@sethufan

Yes FY15 figures are available in RHP but since FY15 figures of its Indian peers are not available, chose to provide figures till FY14 only…

Will not like to comment on valuation as I am a firm believer of the fact that “beauty lies in the eyes of beholder”, however, Have personally studied deeply similar companies before… first Divis and then PI Ind…Some views from my end :

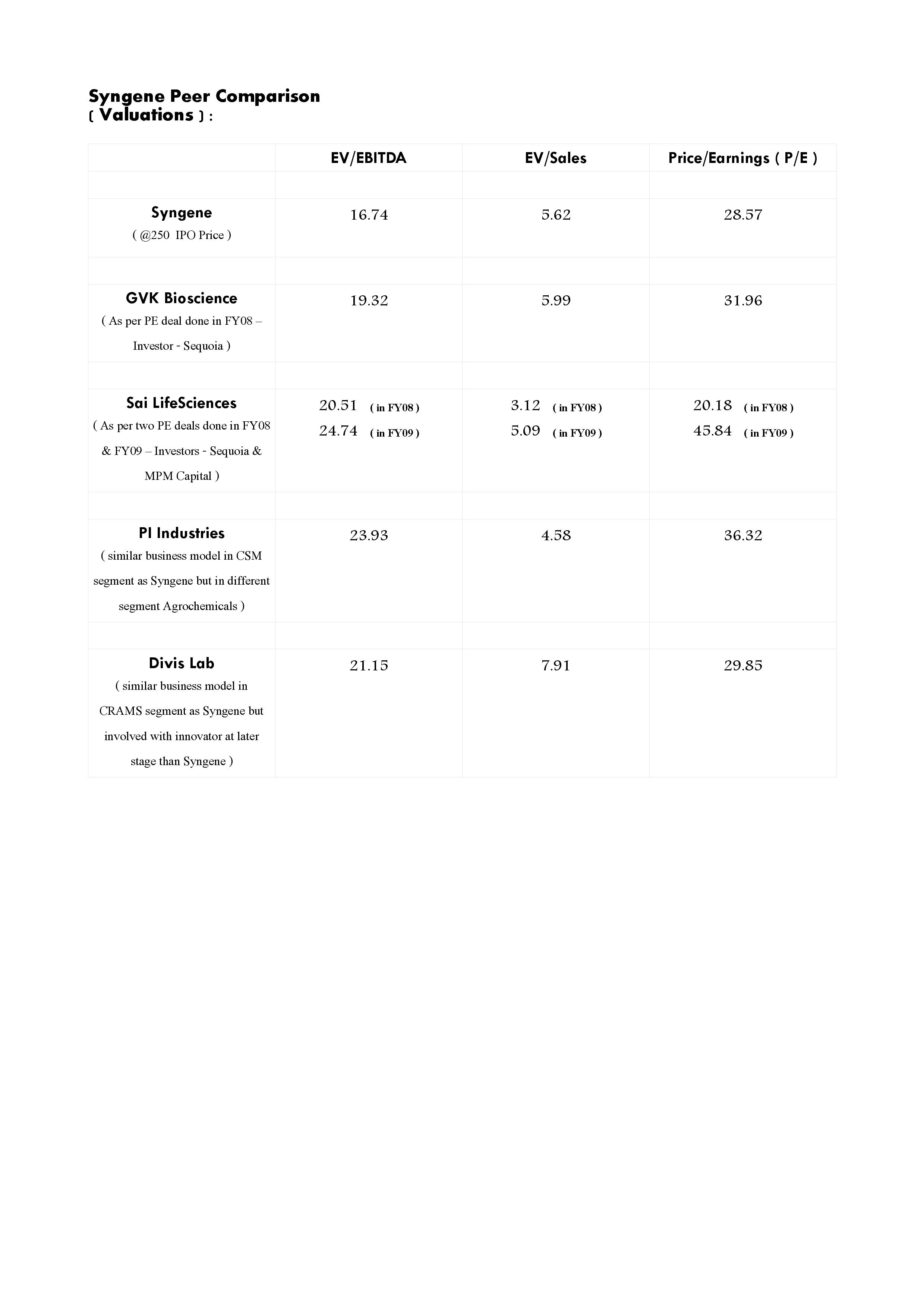

(1) Once listed, Syngene could become a unique company which might not have any comparable peers…its business model’s closest match in the listed space is PI Ind.'s CSM segment model, but its in a different space i.e. agrochemicals…Both have a singular focus and that is New Molecules…however, PI is involved with innovator at a later stage i.e. at process research stage whereas Syngene is involved from very beginning at discovery stage…Once custom manufacturing starts, Syngene will be present right across the lifecycle of a New Molecule…

Divis is also similar and that too in Pharma space but it has generic exposure too and like PI, it is involved with the innovator at a later stage than Syngene.

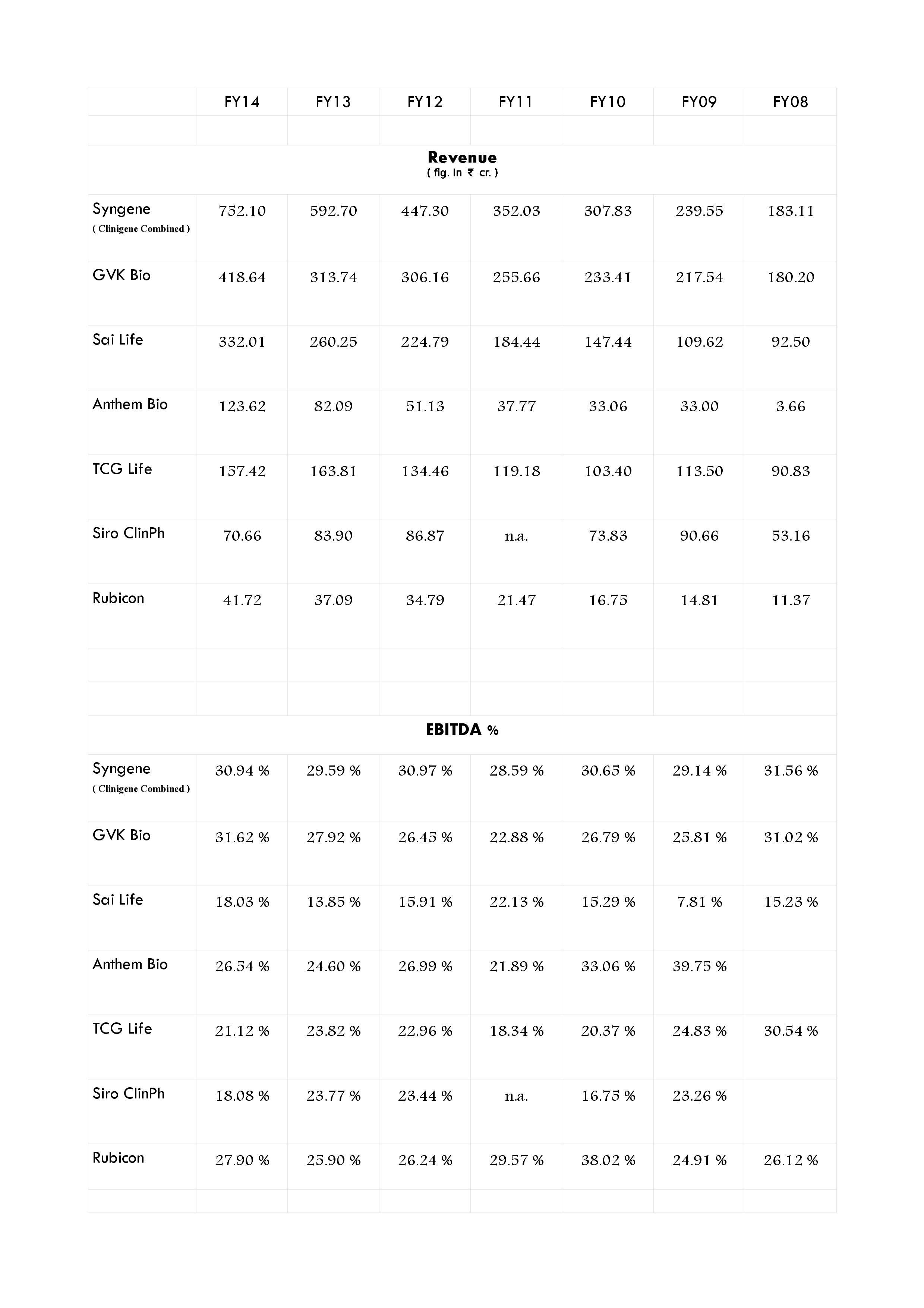

(2) In unlisted space the closest Indian match is GVK Bioscience but it is also involved in generic space especially via its subsidiary Inogent Lab.

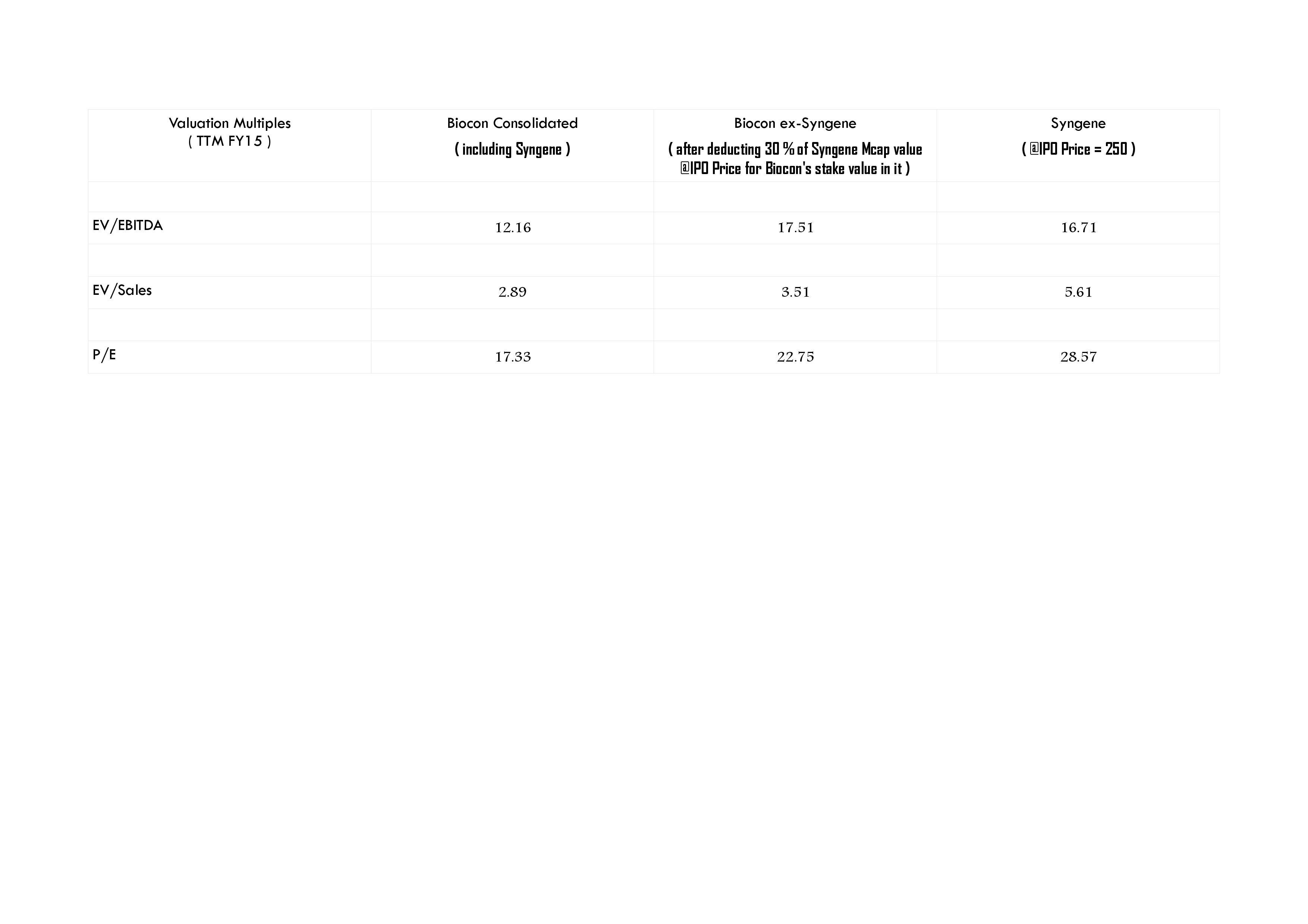

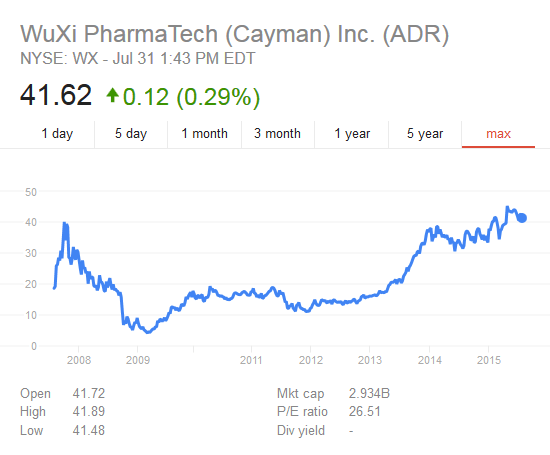

(3) Post listing, it will not only be India’s only pure-play CRO+CRAMS focussing on new molecules but also Asia’s largest listed company in the space as the only bigger peer Wuxi is getting delisted soon (delisting price @23.73xTTM EV/EBITDA & 4.45x TTM EV/Sales & 29.31 TTM P/E).

(4) The beauty of this business model is that once you are into commercial manufacturing of a New Molecule, your failure is more detrimental to your client than yourself…This is because, normally, an innovator doesn’t keep more than two to three suppliers in the initial years of commercial launch of its patented product. So, a supplier gets long term contract inplace with good margins and there is no threat of generic for atleast 6-10 years…So with the success of innovator, supplier also flourishes whereas in case of remote chance of failure of the molecule post launch, you have minimum compensation clause inplace which protects the supplier.

(5) If we talk specifically for Syngene, then it has already signed contracts for three molecules which are under process of commercial launch out of which for one supply might start by FY17…However, stabilisation takes time and we might be able to see the real benefit of this only starting 2HFY18…

(6) Syngene has lined up ~1200 cr. CAPEX over next three years…Key is how well it manages this CAPEX…if it can manage this by judicious mix of internal accruals, debt as well as equity then this company has the potential to be a good wealth creator…

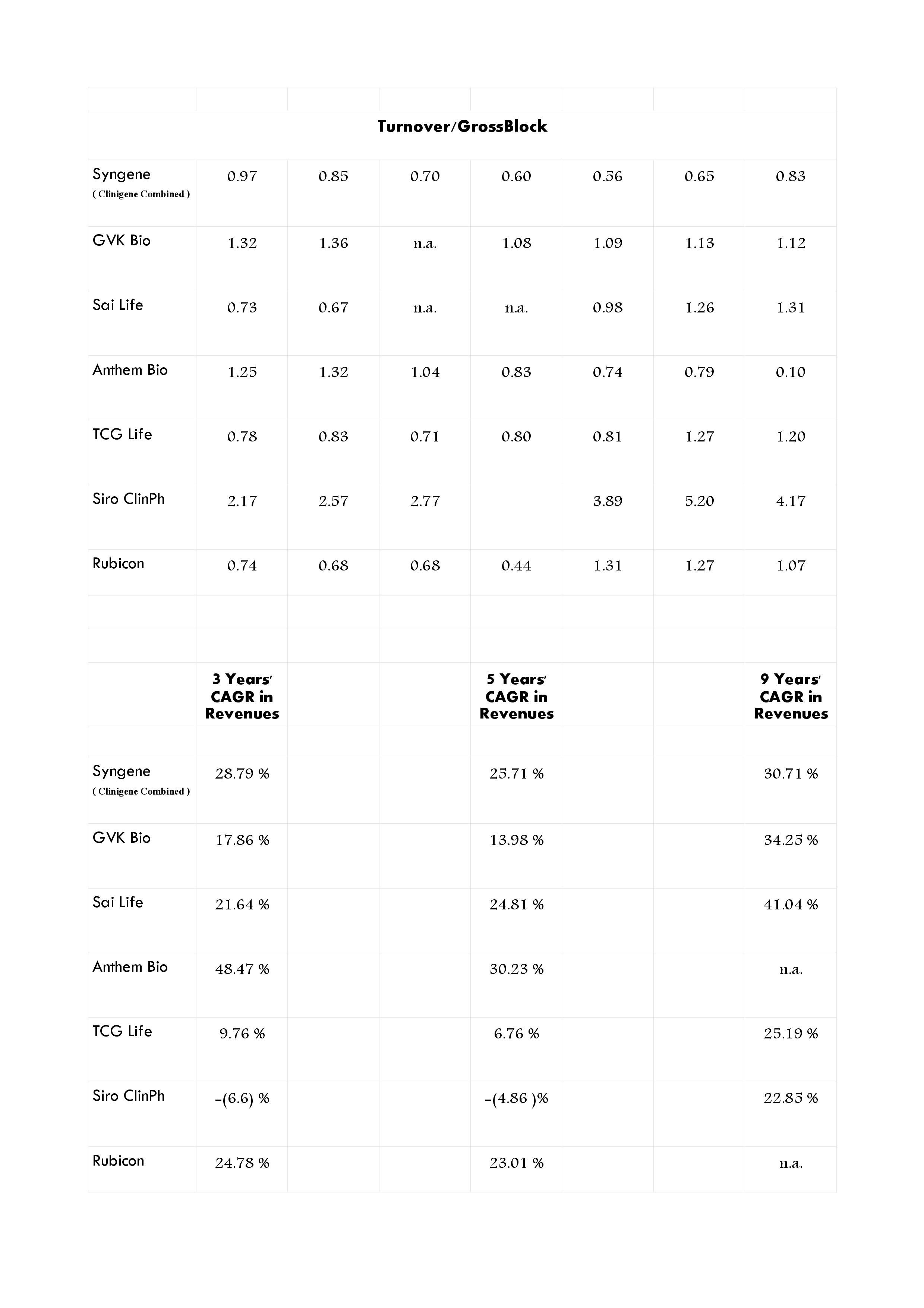

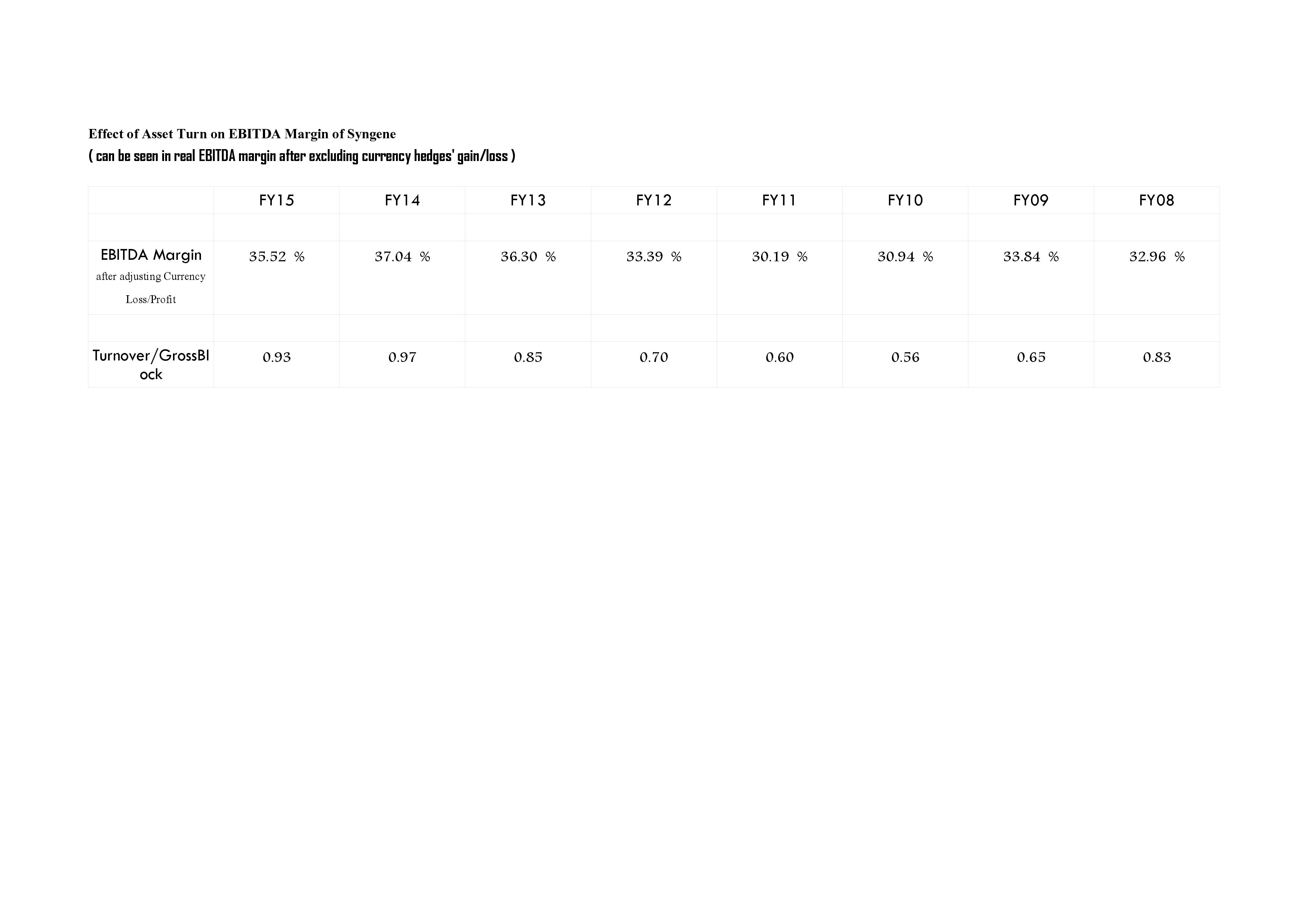

(7) Asset turn is key to margins and with Syngene only at 0.93 with a scope to reach 1.2-1.3 post stabilisation, margins might be very healthy post stabilisation phase of CAPEX…Initially, although management has guided for blended EBITDA margins of 30 % in the analyst meet but I expect a blended EBITDA margin of 27-29 % considering the pace of CAPEX and the fact that manufacturing might only command at best 24-26 % margins in first two years.

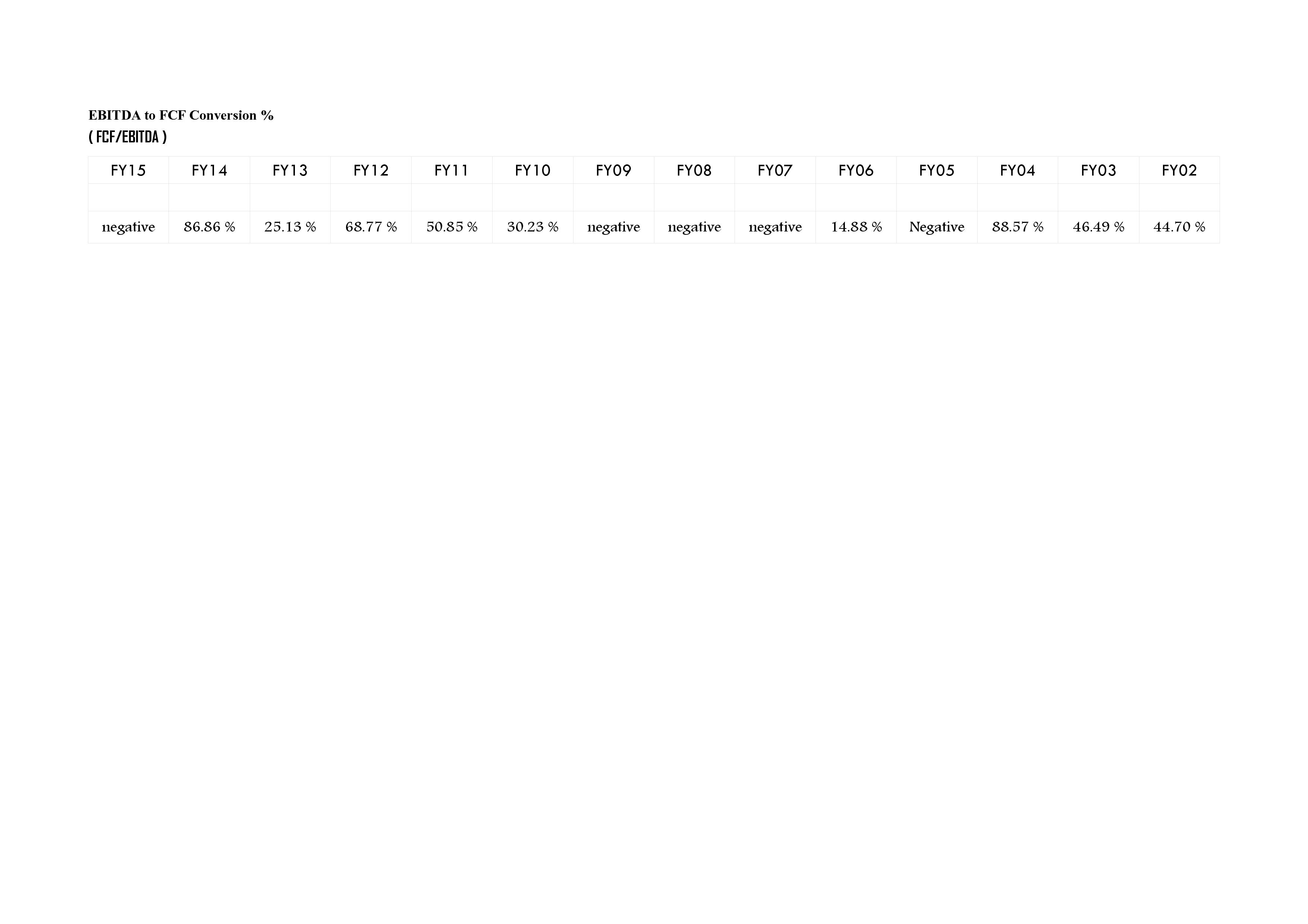

Regarding ‘money guzzler’, yes its a business requires continuous CAPEX to support your clients and asset turns in this business are low at only max 1.2-1.5 ; however, as compared to other CAPEX, this businesss CAPEX is normally backed by firm contracts and offtake post commercialisation of NME usually rises gradually for first 6-8 years atleast…in addition, margins in this business are relatively high which more than compensates for upfront CAPEX you incur…Let’s have a look at EBITDA to Fee Cash Flow conversion of Syngene (Clinigene combined) for last 14 years – the maximum data I have…

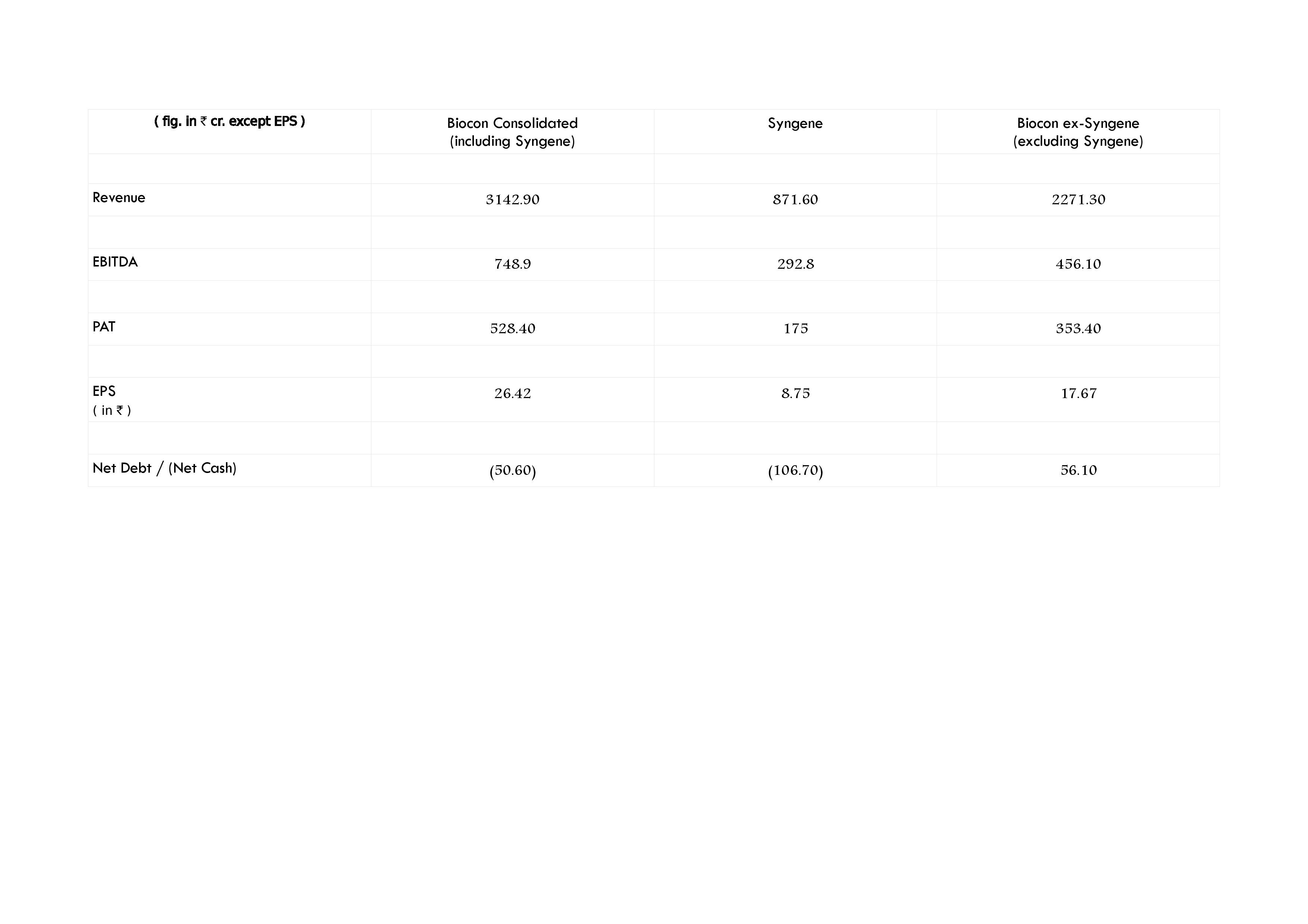

Lastly, not a single paisa of INR 550 cr. raised via this IPO is going to be used for Syngene business…entire proceeds go to its parent Biocon to invest in its own other businesses ex-Syngene.

Rgds.

Discl.- Subscribed to IPO.