Listing down my portfolio here, would like other investors to opine.

Goal: Compound Wealth for Long Term (30-40 years)

I am in mid 20’s and can take risk and hence the higher weightage to mid and small cap sector. I am also a trained CFA and work in investment banking sector so have knowlege of financial concepts.

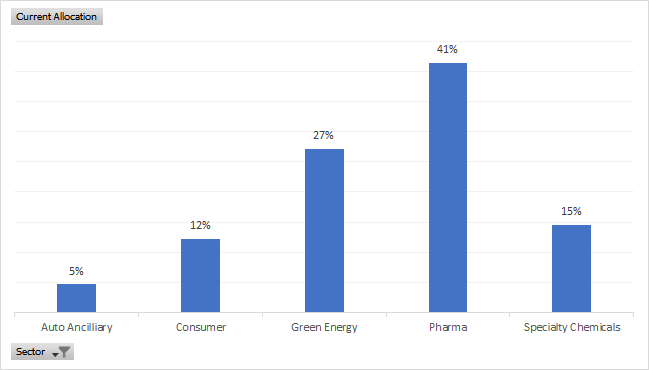

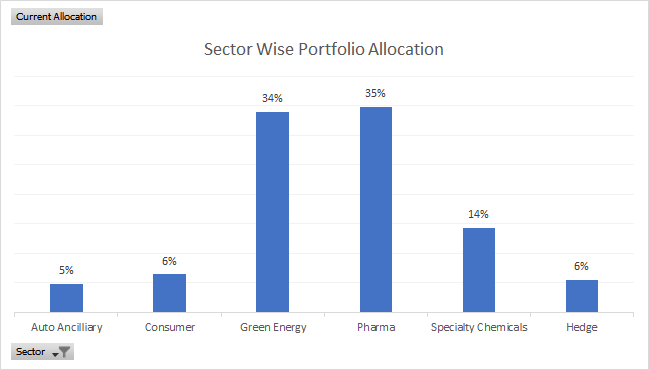

Portfolio: (Most of these stocks were bought in the panic sell of Mar and April. I was buying when others were selling, so have made decent returns in almost all of them.)

- Vinati Organics

- Navin Fluorine

- IOL Chemicals and Pharmaceuticals

- Biocon

- Avanti Feeds

- Kaveri Seed Company

- Laurus Labs

- Divis Labs

- Granules

- Manappuram Finance

- Indian Energy Exchange

- Vodafone Idea

- Tata Power

Rationale for each stock below

Vinati / Navin : based on emerging trends on Speciality Chemicals space globally and in India

IOL : based on their growth, market forces creating disruptions for BASF. They are increasing production capacity to 3x and branching off into other products.

Biocon: their growth in Syngene + Biosimilar story ( I am waiting for Biocon Biologics IPO, will decrease holding in Biocon post IPO and allocate more towards the Biologics)

Avanti Feed and Kaveri Seed: Leaders and borderline monopoly companies. They are set to benefit immensely with the planned upcoming Govt spending on aquaculture + agriculture. I see both the companies are highly undervalued.

Laurus, Divis, Granules : Mixture of 3 high growth large cap, mid cap and small cap companies within the API space. I am only invested in these till Covid related tailwinds dry up. Monitoring them every quarter and don’t plan to sell at all for next 2-3 years. I think the industry is poised to grow at a decent growth rate and may face some consolidation in upcoming years.

Manappuram Finance: NBFC based on India’s rural growth story. It’s easier for NBFCs to create a banking system in rural India and if India needs to become a $5 trillion economy rural sector has to participate more. Manappuram has a second competitive advantage, with interest rates being so low they are able to raise millions of dollars at rates as low as 5-6%. Most of their loans to their customers are at 24-30%. This creates a massive Net Interest Margin for them. Further they operate more efficiently than their other competitor (Muthoot).

Indian Energy Exchange: Monopoly power exchange with consistent return on capital rates of over 40%. The company is set to benefit massively on renewable shift in power sector. Govt of India is also amending policies on how power will be traded in the country. We are moving away from 25 year fixed PPAs to a daily weekly real time exchange system of power. I beleive India will become a world leader in renewable energy esp solar since we are the only country in the world that gets considerable sunlight throughout the year. I expect IEX to continue growing for next 5-10 years.

Vodafone Idea: This was a valuation play. Market noises had beaten the stock down to throw away prices. I started accumulating this at 3 to 4 Rs. Market hasn’t considered the spectrum assets of this company. On just liquidation value alone VIL has more value than the stock represents. Airtel and Jio both has their spectrum expiring in 2021-2022 and will have to spend 40,000 cr each to gain new licences. VILs spectrum only expires in 2030 to 2035. I expect them to get 15 year time period for their AGR dues and bring down significant debt via selling stakes in the company. Further the sector has many tailwinds. VIL can also significantly increase their ARPU above 200 by focusing more on corporate accounts.

Tata Power: This is a fairly small position. I am increasing it as I see the company executing on its forward growth plan. I see the company becoming a renewable first energy company with a leading and possibly a monopoly on EV charging stations in India. They will also benefit from Tata Motors focus on becoming a electric vehicle first company.