Q2 FY2025 Conference call Highlights:

Opening Remarks:

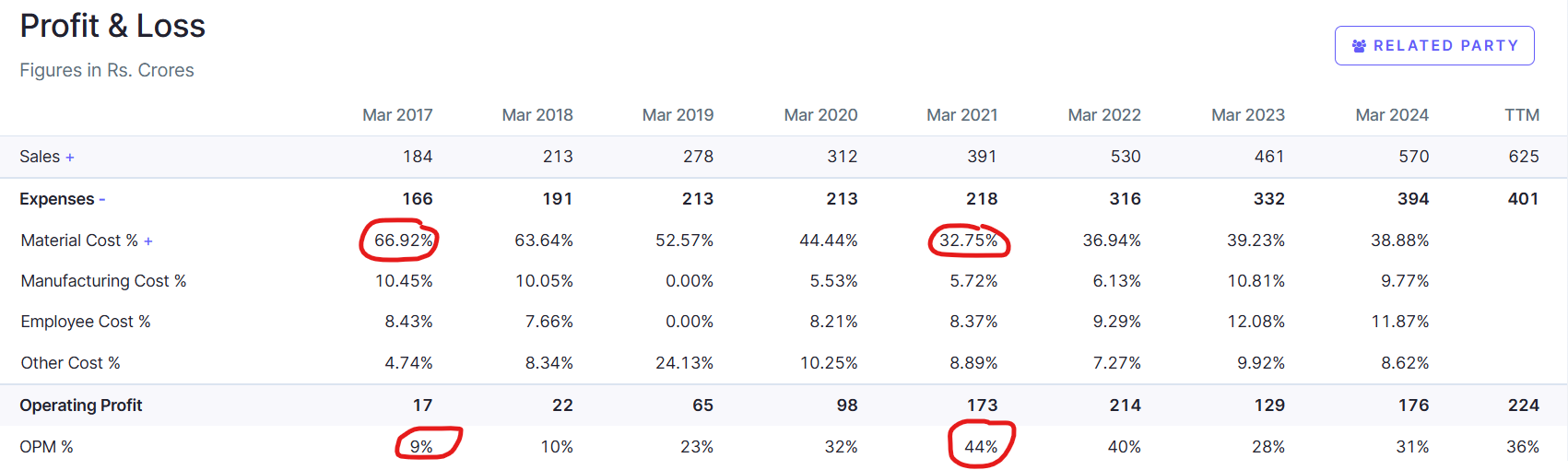

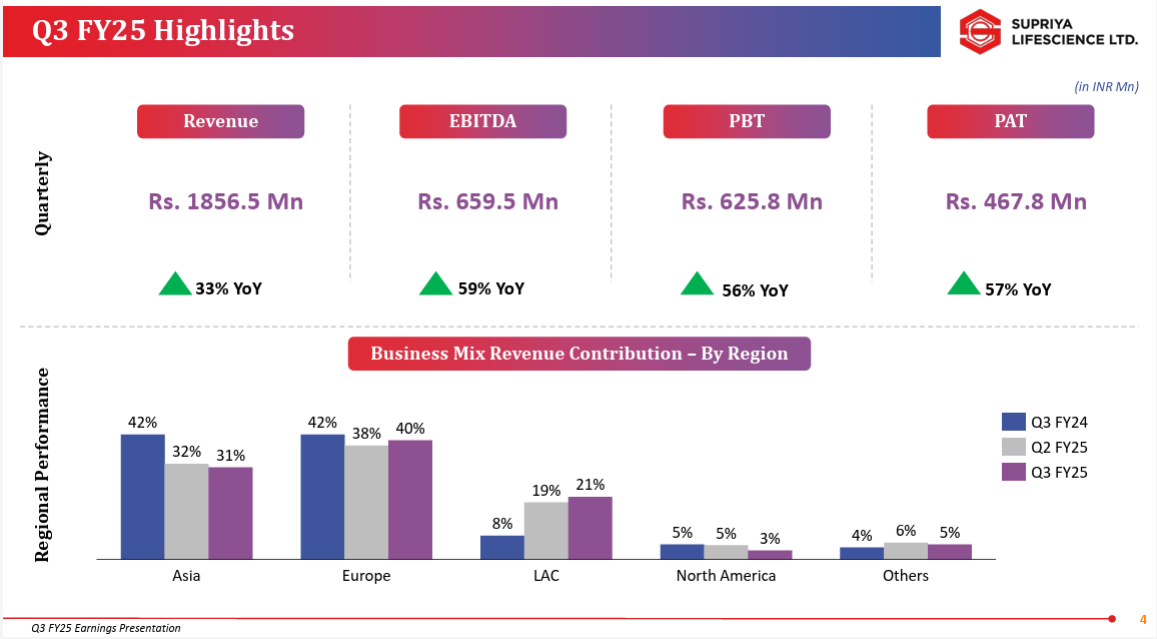

Revenue increase 19% YoY.

EBIDTA increase 104% YoY.

PAT increase 93% YoY.

CDO/CDMO Ambernath facility started from Q4 FY2024 for finished formulations. 70KL.

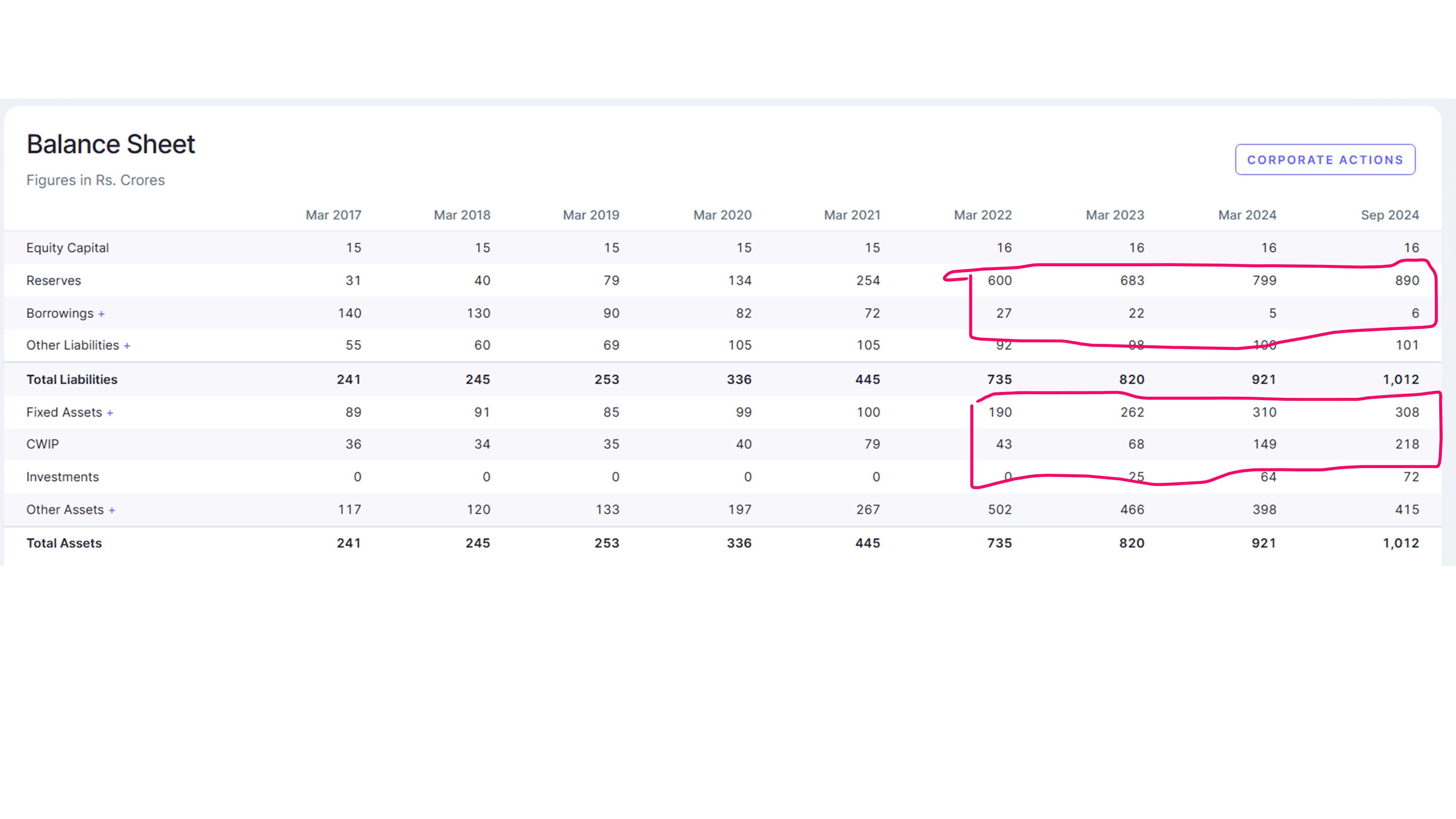

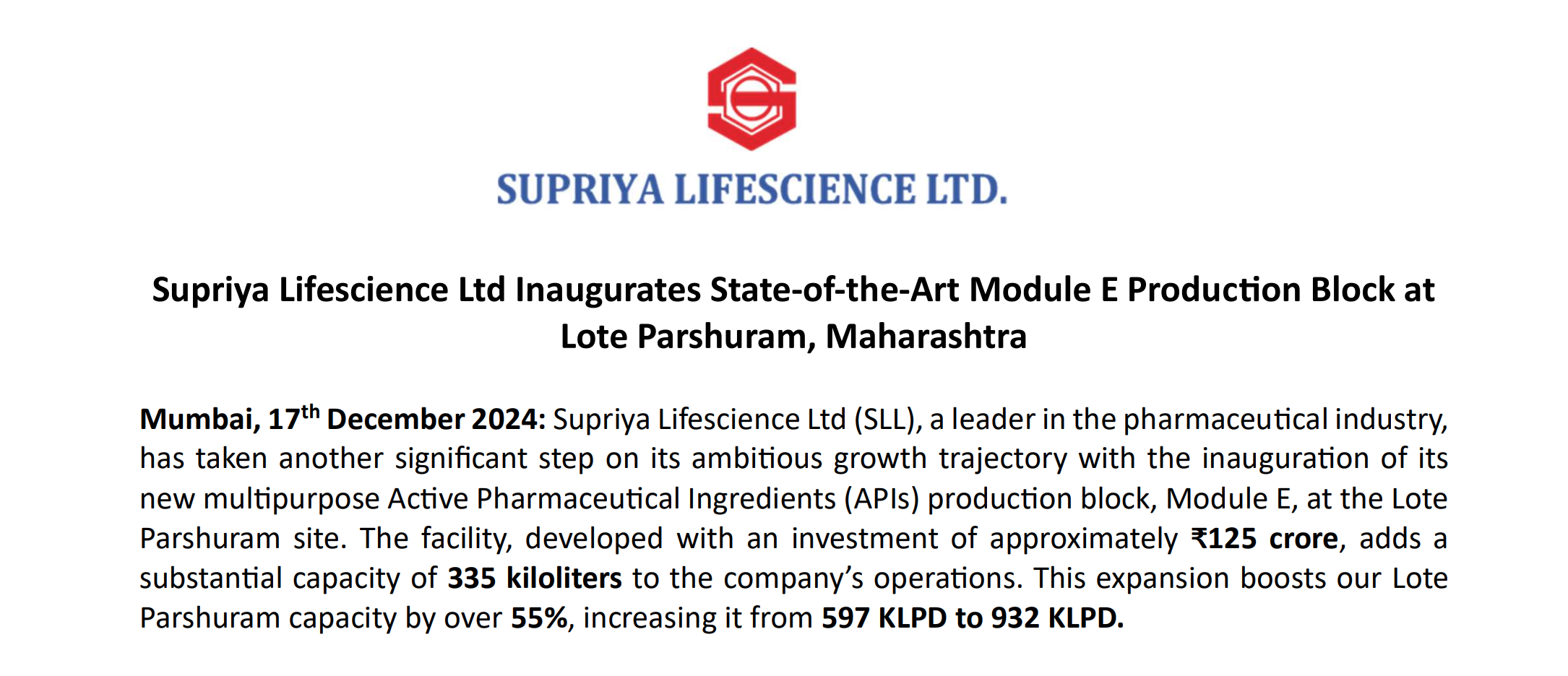

Manufacturing block (E block) at Lote Parshuram, which will increase total capacity from 597 KL (76% utilization, optimum) to 1,020 KL by Q3 FY25. It will take 1.5 to 2 years to take reach max. capacity.

Guidance:

Confident of 20% Revenue growth with high margin.

Revenue target of 1000cr. by FY2027 with high margin. Very conservative guidance.

CDO/CDMO to diversify revenue stream.

Margin guidance is 30 to 34% on yearly base due to new products.

Margin :

Backward integration helps in increase in margin. Many products manufactured up to 8 steps backward integrated.

Regulated markets have higher margin.

New products will be added in next quarter, which will have slight dip in margin due to first roll out in semi regulated margin and then to regulated market.

Cancer oral detection kit: filing patent for many countries, expected to start clinical trails. Revenue may come after 3 years.

CDO/CDMO opportunity:

Full effect will be in 2 years. In next 3 years, should contribute to 20% of revenue.

No capex, next wave will be in Patalgana after 2 to 3 years.

Once DSM project complete, bigger opportunity may come.

Margins will be similar. Formulation will have higher margin.

China:

Supriya do not produce any product which is produced in INDIA. They compete with China, as Chinese plants do not have GMP or any certification. Do not negotiate for price as Supriya is GMP, USFDA certified plant.

Others:

52% revenue from regulated market, remaining from semi regulated market and domestic market.

Diversify product portfolio and not dependent on any key raw material. Raw material Available cheaply and widely available.

H2 will be better then H1 on overall basis.

Latin American market is improving and will continue progress as registration continue.

H2 will be better then H1 on overall basis.

Latin American market is improving and will continue progress as registration continue.

D: Invested