Q2 has always been the best for swaraj. with the extra capacity kicking in and monsoon good i am hoping for a good Q2.

disc invested.

Q2 has always been the best for swaraj. with the extra capacity kicking in and monsoon good i am hoping for a good Q2.

disc invested.

Q2 results are out. Though the sales of the engine has decreased compared to the last year’s same quarter, profitability has increased a little bit. Shows the prudence of the management in controlling costSWARAJENG_press.pdf (699.7 KB). With two states declaring drought officially, short term concerns are there. But pretty confident that management would ride this through without any major problems.

Valuable inputs are invited

Disc- Invested

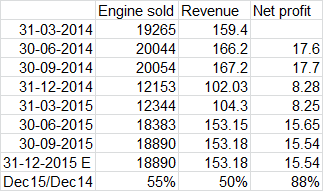

Being a seasonal business and dependent on Monsoon, FHFY15 was the best performance in my knowledge in history of the company. SHFY15 were profit and sales declined significantly. In fact in Q1FY16 and Q2FY16 the company shown decline in YOY sales, same is almost up 50% over SHFY15.

What would be interesting to observe that in case company even repeat same number in Q3FY16, of what shown Q2FY16, we would find 50% growth in Sales and 88% growth in Net profit !!!

Personally, I like the business and management of the company and among top 5 investment holding in my portfolio. My view may be biased due to my holding.

Hi @kunal_pawaskar, @siddharthshukla n all others,

Sid, I have been a follower of your blog since long. Any reason you have stopped blogging?

Kunal, I went through your analysis about the company on your blog, you have done a good research on the same. Regards to pricing power of the company, I have a different view from what you have.

As one can see, number of units sold has increased at a decent pace of 15.5% over 10 years, PBDIT per unit has shown a dismal growth. This is evident from the slowly falling PBDIT margins over the 10 year long period. I do not think the company has strong pricing power or may be it did have in the past, which is decreasing over the years. Hence, growth has come from increasing the units sold only.

Yes, there is a good chance that the company may increase the unit sold in the future as well however, we need to see whether margins are further going down or remain stable. There are other pros like, good cash flows, dividend payout. If we can get estimated revenue figures for the next two quarters (from a reliable source or management), then predictability would become a little easy. But, this will be medium term play and surely not a long term, IMHO.

Please correct me if I have gone wrong anywhere. Have made calculations in a bit hurry.

Views invited.

Guys, any old fellow boarders/investors, who have been tracking or Holding SEL for past few years, would like to share their Opinion, apart from conveying or calling it as a Cash Generating Machine or great Compounder.

Sanjoy Bhattacharya & Billionaire Infosys Founder Narayana Murthy’s Presence & Praise of company as a Shareholder & recent Performance & MCap now crossing Rs 1500 Cr, with Dividend Yield of 2.7%, though Valuations are a bit stretched, but still it makes a case of Core Holding for coming few years.

Views Invited.

Regards,

Bharat

How different is the business model with Escorts, Escorts have been soaring, but swaraj has hardly moved in last 4-5 months?

I like the company. Its got many things going for it - management, sound financials etc. But overdependency on M&M keeps me off. Also, its highly overvalued.

Anyone holding Escorts? If so can anyone share ideas on how and when to exit Escorts.

Since I don’t see any update on Escorts thread so pinging here Escorts Limited - Playing for Margin Expansion

Disc: I have big holding in escorts, small holding in Swaraj engines

I don’t have any exposure as I missed on Escorts but IMHO it has done very well recently because Mgmt has sold off loss making auto ancillary unit and has publicly expressed their intention to focus on their core business which if executed well can really turn around otherwise lagging business on back of expected agricultural revival due to OK monsoon. Provided that you have good entry price and depending on your opportunity set, IMHO It won’t be a bad idea to hold on to it till the story plays out completely.

To be honest I entered Escorts only on the ancicipation of a good monsoon without knowing about any news of auto ancillary, but if you have any numbers around how much EPS it can impact please do share on the read thread.

Excellent M&M Tractor Sale Number. Swaraj Engine May have wonderful September quarter if the sourcing remain at same level as in past. Around 70% growth in Month on Month Tractor Sales for M&M for Sep 2016

Escorts can be tactical holding in Bull market. But management is cheat. A majority of people who invested in Escorsts Finance FD were never paid back. I have personal experience

Looks like even they cheated their own employees

http://www.consumercourt.in/fixed-deposit/9587-non-refund-fd-amount-escort-finance.html

As they say, lots of sins are washed away in bull market.

Swaraj posts another set of excellent numbers. Happy to see that demonetization did not effect the company’s performance as expected widely. Also, company planning to increase the capacity to 1.2 lakh engines per year anticipating the demand.

Disclosure: 6% of portfolio

I think some bit of weakness owing to demonetization still exisits in the stock, moreover there have been reports that the RTOs are not registering tractors owing to the BS-IV ban.

Stationery engines as is present in tractors are classified separately and do not come under the purview of the BS-IV emission norms.

Stellar performance by swaraj engines for q4 and overall fy17.

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/4e0ddac5-5bc2-420e-9f81-379861833493.pdf

Declares Rs .43 dividend as well.

Disclosure: invested.

I like Swaraj engine and holding for last 5 year with addition during May/June 2014. Very good business model with management and real cash generating compounder. I never expect Swaraj to grow by 50-75% during one year. However, very comforable with the kind of dividend and growth it has shown.

During FY12, it declared Rs 13 Dividend (With March 2012 share price Rs 407, giving almost ~3% dividend yield).

FY 13, dividend declared Rs 33 (March 2013 share price Rs 395, giving dividend yield of ~8%)

FY14, dividend declared Rs 35 (March 2014 share price Rs 691 giving dividend yield of ~5%)

FY15 dividend declared Rs 33 (March 2015 share price Rs 802 giving dividend yield of ~4%)

FY16 dividend declared Rs 33 (March 2016 share price Rs 857 giving dividend yield of ~3.5%)

FY17 dividend declared Rs 43 (March 2017 share price Rs 1484 giving dividend yield of ~3%)

On share bought on March 2012, Rs 407, total dividedn received by investor is Rs 190, so almost 50% of value received back as dividend ! Further, on acquisition price, the company is paying almost 10% dividend yield, which is much better than current interest on fixed income.

Risk:

Positive:

As per my understanding, the company has increased capacity from 42,000 in March 31 2012 to 120,000 in March 2017.

So almost 3 times increase in capacity with no increase in debt and constant increse in dividend. What more we can expect form the company? While at a particular stage, the company would not be able to increase capacity by brown filed, and may need to undertake greenfield project. I expect Greefield capex cost would be signficantly high as compared with current capex cost. However, with 82,297 engine sales and 120,000 installed capacity, I feel even no further scope for capacity expansion in current plant, I still feel it would be able to work with current capacity at least for 12-18 months.

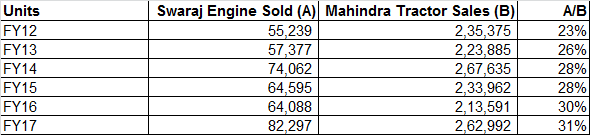

Increasing share in Mahindra Tractor procurement

Find enclosed incresing share of Swaraj engine in Mahindra Tractor sales over the period

Efficient operating performance

Despite increase sales (no data about of production of engine avaiable now, so assumed production equal to sale), average production of engine increase signficantly

This is just one parameter I could collect from annual report over the period. However, give very good unstanding about efficient resource utilisation.

BSE link for dividend declared:

Discl: Swaraj is among Top 5 holding of mine and my view may be biased. Investor are requested to do their own due diligence before investing.

I attended Swaraj Engine AGM on July 24 2017. Find enclosed my notes on AGM and other dicussion. Please note that Swaraj is among my Top 5 holdings and my views may be biased due to my holding. Also, there may some communication error from my side and reader should do his/her own due diligence before taking any decision.

Chairman Mr Makand appreciated contribution of Mr NR Thakker who died in 2017 as age of 84 years, for being pioneer and main person to set up plant with Cost of Rs 4 Crore and completed installation of new plant within 12 months time. He was associated with Kirloskar group who has been associated with the company since inception as a promoter when Punjab Government intended to set up Swaraj Engine in mid 80s. Subsequently Punjab State divested its stake to M&M group while Kirloskar group continue to maintain its original holding.

The company’s fortune are directly linked to Tractor industry, which in turn, is depedent on Monsoon and agricultural income. After 5 years of decline, during FY17, tractor demand regusteres 18% growth in domestic market to 582,084 units. Swaraj delivered its best ever life performance on all paramters (i.e. Highest engine sale of 82297 units, Net operating revenue of Rs 666 Cr, PBT of Rs 105.5 Cr and PAT of Rs 68.8 Cr).

For first time, the company reported PBT crossed Rs 100 Cr. The company increased dividend declared at Rs 43 per share (including Rs 25 per share special dividend) for FY17 as against Rs 33 per share declared for FY16. The share price also increased significantly resulting in market capitilisation of the company crossing Rs 2,500 Cr.

The company has continue to work along with society and employee well being and constantly assist neighbour villlages by providing skill training to provoding primary healthcare through mobile healthcare van.

During FY17, Swaraj received TPM excellence awared by Japanese Institute (not sure about the name) and also quality circle team won Gold award in Banglore.

In Q1FY18, the company report all time high sales of 23,287 engine (20,910 in Q1FY17); Sales of Rs 194 Cr, PBT of Rs 32.2 Cr and PAT of Rs 21.5.

Based on good monsoon anticipation and performance and also based on interaction with the clients, the company anticipate demand to continue to remain strong. In order to capture growth in the demand, the company has announced to enhance capacity by 15,000 units to 120,000 units which is expected to operational from next financial year.

Swaraj transition to GST was very smooth with no loss of production. Further, commercially also GST rate is broadly in line with previous tax regime and hence there is no major impact expected either on Swaraj or on its end use industry i.e. Tractor in view of management.

The company would be spending Rs 35 Cr to increase capacity from by 15,000 units. (Average Capex of 23,333 per engine vis FY17 EBIT of Rs 12,829 per engine, giving incremental ROCE of more than 50%).

The management were asked about perceive threat from Electrical vehicle and likely threat of same to Swaraj engine. Management consider that current threat of EV is more proximate to Car/SUV business. The load required for tractor engine is very high which would not be possible to replace with current development in battery for tractors. Hence, management do not consider Electrical betteries replamcent to Enginre in foreseeable future.

The company has Rs 180 Cr worth of liquid balance (in MF and FD). The management were asked about usage of same. Management said they would like to invest in business which can match the ROCE return with Swaraj Engine is generating currently. Till the time they find such remunerative opportunity, they would continue to hold same on balance sheet and reward the shareholder by way of increased dividend (from income generated of cash surplus) rather then make wrong acquisition which would adversly affect future prospect of the company. Management appear to have clear focus on wealth creation as appeared from the reply.

There were also queries about potential to expand product range of Swaraj Engine. Management said currently there is no product which Swaraj can enter and replicate market leadership which is enjoy in the tractor engine. However, they are open in case appropriate opportunity arises.

The company has suffient space/infastructure to expand capacity at present location in Mohali for at least 5-7 years. Hence, with growing demand for tractor, the company would continue to do expansion at appropriate time with lower capex resulting and superior ROCE and cashflow in medium to long term.

The company has proper agreement with M&M (Swaraj Tractor division) which provide of pass on increase/decrease in material cost. During the recent year, the company new product launches are for higher HP tractor which generally get higher realisation then in 2-3 years back. Despite imrpoved product mix, average engine realisation continue to remain in range of 80-82K. Enclosed table provide detail information

Due to lower raw material cost, the commpany has passed on input cost benefit to M&M as per the agreement. Hence, while sales realisation has remain constant, operational EBIT increased from Rs 7,558 in FY15 to Rs 10,742 in FY17.

The management also indicated that the company is well prepared to manufacture engine which are in compliance with new emission norms as and when implemented.

This was my first AGM with Swaraj despite my holding the company for last 5 years due to location. However, I must acknowledge that my experience for this AGM was one of the best I have attended over last 3 years, definitely much better then all Mumbai AGMs.

Revenue up by 3.75

EBITDA up by 20%. EBITDA margin 16.8 (up by 2.36%)

Net Profit up by 22%

Good set of number by Swaraj engine in my view. However, press release is not providing any update on capacity expansion which would be critical as current quarterly production of around 24,000 is almost operating at full capacity of 100,000 engine per annum. One need to get more insight from the management about when the new expansion would commence operation in my opinion.

Discl: It is among by top 5 holding and my view may be positively biased due to my holding. The investor are advised to do their own due diligence.

Interesting move by swaraj engines.

"Swaraj Engines Ltd has informed BSE that a meeting of the Board of Directors of the Company will be held on November 28, 2017, inter alia, to consider the proposal to buyback the fully paid-up equity shares of the Company"

http://www.bseindia.com/xml-data/corpfiling/AttachLive/E07BDB73_6139_4E16_8496_F6DE12FF77BB_161746.pdf

Any comments by the senior members on this move by the company?

Disclose : invested. Watching the development closely.