Short Term market movements have no relationship with Long Term movements in a stock.

For a stock to move it needs catalysts and triggers. These triggers are usually change in fundamentals, any news related to the company etc.

For eg, Biocon’s stock went from 500 odd to sub 400 in a few days on the news that Biologics CEO has resigned.

Short term movements are pure speculation and no one can make sense of why a stock may fall or go up in the short term.

Don’t play the short term game, invest for the long term and let market over/under react in the short term.

Syngene’s long term fundamentals remain strong and nothing has changed fundamentally in the company.

Syngene offers outsourced services to support discovery and development for organizations across industrial sectors like pharmaceuticals, biopharmaceuticals, nutraceuticals, animal health, agro-chemicals, etc. It currently caters to 293 global players including Bristol-Myers Squibb (BMS), Abbott, Baxter and Amgen, among others.

Segmental Growth Year on Year from past 3 years

CRAMS and R&D growth, Biologics is also in line for growth traction sequentially Revenue increased 13% YoY to INR17.5b (in-line) in FY20, mainly led by strong growth in Biologics (+31% YoY, 34% of sales) and Small Molecules (+16% YoY, 31% of sales). Research Services (30% of sales) grew 11% YoY to INR5.2b. However, Branded Formulations (9% of sales) de-grew by 26% YoY.

Increase in number of Clients

Capital Expenditure

On a US$550 million program that was spread over multiple years, the last year of which is FY21, it’s expected to be fully invested with all US$550 million by the end of this year. During the last 12 months, the company added US$108 million of that capex. With this capital infusion, company’s fixed assets currently stand at US$425 million. This includes an asset under construction of US$70 million.

Company is very much on track to have a total asset base of US$550 million by the end of FY21. Capex in FY20 stood at 108mn USD, of which

• 43mn USD in API

• 28mn USD in Discovery

• 12mn in Biologics

• 25mn USD in others

• Total gross block stands at 451mn USD including 33mn USD of CWIP

• It commissioned a new research facility (152K sq. ft.) supporting biology, QC microbiology and other research domains.

• It is currently working at 70% utilization and expects to hit 100% by end of May.

• It expects to achieve at least 1x asset turnover with revenue build-up by second year of asset.

• Revenue build-up for manufacturing will take longer.

Scientist Count

Scientist strength addition, the company has typically added between 450 to 500 people on an annual basis over the last five years. Now in FY20, the company added about 240 to 250 people. Syngene still has large room to grow in terms of scientists.

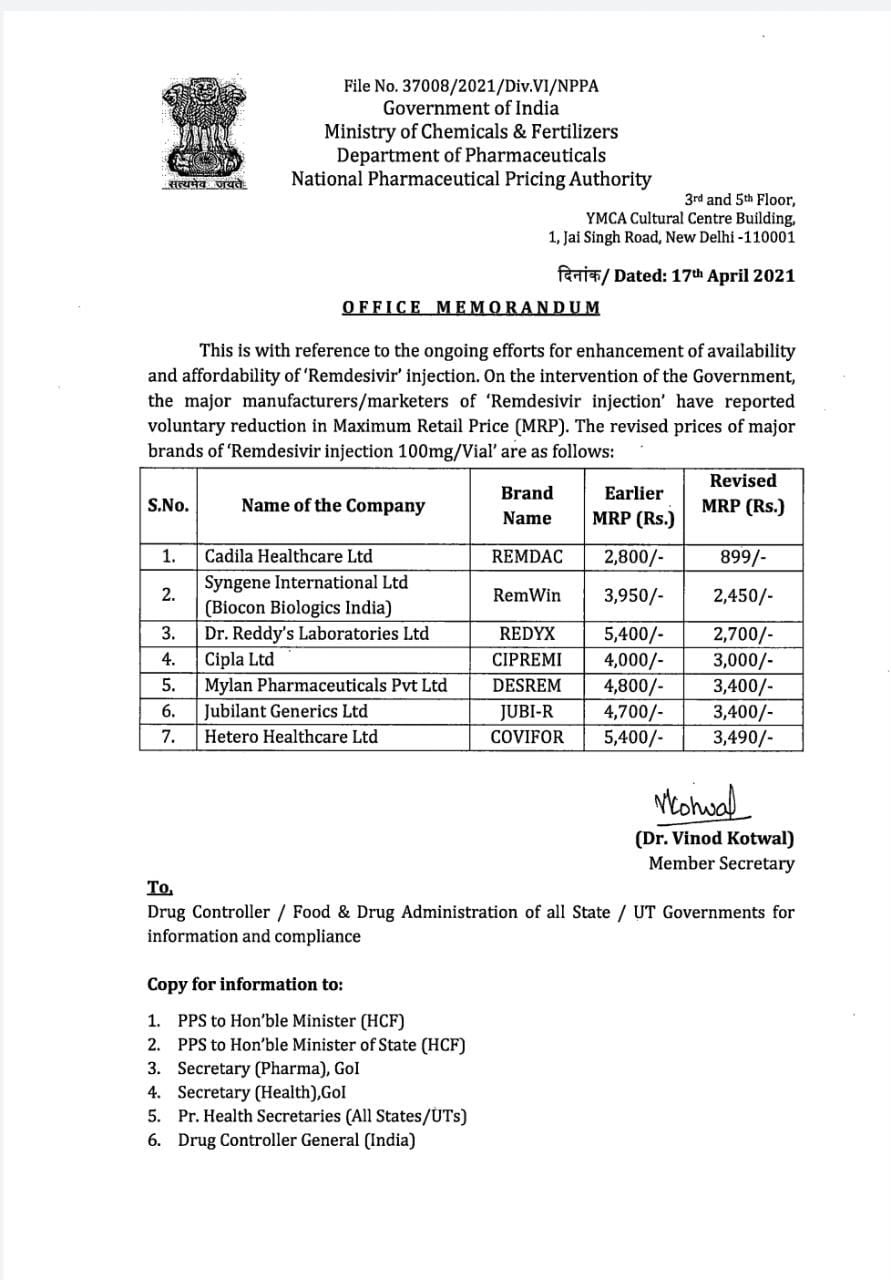

While Govt wants to scale up production of Remdesivir, that have capped MRP as well.

Can Syngene multiply their manufacturing ?

What is an adjuvant and why is it added to a vaccine?

An adjuvant is an ingredient used in some vaccines that helps create a stronger immune response in people receiving the vaccine. In other words, adjuvants help vaccines work better. Some vaccines that are made from weakened or killed germs contain naturally occurring adjuvants and help the body produce a strong protective immune response. However, most vaccines developed today include just small components of germs, such as their proteins, rather than the entire virus or bacteria. Adjuvants help the body to produce an immune response strong enough to protect the person from the disease he or she is being vaccinated against. Adjuvanted vaccines can cause more local reactions (such as redness, swelling, and pain at the injection site) and more systemic reactions (such as fever, chills and body aches) than non-adjuvanted vaccines

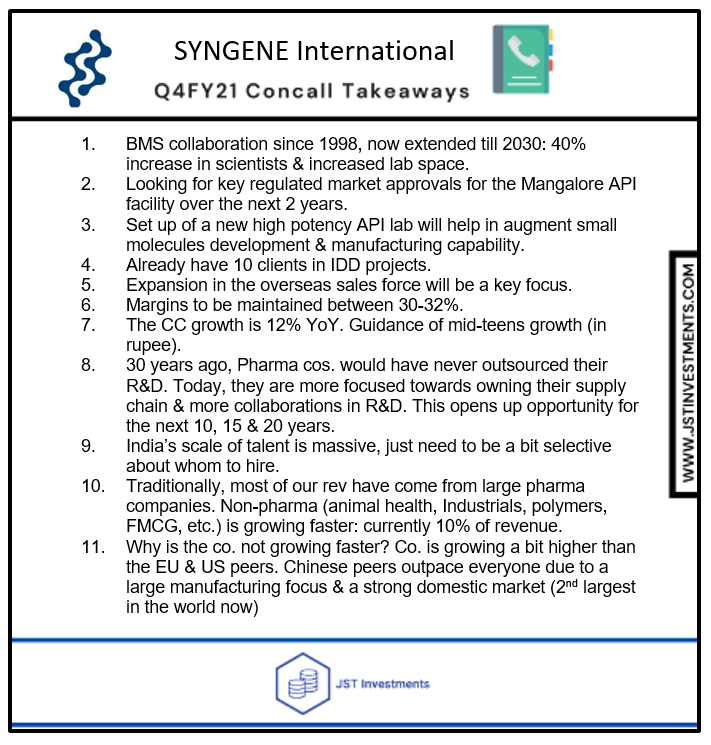

EXTENDS LONG TERM RESEARCH COLLABORATION WITH BRISTOL MYERS SQUIBB UNTIL 2030

This seems to be quite a significant announcement. The extension atleast till 2030 envisages another 200 more scientists and addition of a 50,000 sq.ft. dedicated lab space as well as new areas of research beyond what they are doing currently. Good work.

Per media release next year guidance puts revenue around 2500 cr+ and PAT at 420cr+, Capex close to 900 Cr. Current mkt cap of 21K cr is close to 10X sales.

Syngene has multiple growth levers, super long runway and one of the strong global CRAMS player with solid credentials. Valuations are likely to stay elevated and investment/ Capex heaviness phase continues.

Invested and added in recent pullback.

Thank you for the nice PDF. One of the takeaways for me is that growth rate has declined in the last 5 years. Does that mean that the premium (if any) is not worth paying anymore?

Disclaimer: Holding since 210 levels but unsure if the upside is limited from current levels (~600)

Study the future growth triggers of the company. Here are a few:

- Mangalore plant was just approved as GMP, once manufacturing starts this gross block will start yielding results

- If you are following recent developments, BMS extended their partnership with Syngene to 2030 while also increasing the scope. So they are billing existing clients more while increasing the future revenue visibility by almost a decade

- Study Syngene’s core development pipeline, if any of the molecules they are currently researching on pays off (and there is a high likelihood that it will since they work with 8 out of top 10 pharma names in the world), there will be a sudden hockey stick like growth

- They just finished building the biologics plant, another area of revenue growth for the company

Syngene is not for the impatient investor, will take years to grow with periods of hockey stick like growth.

Forget the price and study the business, you will see runway for the business to grow.

Disclosure: Holding, adding at every dip/business development

Sadly most Indian financial analysts focus either ask about margin, revenue and profit. Rarely anyone focuses on exploring if the quality of business is improving.

In any business, if the quality improves, underlying fundamentals will automatically improve if the management is competent. Improving margin and revenue is a knock on effect of improving quality in the business.

Revenue wouldn’t start as soon as trails are completed, it takes time to explore a drug and launch a product. Most of the really high revenue growth for Syngene will come from manufacturing (CDMO) rather than CRO part of their business. That’s why Mangalore API plant and their investments into Biologics manufacturing is really important.

In the recent conf call someone asked if Syngene can be a $1 Billion revenue business 5 years out and as a CEO he can’t directly comment on it but did manage to give an answer that’s it’s very much possible for Syngene to reach that level of growth. For context, Syngene’s current revenue is about $300 Million, so we are talking about a 3x revenue growth.

Thesis isn’t wrong, just may not happen immediately. This is a growth stock with more than 10 years of runway growth and clear visibility.

I will even go out on a limb here and say that Syngene has everything going for it and a very high probability that it will become part of Nifty 50, in 2030 or beyond.

A few thoughts about Syngene from what I could understand from the numbers:

-

In the last six years, revenue from operations has grown at about 17 % CAGR. There was been no down year since listing – one of the signs of a moat business model. Profit growth however has been a slower, in the 13-14% CAGR range.

-

Business is a high margin business, with operating margins consistently in the 30% range since listing (another moat indicator). PAT margins however have been declining lately from a consistent 20%+ range in the first three years of listing to 16.45% in FY21.

-

Operating cash flows have been very strong, growing at 18% CAGR. In recent years, working capital has generated positive cash flows, which is a very good sign. Operating cash flows in the last three years have been almost double of PAT. To that extent therefore, I would say EPS is understated and so P/E is overstated.

-

Business is capex heavy. Annual capex has grown from Rs. 300 crore per year range to more than Rs.600 crore per year in recent years. Capex for FY21 was lower at Rs.440 crore due to Covid, but company has guided for Rs.750-900 crore for FY22. As the business grows, you need to invest more and more to maintain the same level of growth.

-

Both interest costs and depreciation have been rising, which explains the decline in margins at the PAT level. Also point to note is that employee costs have tripled in 6 years, rising at 22% CAGR against 17% CAGR in revenue. Scientists don’t come cheap (programmers are dime a dozen)! No wonder company has guided revenue growth in mid-teens but profit growth in single digits for FY22 as well.

-

The capex-heavy nature of business also means that despite strong CFO, Free Cash Flows are weak. And so, dividends have been low or zero. Company also uses a moderate amount of debt (which is fine). Large debt repayment was done in FY20, but fresh debt was raised in FY21.

-

In FY21, company added 42 new clients – quite impressive I must say. Almost one new customer every 9 days! Now we need to see how fast they scale up and add to the revenues.

To conclude, I like the business model. But profit growth will not be easy in the long run as the capex will take its own time to reach full scale. How well they do that only time will tell. Current valuation is quite rich and not much can be expected immediately.

(Disc: Invested)