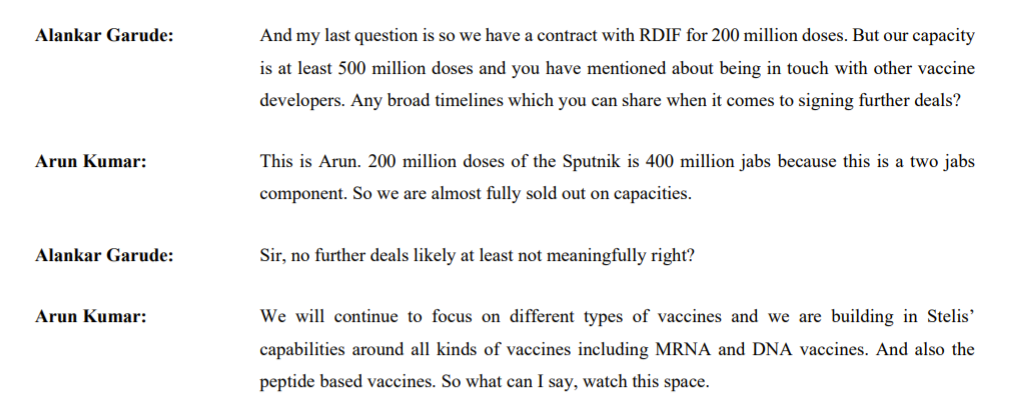

My thesis on Stelis seems to be playing out. As soon as US Russia relations stablized, Covax announced to deliver 1.4 Billion Doses to various countries in the world. No way they can do this without Sputnik and all the other vaccines being available and no way vaccines can be made without Indian firms being involved.

I expect Stelis to get more orders, this time even bigger ones.

It’s about the entire scientific supply chain of vaccines, the difference in making mRNA, adenovirus and peptide based vaccines, and has really nice implications for Stelis (and Laurus Bio) given Arun Kumar’s commentary.

There was no extra capacity for an unknown virus, and now companies are trying to find capacity,’ says Kis. It is somewhat easier than for mRNA production, because growing human cell culture for medicines is old hat. But expertise is crucial.

Existing capacity lies within facilities making recombinant protein for medicines or inactivated virus for vaccines. ‘Those could make adenovirus,’ says Kis, but ‘you don’t want to disrupt life-saving vaccines for other diseases or other injectables like cancer therapeutics.’ Also, adenovirus production requires more stringent biosafety requirements than for monoclonal antibodies.

It’s really exciting to see how their plans for extended mRNA and peptide manufacturing plays out. From my understanding, vaccine manufacturers are fractured, with mRNA expertise held by one company, adenovirus elsewhere in the world. If Arun Kumar’s claims play out, Stelis could be a one stop shop for all 3 vaccine types, and cash flows from these could last well beyond the current Sputnik order book.

Absolutely, Stelis already has the second largest viral vector capacity, only next to Serum.

Sputnik is also a very technically challenging vaccine to make. The vector used for second doze is different from the first doze. I think that is why Arun Kumar alluded to making 400 Million doses as they have to make 200 Million for each vector.

Couple of videos I like on Sputnik. Will add more thoughts on this later.

I also hold few of these stocks. besides the pharma stocks that you have i also have granules as valuations are still not very exp. and ive been holding on to it for last 2.5 years mostly will shift this to Neuland or Stelis.

Wrt to Borosil Renew i wanted to know if you have any update on more land being acquired by the company. I’m to understand that the current factory is good for 2000tpd but beyond this the company has to acquire more land. wanted your view on this point as to how easy or difficult will it be for the company to do get land. I also agree that growing 4x in size wont make much of a difference when it comes to the demand for the solar glass. This is the same reason why im not that worried about St.Gobain or Asahi entering this field. St. Gobain doesnt have the balance sheet strength or the product capability. For Asahi I doubt is this is something they are focusing on right now. But what ive heard is that PV module manufacturers are encouraging these two companies to enter this domain to bring in some sort of competition in the domestic market.

Anything I say here is just conjecture, but here it goes. The way I look at it, land acquisition in Bharuch (where BR is located) isn’t a big deal. Most likely they will get the land for free from Govt of Gujarat. Gujarat Govt gave many acres of land free just a couple of months back to ReNew Power. Gujarat will be the epicenter of solar industry in India and its already showing signs of it. Multiple firm in solar (both big and small) have set up shop there. So either BR will get land for free or will acquire more for really cheap prices.

Glass is looked as a commodity but isn’t very easy to make. A lot of technical expertise is required to make glass and even more to make solar glass. Corning is the only maker of Gorilla glass that goes on almost on smartphones in the world. Why hasn’t any other glass company taken over the market share from Corning if glass is so easy to make?

Solar glass requires efficiency levels as well. Anything less than 18% efficiency means solar plant wouldn’t perform so module manufacturers cannot cut corners when it comes to procuring solar glass quality.

And if glass was so easy to make and anyone with deep pockets could set up shop, why hasn’t Adani yet or why Reliance didn’t announce anything related to solar glass at their AGM with the announcement of Giga factories?

St.Gobain and Ashai both exited solar glass market many years ago, they would find it increasingly challenging to set up scale of plant and restart that business. Manufacturing of normal glass and solar glass isn’t interchangeable.

Here is a video on Corning that shows how much technology is required to make Gorilla glass.

In their Interview with Omkara Capital ( DHANDHA: BOROSIL RENEWABLES ), they have mentioned that apart from the existing 450TPD factory & already in construction 500TPD factory. They have enough land to construct two more factories of 1000TPD each.

So they have land for upto ~3000 TPD (6x of current capacity).

so it isn’t a problem for a good no. of years.

Tar thanks for taking time to reply to my questions. I’m not saying that making solar glass is easy. I understand the competency that Corning has and its reflected product innovation/improvement like gorilla glass. I was wondering that since the margins are so lucrative now and the industry is expanding rapidly will it not attract competition? St Gobain does not have the balance sheet strength, but Asahi has a solid name and resources to enter this segment. Even if this happens still the industry will still be a import substitution play. If I know what to expect then I wont have a knee jerk reaction if this threat materialises.

In this article the second last para reads this "Stressing the need for competition in the Indian solar glass market, a top executive with a large solar module manufacturer said, “We are working on an association for component manufacturers. A lot of people are calling us to start glass manufacturing in India. Borosil is the only manufacturer in India. We are encouraging people who are calling us to start glass manufacturing. I think three to four players will soon start glass manufacturing in India. Triveni Glass, Saint Gobain, and Asahi glass might enter the glass manufacturing business.”

I personally think that BR has a huge lead over others as its the first company to toughen a 2mm thickness glass. This will inturn reduce the weight of the overall panel and increase the life span of the solar modules. I have general philosophy that if I cant find some risk or concern in the business then I’ve not looked hard enough. Hence I’m on this forum seeking knowledge to get my investment thesis sorted.

You maybe right about the point…that there is no entry barrier in the industry as such…and more

players would certainly join the party…but even in that scenario…

the profit pool of the industry would still remain quite concentrated…and BR will always have the first mover’s advantage + economies of scale…because of size… (i imagine a paints industry like scenario playing out where Asian paints was far ahead of all others for decades…in a concentrated industry)

So,in a big pond with limited fish…the big fish is expected to become the biggest…eating other fish’s food(market share) too…

Hi,

I notice that you are invested in strides and also very upbeat on stelis. My question is regarding an IPO. I have been invested in biocon for long term. I was somewhat disappointed that biologics could go IPO route. Consoled myself that I would buy that and reduce biocon. Is something similar going to play out in stelis? I am invested in strides too.

Arunkumar has historically always kept the interest of minority shareholders, as his one of the key priorities, also visible from his past actions of demergers, ex Solara & Sequent & it has also been mentioned that Stelis will be a demerger in one of the call by him.

Also, evident from the fact that it was clearly stated in a past concall that the Sufficient Funding has already been raised for Stelis which is unlike BBIL which will need more capital in future & thus KMS will prefer the IPO route rather than Demerger. There hasn’t been a recent update regarding BBIL so we can assume it will be similar to Syngene.

“So at this stage, as per me, I do not know whether they will go ahead with a vanilla demerger (good for Strides shareholders) or a listing via IPO (not so good for Strides shareholders).”

Can you please explain a bit more on the merits and de-merits of demerger vs listing via IPO for Strides shareholders.