Supriya Lifesciences( very bullish commentary ) -

Q1 FY 25 concall and results highlights -

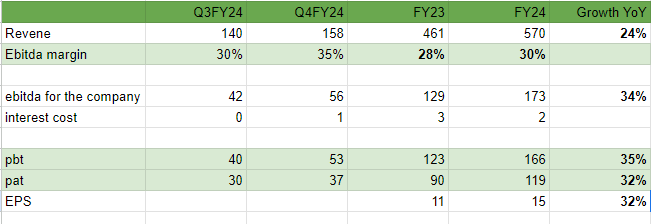

Revenues - 161 vs 132 cr, up 21 pc

Gross Margins @ 69 vs 64 pc ( massive expansion )

EBITDA - 63 vs 44 cr, up 41 pc ( margins @ 39 vs 34 cr )

PAT - 45 vs 29 cr, up 56 pc

Therapy wise business mix -

Analgesics / Anesthetics - 48 vs 46 pc

Anti - Histamines - 11 vs 19 pc

Vitamins - 11 vs 12 pc

Anti - Asthmatics - 7 vs 6 pc

Anti - Allergics - 5 vs 5 pc

Anti - Hypertensives - 4 vs 1 pc

Company has a niche product basket of 32 APIs. 15 products have a high degree of backward integration. They represent 70 pc of company’s revenues. Company is in the process of integrating 3 more products

Geography wise sales mix -

Asia - 33 vs 41 pc

Europe - 51 vs 34 pc

Latin America - 9 vs 10 pc

North America - 3 vs 9 pc

Others - 4 vs 6 pc

Top 10 customers account for 50 pc of sales

Exports constitute 80 pc of company’s sales

Company is the largest exporters of - Chlorpeniramine Maleate ( Anti - Histamine ), Ketamine Hydrochloride ( Anaesthetic ) and Salbutamol Sulphate ( Anti -Asthmatic ) from India

Currently, the top 3 products contribute to 45 odd pc of the revenues. In the next 3 yrs or so, company expects this to come down to 25 pc of revenues as other products ramp up. Expecting to add 3-4 new products / yr for the next few yrs

Surge in revenue contribution from regulated mkts ( EU ) has been margin accretive in Q1

Growth in future will be led by more molecule launches. Company initially launches their molecules in unregulated mkts and then introduces them to regulated mkts - over a period of time. Hence the business from new launches is likely to be margin dilutive - to begin with

The newer molecules that company intends to get into are going to be higher volume molecules ( vs their existing molecules ). Company will ensure high degree of backward integration to keep the competition at bay in these molecules

Company should be able to maintain EBITDA margins > 30 pc for full FY 25. Exactly how much above 30 pc can’t be said

With the new launches lined up in H2, share of business from North and Latin America should definitely move up

Revenues from the new CMO segment should start flowing in from Q3/Q4. Will see larger contributions from CMO business in FY 26

In the next 3-4 yrs, company expects CMO operations to contribute to 20 pc of their topline !!! ( this should mean rapid growth in CMO vertical )

Generally H2 is always better for the company vs H1. Likely to be the same for this FY too

Company new launches are in the areas like - anti-anxiety, anti-diabetics and aesthetics. These r likely to be large molecules ( in volume terms ) and are mostly part of China + 1 strategy of the customers. Full impact of these should be visible by next FY

Company has given a 20 pc topline growth guidance for this FY ( although they admitted that its on the conservative side )

**Company expects its Ambernath facility to commence commercial production - sometime in Q3. This facility will also cater to CMO of formulations. They r setting up large lines for bottling, tablets, capsules and Injectables at Ambernath. Total capital outlay for the Ambernath facility should be around 130 cr **

Company has been awarded a 10 yr CMO by a European player - DSM Fermenich. Supplies should start in H2. Have another 2-3 opportunities which are in final stages of discussion. Expecting positive outcomes on these before end of Q2

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation