FY15 PAT was Rs.175 crore and FY20 PAT is Rs.412.10 crore which gives me a 5 year CAGR of 18.68 %. What am I missing?

Syngene International_Investor Presentation_July 21, 2020.pdf (2.2 MB)

Please have a look at page 17 of presentation.

2 Likes

2 Likes

Hi can u share your thoughts on why there was revenue growth fall in 17/18 is it due to fire incident or any other reason. Thanks in adavance

AGM proceedings and management reply to queries.

8 Likes

3 Likes

Results for the half year.

Results looks okay. Valuation is expensive.

Trade receivables have increased. Also company has borrowed long term loan. The rate of interest needs to be checked

9033068c-5b65-4077-935c-a2b6d5600d15.pdf (994.7 KB)

1 Like

Annual report excerpt detailing the syngene. worth a look

2 Likes

Syngene Q2FY21 Earnings Call: Key Takeaways

I will be dividing this into Business, risk and management

Business

-Credit Rating has been upgraded by ICRA on back of the upgrade by Crisil in the last quarter.

-Topline was up by 12% (YOY) and 23% on QoQ basis.

-Margins remained at 32% and experienced 150BPS reduction in expenses primarily due to power cost and RM cost coming down, and change in mix of the business.

-Staff cost increased by 22% to 161 crores as compared to 132 Crores last year, which led to a 15% increase in employee cost.

-Currently we have 5200 employees as compared to 4700 employees last year

-Mangalore API Plant has started accruing operating expenses. The last 2 years were spent in building the plant and the current year will be spent in validations, audits, etc. From next year onwards, we will talk about the growth prospects and utilization of the facility.

-Excluding other income, EBITDA margins at 30% in the first half of the financial year, which is an improvement of 1% as compared to the last financial year.

-Operating losses in the newly commissioned Mangalore plant and the decline in interest income, contributed to 200bps reduction in tax rates and other 200bps reduction in tax rates came from the reversal of tax position from earlier years. The effective tax rate was at 11%.

-PAT margin came in at 16% vs 17% YOY. Impacted due to depreciation and lower interest income.

-Capex incurred was $26million: (Capex break up)

1)$7million on the Mangalore API plant

2)$8million in the discovery business

3)$3million on the biologics facility

4)$8million on dedicated centres and development business.

Currently, $450 million in fixed assets (inclusive of $32million in assets under construction), earlier plans of closing the financial year with $550 million of fixed assets might spill over to the next year. In long term our Asset turnover would likely be at 1x.

-Since, most of the receipts are in $, we can borrow US Dollar-denominated money without posing risks. Interest rates are very low, decided to refinance the $50 million loan that we repaid last year during this quarter to strengthen liquidity.

-Near full operating capacity in spite of covid. If the interest income is taken out, operating EBITDA, we had EBITDA Margin improvement. Revenue has grown faster than the costs by a bit, but large gap would only be visible once operating leverage kicks in.

-On Agchem, Animal Health and Speciality Chemical Business

1)Don’t do a great deal in manufacturing in Animal health, Spechem, and Animal Health.

2)Our role is front-ended (Providing quality research etc)

3)In Animal Health, due to the margin structure customers are very cost-sensitive. We can create value for them as India provides low-cost advantages.

4)On Agchem, it’s more of a sideline work than a major driver. Not a good fit for us, as it is scale based+High capex industrial approach.

Management

-Think long term do not go by quarters. Think of how Asset will develop over next 30 years rather than next few quarters. (When Asked about for a guidance from Mangalore API Plant)

-We don’t think we have reached half way in terms of industry potential.

-On potential conflict of interest with Biocon being in novel biologics: That was a question asked 20 years ago, not been a relevant question since the last decade as we operate independently.

-Expect to meet the guidance of low Revenue growth and Flat PAT levels by the end of the FY. Expect to continue the momentum that has been built up in the first half to the second half of the year.

My view in terms of risks: business has been re-rated ahead of the eventual earnings growth and ROCE expansion in the next 2-3 years. However, what most people fail to realize is that the manufacturing of patented molecules is inherently a lumpy business. Given the recent commercialization of the Mangalore plant, it can take some time for it to reflect in revenues and achieve utilization levels. Any disappointment can lead to some correction. For a long term investor, the business is well poised, and as @basumallick recently pointed in a post, that tailwinds, favorable economics, business, and stock momentum create a Lollapalooza effect which propels the returns.

Disclosure: Invested in Syngene, Pi Industries, Divis, Suven, and Navin Fluorine. Not a recommendation to buy/sell as I am already biased.

25 Likes

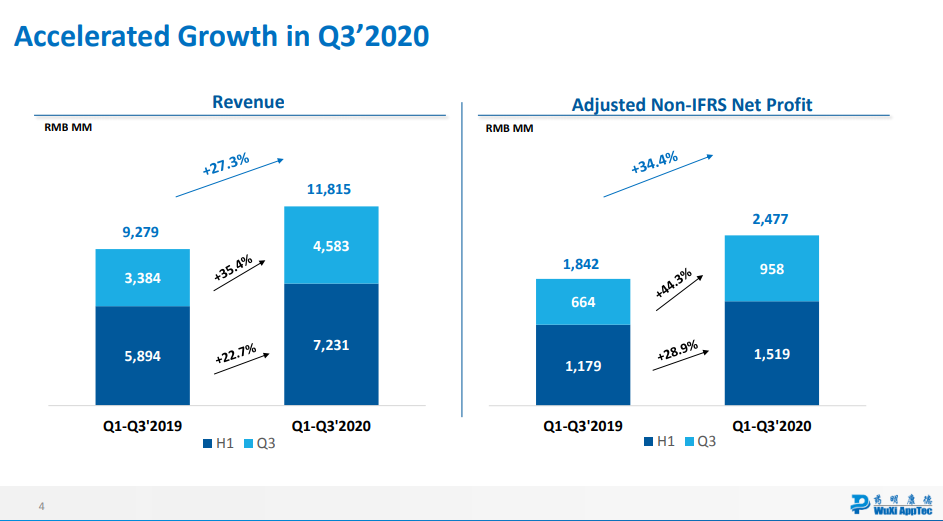

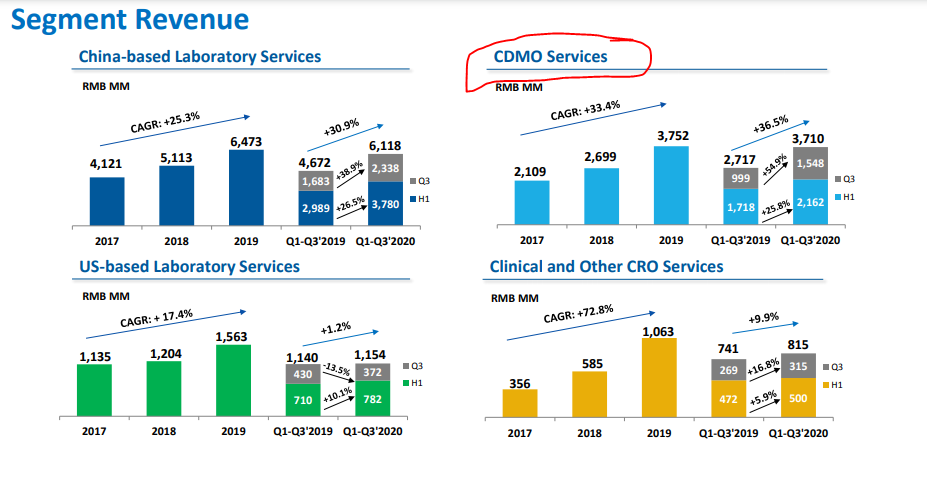

Syngene’s China counterpart WuXi AppTec (which is a much larger player) reported solid 3Q20 earnings and they look much better vs. Syngene’s. (link to 3Q20 earnings presentation)

Segment wise:

- China based lab service and CDMO service continue to do well, growing at 35%+ in 3Q20.

- Clinical and other CRO service up 17%

- US based lab service down 13.5% (vs. +10% in 1H) (this could be interesting development, need to understand this more deeply)

I might be wrong in my assessment but I don’t think China-to-India shift story in pharma CRAMS/CDMO is playing out in the near-term after looking at these numbers.

Would like to invite @Worldlywiseinvestors and other senior VP members to comment on this.

Disclosure: This is not an investment advise. Do your own research before investing.

5 Likes

Wuxi is way ahead in its journey, Syngene has only recently entered manufacturing in a big way with the capitalization of the Mangalore API plant. This is not just about the shift from China to India, as you rightly pointed out some credible Chinese players like Lianhe Chemicals, Wuxi Apptech and Wuxi biologics have exceedingly done well. Business is shifting from western CRO/Cdmo’s(such is the nature of the industry that bigger western CDMOs are likely to maintain their business due to very sticky relationships), increased outsourcing due to cost differences is what is playing out. India will be beneficiary of the China+1 policy,

However, what is important to realize is that in Patented Crams it isn’t a 1 or 2 quarter trend. It will take 2-3 years to fully reflect in numbers or possibly longer. Some businesses like Suven Pharma have categorically denied that they are seeing benefits of Chinese disruptions. On the other hand, for some like Navin Fluorine enquiries have substantially increased.

11 Likes

Syngene International: The company has signed an agreement with Deerfield Discovery and Development Corporation (3DC) to collaborate for five years to advance therapeutic discovery projects. The collaboration is to advance the therapeutic discovery projects from target validation through to pharmacological proof of concept and pre-clinical evaluation.

Discl - invested

3 Likes

https://repositive.io/blog/post/repositive-further-expands-global-network-with-cro-from-indi

Interesting new tie up of Syngene with Repositive

1…Cancer Model Platform

When you want instant access to browse cancer models available globally, our online platform presents the world’s largest cancer models inventory compiled of over 8000+ models available from our 21 CRO partners. Our platform gives your team a powerful tool to browse for suitable models to plan their experiments without delay. Give your whole team a tool to browse for suitable models in real time to plan their experiments.

2…Cancer Models Scout

A concierge search conducted by our expert team

We conduct a comprehensive search based on a well-defined scope of your needs and results are delivered within 2-4 weeks in a data-rich report of all identified matching models across CROs in our network. Let us do all the heavy lifting for you by activating our expert team.

Disclosure invested

3 Likes

I see that the ‘share capital’ has increased from 3 Cr. in Mar’11 to 400 Cr. in Mar’20 - Does this mean the management has issued fresh/new shares into the market to raise capital?

Could you someone help me understand whethere such a consistent increase in share capital, is considered good or bad?

If you see the capex I.e the Fixed asset growth you can understand the reason for increase in capital

This company is in expansion mode so naturally they require funds to aid the capex.

2015 IPO @ 250 and in 2019 1 to 1 bonus that’s how share capital is increased.

It’s a capital intinsive business but observe there working capital since few years and compare to any CRO/CDMO business you will be surprised that’s there efficiency This efficiency help them to repay there debt

Thanks

Invested and obviously biased

3 Likes

Syngene a long term play!

5 Likes

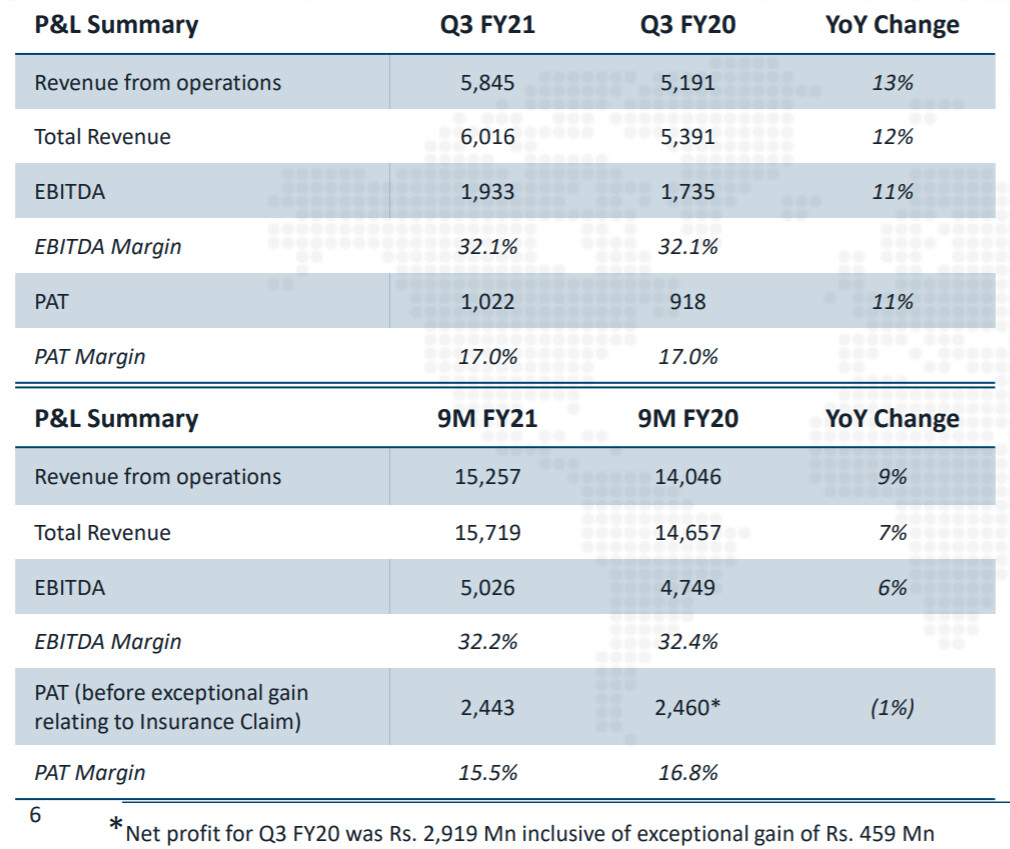

Q3 FY21 revenue from operations up 13% year-on-year

Q3 FY21 EBITDA growth of 11% year-on-year and EBITDA

margin at 32%

PAT growth of 11% year-on-year

3 Likes