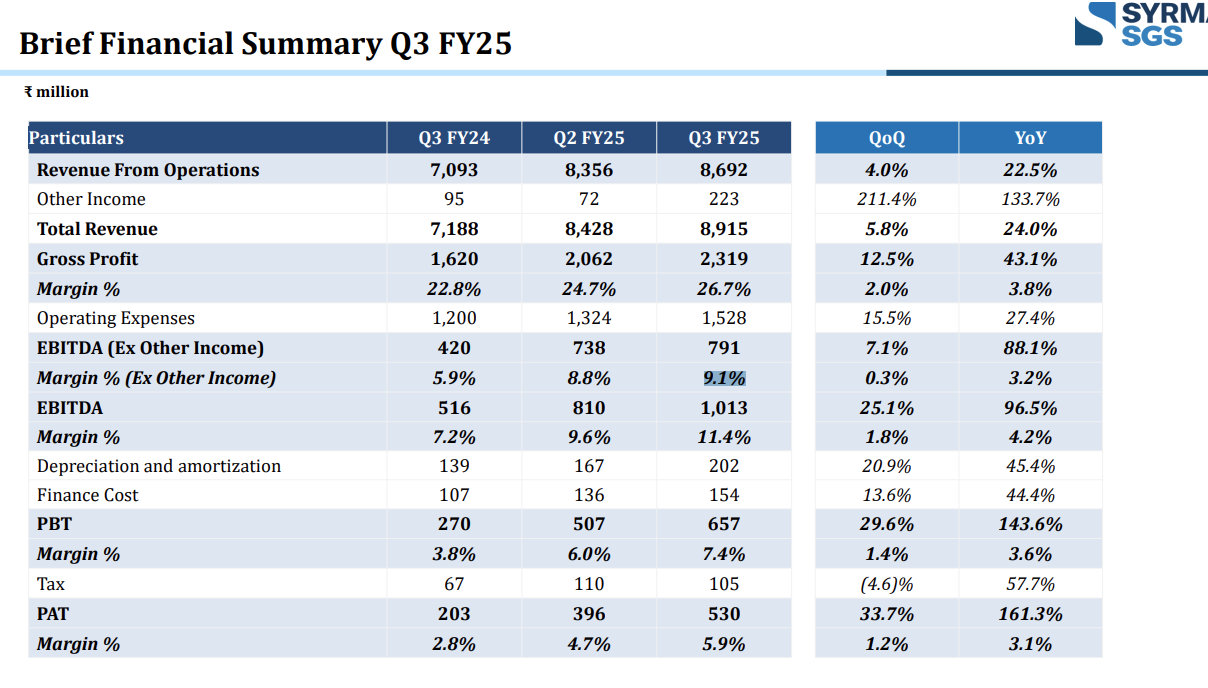

Good set of numbers posted by the Company. PAT increased by more than 2.5x YoY. https://www.bseindia.com/xml-data/corpfiling/AttachLive/44ff7613-495f-4360-983e-bd512ab4961e.pdf

Solid print from Syrma. Probably one of the strongest results in past 6-7 quarters.

- Revenue + 23% YoY

- Gross margins expanded by ~400bps (very impressive)

- Operating EBITDA margins expanded to 9.1% (vs 5.9% in Q3FY24)

- EBITDA +88% YoY

- PBT +144% YoY

- PAT +161% YoY

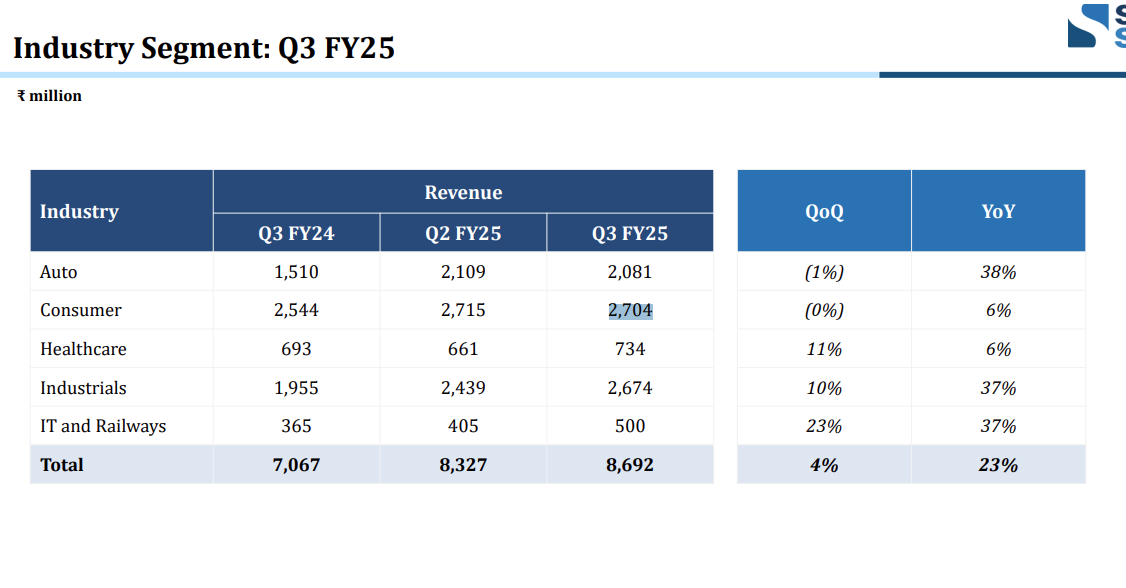

Margin Expansion led by mix change. Consumer segment was the pain point in the business which was pulling the margins down. Co seem to have reduced growth in consumer segment.

- Lower margin Consumer segment grew only 6% YoY

- Higher margins segments (Auto + Healthcare + Industrial + IT & Railway) grew 33% YoY

- This mix change towards higher margin segment has led to margin expanison.

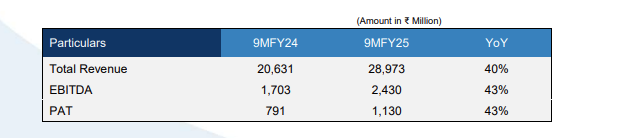

- While quarter to quarter there is variability in margins due mix change, 9MFY25 results look very balanced with 40%/43%/43% Revenue/EBITDA/PAT growth

9 Likes

Management did not increase the EBITDA margin for FY 25 and FY 26 from 7% and they expect a revenue of 5200-5500 Cr in FY 26 which is hardly 15-20% growth YoY. I don’t see how they can maintain 30%+ growth moving forward.

2 Likes

Just my assumption, management is very well understood by the underperformance that the market awards or is driven by the profitability. Hence, the outright focus is on improving the EBITDA margin. They will not focus on high-revenue, low-margin consumer business and chase the revenue; rather, they will focus on high - margin automotive, medtech, or industrial business.

I won’t be surprised if their EBITDA margin inches to 8% in FY26 due to the change in product mix and the benefits of operating leverage kicking in.

If they do a a revenue of 4400cr and would grow by 25% yoy to reach the revenue of 5500cr. The PAT margin of 5% will result in PAT of 275cr (60% yoy) and EPS of 15.4INR. I am more happy with Margin expansion than merely a inflated revenue growth.

Disclosure: Invested and Biased

4 Likes

Please listen once more to earnings call - particulalry the response to questions asked by Mr. Bharat Shah. ![]()

Once transcript is avilable, will share exact excerpts. Here is the AI generated summary in meantime:

Based on the Youtube recording of earnigs call, here’s a summary of the questions asked by Bharat Shah during the Sirma SGS Technology Q3 FY25 earnings conference call:

• Clarification on EBITDA Margin: Bharat Shah sought clarification on whether the stated 7% EBITDA margin actually referred to the operating profit margin, excluding other income. The management confirmed that it was indeed the operating profit margin, with other income being over and above that

• Turnover Outlook: He inquired about the previously discussed turnover of around 6,000* *crores and whether that figure was still intact. The management responded that there might be a slight variation in the turnover but the EBITDA margins guided on the basis of a 6,000 crore revenue would remain intact → My interpretation is that this means managment indirectly hnted towards EBITDA of 420 crores+ for FY26 (6,000x7%; although actual margin might be different). For FY25, management has guided for 300-310 crores of EBITDA. Hence FY26 could see 40% EBITDA growth - which is very attractive.

• Capital Efficiency and Return on Capital Employed (RoCE): He questioned the progress being made on capital efficiency, specifically regarding the target of keeping working capital below 60 days, and if new facilities, hiring, and other investments would lead to a measurable improvement in RoCE4… The management confirmed they were targeting an RoCE of 14 to 15% for the current year, with a goal of moving towards 20% over the next two years

• Capacity and Infrastructure: Bharat Shah asked if the company would need to raise physical infrastructure to meet the growth targets, considering the potential to achieve a turnover of 6,500 crores with current infrastructure

• Tax Rate: Bharat Shah inquired about the likely tax rate for the current year, and the management replied that it would be around 23-25%, though it may be lower for the current quarter due to other income with lower capital gains tax

Syrma SGS | Management Interview

- On track to achieve EBITDA margin of 7% for FY25

- Company expects to grow at industry average of 30-35% in FY26.

- Company expects exports to cross the Rs 1,000 cr mark in FY26.

Watch the management interview here

2 Likes

On his Interview and Page 7 of 26 of last concall:

Question: Sir, my question is on the margin profile improvement that we have seen. You know, if I see your order book composition, I think auto and consumer continues to be almost 60 to 70% of your order backlog. So, is it that incremental order that you all are taking are at a better margin or what would we really attribute to the margin improvement over here?

Answer: See, the margin improvement, as I have all the time been saying, is a function of the product mix which we sell. For example, in Q3, my consumer business is only 31%, high-volume consumer business, which is a tight-margin business, whereas my industrial business is 30% for three months against the average of 25% for 9 months. My automotive is 24% of my revenue for this quarter comes from automotive. For 9 months it is 21%.So, the product mix change results in this change in the margin profile. And as I had said earlier that for this year we are guiding, we have targeted about 40% of our revenue coming in from consumer business. The wish and the desire of the management on which we are working with a very focused strategy is to bring this high-volume business to about 35% of our revenue. I would be happy with 30%. But I don’t see it happening immediately. If it comes down to 35, it will have a natural positive impact on the margins.

Change whole business is depends on the product mix. The Management is near to delivered Revenue guidance 40-45% and EBITDA 300-310. The Next year guidance of 5000-5500 Cr revenue and MINIMUM 7% EBITDA margin. (Translate ~ 350-370 Cr)

5 Likes

1 Like

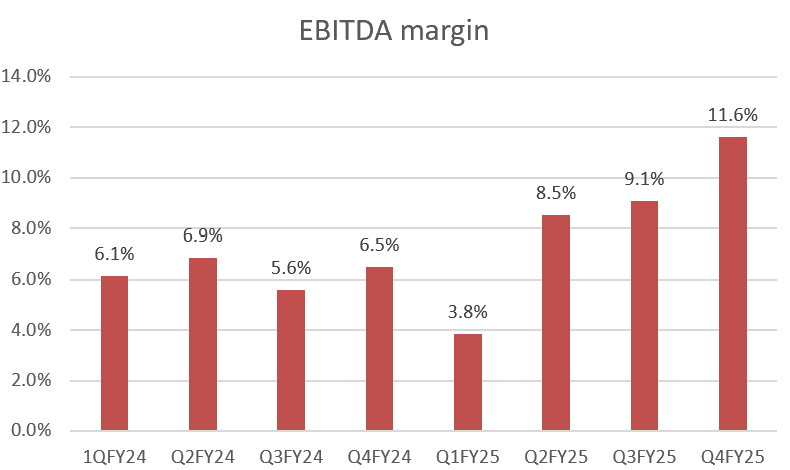

Q4 Results are out.

- Revenue -18%

- EBITDA +44%

- EBITDA margins have expanded very sharply to 11.6% vs 6.5%

- Absolute EBITDA for the year closed at ~302 crores inline with guidance shared by mgmt earlier

- PAT +58%

Seems likely some product mix change or discountinuation of loss making or low margin product. This could epxlain why EBITDA and PAT have grown sharply even though revenue is down for the quarter.

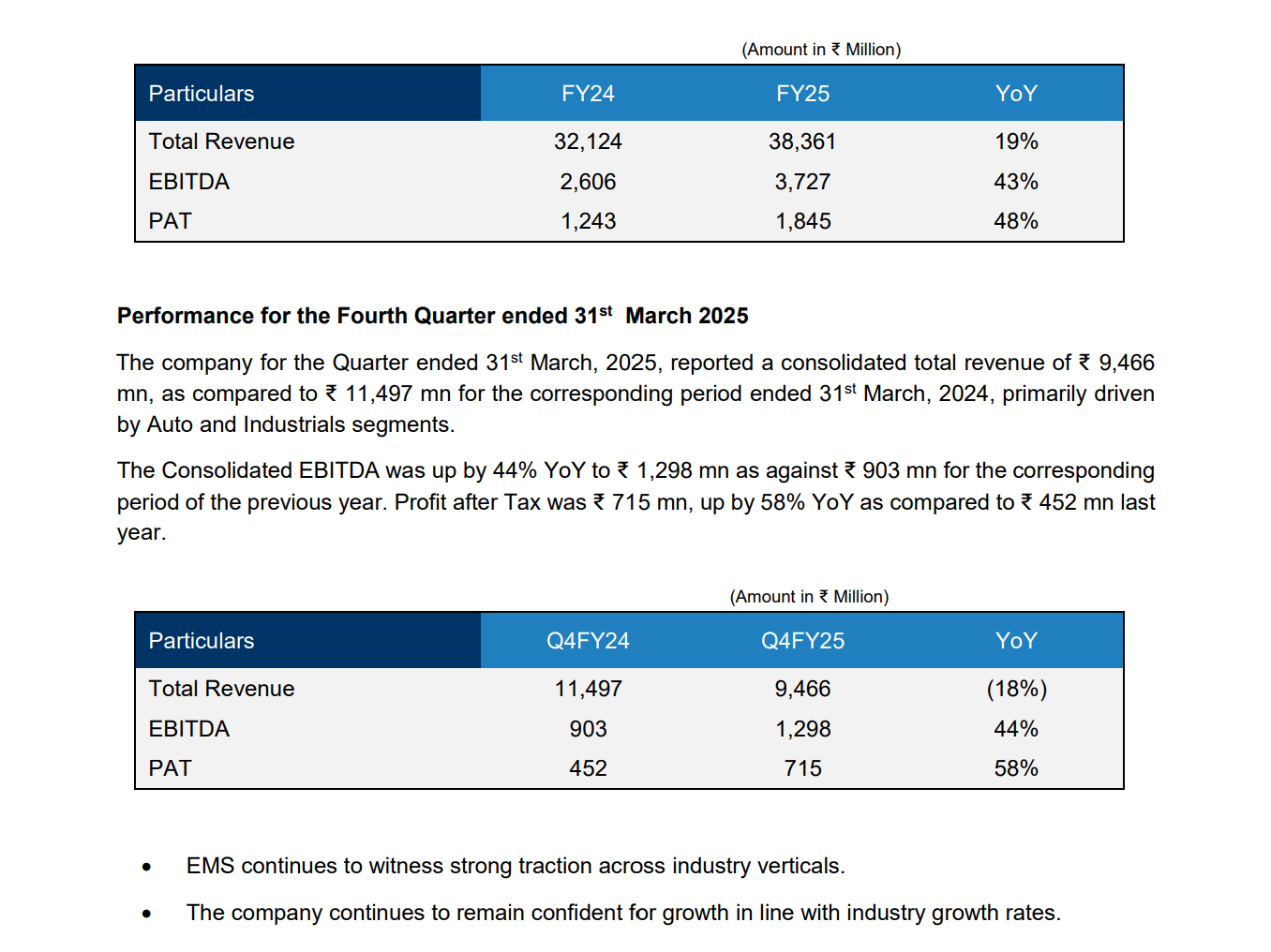

FY25 full year performance

- Revenue +19%

- EBITDA +43%

- PAT +48%

2 Likes

1 Like

Syrma SGS to raise 1000cr via QIP.

Inorganic growth is around the corner as hinted by the management.

See last few mins of this video

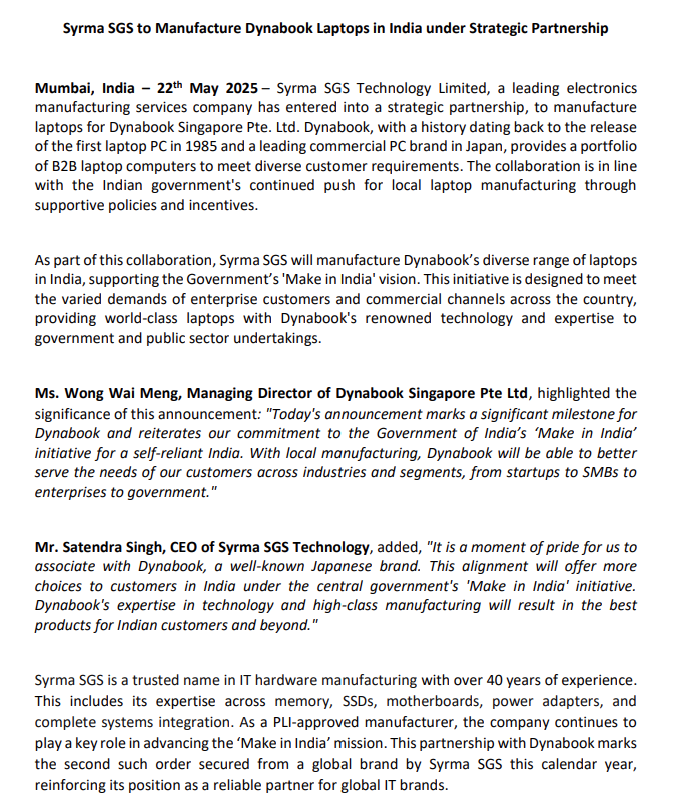

Added 2nd big customer in Laptops

As of FY 2022, Dynabook is the fifth largest PC vendor in Japan with a market share of 8%, trailing FCCL (Fujitsu), Dell, HP, and the leader NEC-Lenovo Group.

6 Likes

Anti dumping duty imposed for 5 years on import of PCB.Syrma assembles PCB. I am not suggesting that it will have favorable impacts on Syrma. Anti-dumping Duty Sparks PCB Manufacturing Surge in India, But Long-term Gains Hinge on Raw Material Independence: Ind-Ra

5 Likes

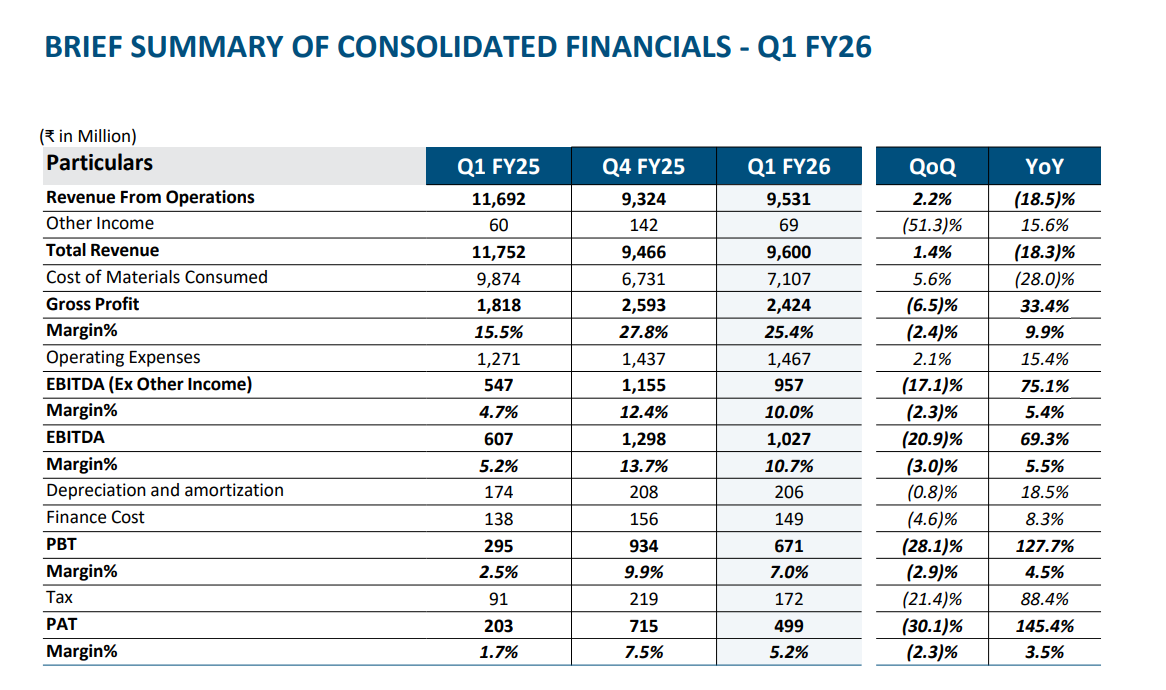

Q1FY26 Results

Revenue -18% YoY

- Industrial and Auto verticals (high margin) grew

- COnsumer (lowe margin) declined sharply

Gross Profits +33% YoY

- Gross margins expanded sharply as a result of mix change towards high margin

EBITDA +75% YoY

PBT +127% YoY

PAT +145% YoY

11 Likes

- Andhra Pradesh Govt allots 26.70 acres to the company at Menakuru Village, Naidupeta

- Land allotted to set up a manufacturing & R&D facility for single, multilayer, HDI & flex printed circuit boards

- Company to invest up to ₹1,595 Cr for all projects in Andhra Pradesh

- Capacity Expansion & Diversification – The new manufacturing and R&D facility strengthens Syrma’s capabilities in advanced PCBs (single, multilayer, HDI, flex), allowing them to tap into higher-value electronics segments.

- Strategic Location Advantage – Andhra Pradesh offers industrial incentives, skilled manpower, and logistics benefits (close to Chennai/Bengaluru hubs), boosting competitiveness.

- Long-Term Growth Commitment – With a large ₹1,595 Cr investment plan, Syrma signals strong growth intent, which can improve customer confidence, enhance order pipeline, and attract new partnerships.

3 Likes

5 Likes

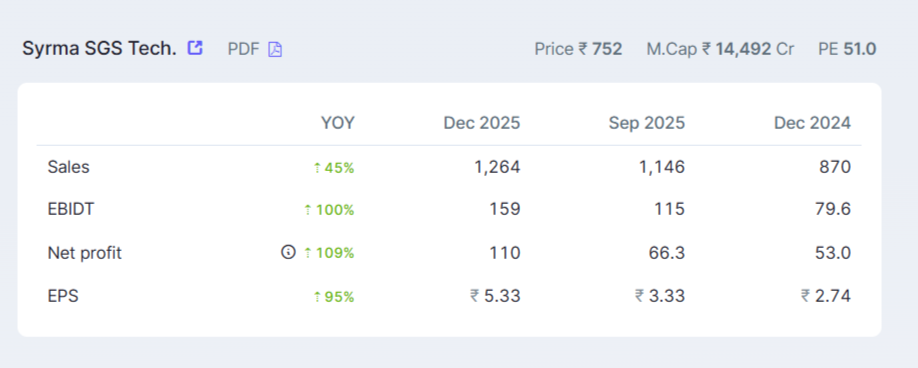

Has the company given EBDITA target for FY27. Any Revenue guidance for Next 3-4 year time frame?