I am not sure whether I am senior on board to comment. However, in my personal view, two things would be critical. One buyback price and second whether the promoter are particiapting in buyback. In case promoter are participating then it would be more kind of dividend distribution. If promoter are not paticipating, then it might be interesting development as promoter find stock of the company moderately value to put surplus liquidity deployed in same.

We shall get better insight one more details are out post November 28 meet.

Discl: Among my top 5 holding and my views may be biased. I sold marginal quantity during last 3 months.

Sir, I am not aware and just asking, it would also be valuable to know if the promoters have issued any shares to themselves as Preferential / ESOP’s in some time prior.

This is all above board and exactly as you described, as long as it is not a way to bring back to normal any dilution done previously.

Although knowing you a little bit through the forum, if this was a diluting via employee options and then doing buyback type of company, you would not be invested here

Tender route buyback at price of Rs 2400 for 2.37% Share amounting to Rs 70 Cr. Not likely to have any major impact on price in my opinion in short term. In Long term does give indication that management find business prospect good and like to purchase share at Rs 2400 per share.

Promoter are also likely to participate so may also be consider as dividend payment then real buyback.

We would like to inform that the Promoters of the Company have communicated their intention to participate in the proposed buyback in the following manner:

a. Mahindra & Mahindra Limited has indicated that they would be tendering a maximum of 97,915 equity shares or such lower number depending on the response received from the public shareholders

b. Kirloskar Industries Limited has indicated that they would be tendering a maximum of 51,254 equity shares or such lower number depending on the response received from the public shareholders BSE Announcement

This appears to be a more of tax saving dividend distribution method than a pure buy back. So how should we interpret the intention of the Promoters in this action? The promoters are not diluting their stake through this action, but at the same time are not willing to increase their stake as well if at all the market price is reasonable as the board views it. This appears a like NOTA selection on the voting machine.

This is normal and being done by many companies as a tax efficient method of dividend distribution. Note that even after promoter participation in the buyback, promoter stake usually increases since acceptance ratio for small investors (those holding less than Rs.2 lacs worth of shares have 15% reservation in the buyback offer) usually turns out to be higher than for promoter / institutions.

Dhiraj, are you still invested in Swaraj Engines. Please share your thoughts on how good is Swaraj for investment. I was going through their financial statements and was impressed by the consistency of NP margin, sales growth, RoE and dividend yield.

After the corrections in broader market as well as in Swaraj Engines , it is worth looking at !

Dividend Yield of 3+% at CMP , Outstanding Track Record and return ratios . Excellent growth without any equity dilution or debt.

They have sold around 92000 Engines in 2018. Current Engine capacities is around 120000 which is near completion and they have planned for a capacity expansion to 135000 engines per annum as per AR18. There does not look any near threat from Electric engines as the HP required for tractors may be far away to be achieved by battery as told by management and shared by one boarder above !

Government’s thrust on agricultural and rural segments and doubling of Farmer income, the tractor industry is expected to maintain its growth trajectory for coming years.

Domestic tractor industry has grown at 22% in last year. Factors like successive normal monsoon, positive sentiments in rural areas, easy availability of farm finance and increasing demand of tractors for non-agri segment etc. may propel the growth in tractor Industry in coming years.

@dd1474 Sir , You have been long associated with the company and have attended the AGM too sometime back. Looking for some answers:

Company’s principal business is to supply diesel engines for tractors being manufactured by M&M- Swaraj Division only. Is it possible for the company to sell Engines to any other tractor manufacturer in domestic or International Markets ?

Do they have any plans or arrangement to diversify in other Engines segment apart from Tractors. Is there any other sector where their engines can be used. Have management shared any other plans in AGMS ?

Regards

Bharat

Disc: Looking to invest in coming days on further 5-10% Correction

You may call me only Dhiraj. On your queries, find enclosed my view point.

The company was origingally promoted to manufacture engine for Punjab Tractors (which sold tractors under Brand Swaraj, promoted by Punjab State Govt and Kirloskar Group). The Punjab State Government stake over period of time (after selling to PE fund) was acquired by Mahindra Group. So Mahindra today market tractors under Swaraj Brand. Punjab tractors are now merged into M&M and no longer seperate entity. So for Non swaraj brand, M&M still procure Engines from all other third party vendors. The share of Swaraj in M&M tractor sales ranges from 30-40% over last 5 years. It would be natural for M&M group to source increased tractors from the Swaraj. In addition to engine sales, Swaraj also supply some engine component to SML Group. However, share of Component sales is less than 5% of total value. While there is no constraint on Swaraj to supply engine to third party, currently, they are not even able to meet full requirement of M&M group and hence I see limited scope for exports and third party supply. The purchase price with M&M provide for a formula where by cost change in raw material is passed on to M&M with price being set every quarter (if my memory is correct). Further, Kirloskar group presence on Board would also check that transfer prices from Swaraj to M&M is proper and market linked.

The management would be focus only on engine business in Swaraj, M&M group would not like to bring other component supply for two reasons in my opinion. First, Swaraj Skill set and infrastructure is very specific to Engine manufacturing. Secondly, M&M does not have clear control on Swaraj Enginre as Kirloskar also have material stake on the company. Why would M&M bring all business to the company which it does not control fully? So, while presence of Kirloskar ensure proper check on related party, it would also being hurdle for Swaraj being used as first prefrence supplier for M&M Group in my opinion. These is my viewpoint and facts may be diffrent from same.

Discl: Among my top 6 holdings and hence view may be biased. Investors shall do their own due diligence before making any investment in the company.

The result are bit disappointing to me on volume front. I was expecting higher volume growth due to higher M&M tractor sales data. It may mean that volume of Swaraj brand tractor in M&M tractor sales has grown at lower rate then other brands.

As a result, financial also shown almost no growth. On positive side, there is no degrowth as well. Intersting to see how M&M sales progress in Fy20 and how is monsoon in Fy20 for Swaraj future performance. The valuation are discounting the figures but may see marginal negative impact of financials in next week.

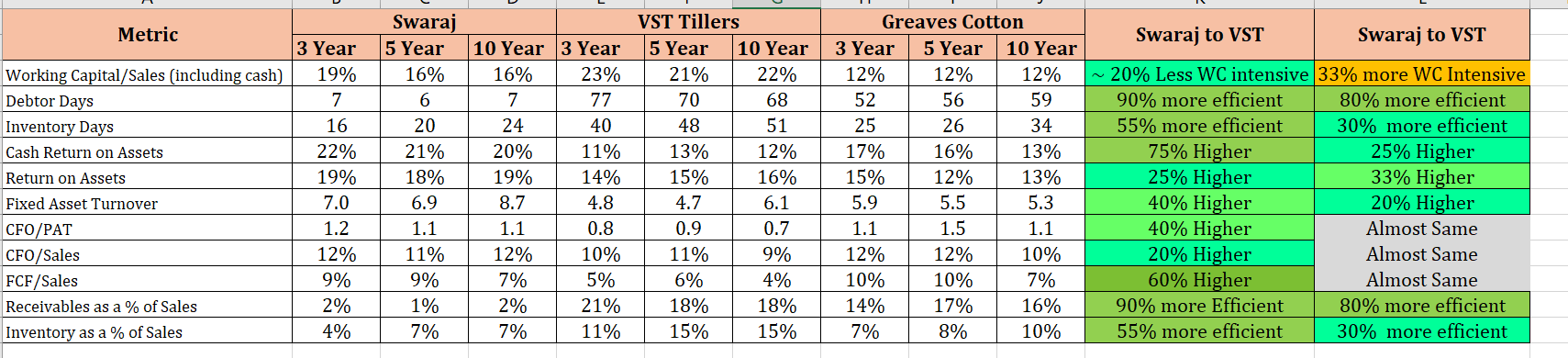

Took a small position recently in Swaraj. One of questions asked by a colleague was around why Swaraj and not VST. Below table may answer to some extent.

One key thing to note is Greaves cotton seem to be doing something good on operational efficiency front. Have not considered any relative valuation comparison in above exercise. I think there is enough qualitative information available on respective threads to address “why” side of these numbers

Hi ,

I think it is not a fair comparison in my limited knowledge as Business of all the three entities are different.

Swaraj Engine manufactures Tractor Engines required by Mahindra Tractor division as of now. They need very low SKU and thus looks very good on Asset Turnover and inventory management. Also their customer which is Mahindra is fixed and thus they have no issues with the Debtor Days and receivables. It is majorly a B2B Business.

VST is more into a diversified business of Tillers , Tractors (currently below 27 HP) , Rice Planters , Engines & Spares. Overall the percent of Engines/Spares is not that high.

It is very obvious that they need large inventories and High SKU and will have to give some credit time to the dealers and thus have high receivables/debtor days & high level of inventory days. It thus results into higher working Capital. It is more of a B2C Business. The growth in last few quarters has been poor. Management quoted delay in releasing subsidies by government as the reasons for poor growth.

Greaves Cotton is also a very diversified business. They are into 3W and Commercial 4W Diesel / CNG engines as well as into Non Automotive engines used in Marine , Construction , Agriculture. They manufactures variety of Industrial Engines ranging from 30 HP to 700 HP as well as smaller engines below 12HP. They also manufactures wide range of generator sets in the range of 2.5 kVA to 500 kVA. They also manufactures power tillers and light agricultural equipment like Weeder. They also have build a network of "Greaves Care” which is a one-stop Center for all services and spares requirements. They recently acquired Ampere which is making Electric Scooters. Given , the kind of business they have which require very high SKU , the working Capital Management is commendable. Despite all these verticals , the growth has been very poor from last few years but seems to be picking up from last few quarters. Management is too buying aggressively from open Markets in last few Months.

Disc: I am accumulating Swaraj Engines and Greaves Cotton in staggered manner. Tracking VST Tillers too which is facing some headwinds due to delay in release of subsidies by the government as per management. I like to play a basket approach here with some names in Auto space keeping a cap of 20% on sector with a cap of 6-7 Stocks.

Thanks a lot @bharat19 This is very helpful. Frankly, I did not ve much idea of greaves cotton when I did this. A friend asked on relative comparison of Swaraj and VST and then nother friend asked to add Greaves. But what was interesting to see that Greaves has improved on some of these metrics over last 2-3 years and available at good dividend yield and going thorugh company details gives good perspective of risk reward scenario. Thanks for the post

@suru27

The growth has started to pick up in Greaves in last few quarters and future looks good with the kind of developments going on. The growth need to be consistent otherwise it may turn into a trap. It can be termed as the Case of “Heads i win , Tails i do not loose much”. I believe that businesses like this need to be bought over a period of few quarters looking at the performance. The big negative is that Bajaj is not their customer which is a leading player in 3 W space.

One more business of this league I have started buying recently is Banco Products which has started showing growth in last 2 Years and is available at good valuations. Here also , when i first bought it , the dividend yield was very attractive and i thought that it may provide support on downside but still it corrected 10-12% from my initial buy price. It was a good learning that Market likes to see the growth every quarter and buying such business over a period of few quarters is more helpful.

Ya, more or less, similar views on Greaves. I think we would need clarity on topline loss which would happen on Diesel size and how much could be compensated by hrbrid, cng, ev,hybrid, b2c business etc etc. Not sure if possible to get a crystal clear view and we may need to flow through execution n keep accumulating if story keeps on delivering. Have few such positions where either there are some open risks beyond analysis and its more of an execution journey and hence hesitant to take big position. This looks one of them. Disc: 1.5% allocation at 122, still studying