The key products of SLL such as Cetirizine Dihydrochloride, Diphenhydramine Hydrochloride, Chlorpheniramine Maleate and Pheniramine Maleate are in the therapeutic segments of anti-histamine and anti- allergic, which are widely and commonly prescribed drugs for treatment of common cold, cough and flu. Ketamine Hydrochloride is in the therapeutic segment of pain management.

Did the company get any boost during covid because most of its products come under pain managment, anti allergic?

3 Likes

Going by the conference call highlights, I think one of the reasons for the fall in gross margins could be the way the company classifies the LATAM markets.

Supriya classifies LATAM markets as a regulated market, simply due to the fact that the registration process with the Brazilian Health Authority (ANVISA) is as stringent as USFDA/EDQM.

However, the management has itself alluded to the fact that although volumes are substantially large in the LATAM markets, pricing is not as good as other regulated markets, such as US/Europe, and is just slightly better than Asian markets.

Now, the share of regulated markets in Q3 FY25 stood at 45% versus 40% in Q3 FY24. This was primarily due to LATAM’s share in revenues increasing from 8% to 21% YoY. Notably, cost of material consumed has increased at a faster pace of 39% in Q3 FY25 on a YoY basis versus the revenue growth of 33% (although gross margins have increased on a YoY basis due to changes in inventory but moderated on a QoQ basis). All this is despite the fact that backward integrated products contributed 77% to Q3 FY25 revenues versus 73% in Q3 FY24 (74% in Q2 FY25).

Also, the management had already guided in Q1/Q2 FY25 that there would be slight moderation in EBITDA margins from the 39% levels seen in H1 FY25. It has also guided that Europe and LATAM would constitute a significant chunk of revenues over the next 2-3 years.

While there are many positives for the company and the management has delivered on its guidance, IMO, the gross margins/EBITDA margins need to be monitored in the context of increasing LATAM contribution to overall revenues.

Also, the fact that to what extent could CDMO/CMO opportunities cushion the impact of margin decline due to the increasing contribution of semi-regulated LATAM markets needs to be watched out.

Let me know if I am missing something.

4 Likes

I think Bluejet thread has an ICICI Securities report which details quite a bit on Contrast Media Global players and chemistry a bit.

Also, Bluejet is dominant in this area for long based on my reading in last week and its quite possible to hire someone from that team into another company and crack this area is its niche and high margin. Somehow locations of Bluejet and Supriya plants seems similar at high level, so this is my guess

I think right way will be to probe management which Global client they are working/ which chemistry and which stage they are in currently? Most of this can come from ICICI Securities detailed report which i mentioned above

For a company like Divis with so much scale, this might have been insignificant for them to consider them earlier as a Strategy

Somehow ECI report didn’t show me anything like Bluejet thread on API and capaciities for Supriya on this

Invested since a year

2 Likes

Management has indicated 34-35% as sustainable margins, even with LATAM contribution increase

Company has many growth levers in place - recent capex, CDMO, contrast media, geographical expansion, whey protein. Plus, valuations are very reasonable and the company is able to grow without any equity dilution.

Disc: invested.

12 Likes

I havent done much of reading on API companies ,though this company has best of gross and ebidta margins, their business looks very capital intensive, yearly capital work in progress close to or higher than yearly profits, high inventories, high receivables… working capital stretched , is this common among API players? per previous year data of the company

,their asset turns is around 0.5 to 0.6, so if they have to achieve the target topline of Rs1000 cr by another year or 2, do they need nearly double the capital (assets) to get there from now? or the new capacities that have commercialized this year will be sufficient?

3 Likes

On the working capital during covid and after years generally companies went on building inventory due reliability in supply chains, Now red sea crisis is playing the spoil sport. But as of now a WC cycle of 120-250 days is visible in api industry as observed from Divis, Neuland and Laurus labs, Alivus. Particularly for large scale api players for scale advantage they make it and store. But this model is changing with innovations like flow chemistry. On the asset turnover a 2-3 times is considered good as your regulated market exposure builds you will have high asset turnover even though volume remains same due to higher realisations. With the current gross block they have commissioned in January they can double their production if I remember from one of their old concalls they can go till 1200 cr with the current capacity Lote. Ambernath formulation facility guidance is unkown as of now. Capacity is not constraint as of now ability to sell more products different apis is the challenge. Whey protein, DSM firmenich, atorvstatin, desflurane etc these are the products they have launched recently. Contrast media as of now it is in validation phase, Q2 FY 26 they will guide.

5 Likes

I forgot to add this they dont disclose their future pipeline so there can be surprises on antidiabetic(semaglutide), anti hypertensive.

2 Likes

this is helpful @buffet , thanks. Since it has listed just a couple years back, have you seen if they can pass the raw material and logistics cost increase easily to customers?

Their AR generally provides some color on their plans and vision and also flexibility of their geographical dependency, but the image that I got so far is , they need continuous large capital infusion to continue growing, it didnt feel like some incremental capital leads to reasonable growth. Liked the background of promoters…

generic api business is very competetively priced in other words no pricing power, the lowest reliable cost producer wins the business. In few cases when there are shortages you tend to get short term booms like covid or the current tarriff regime. The edge supriya has is, it has 15 backward integrated products so they have a good control on pricing and also saves on logistic cost. They are already very large in 3 apis ketamine chemistry and anti histamines. No they dont need a lot of capital to grow they doubled their volumetric capacity from the time of ipo and bought real estate for future acquisition. The business does 20% ROE as no debt and cash you can take that as ROCE as of now I mean for FY 25. As utilisation changes over 1-2 years it improves as they are done with their capex. All they need now is working capital which should be easy. So I dont know why you get an image of capital intensive business.

11 Likes

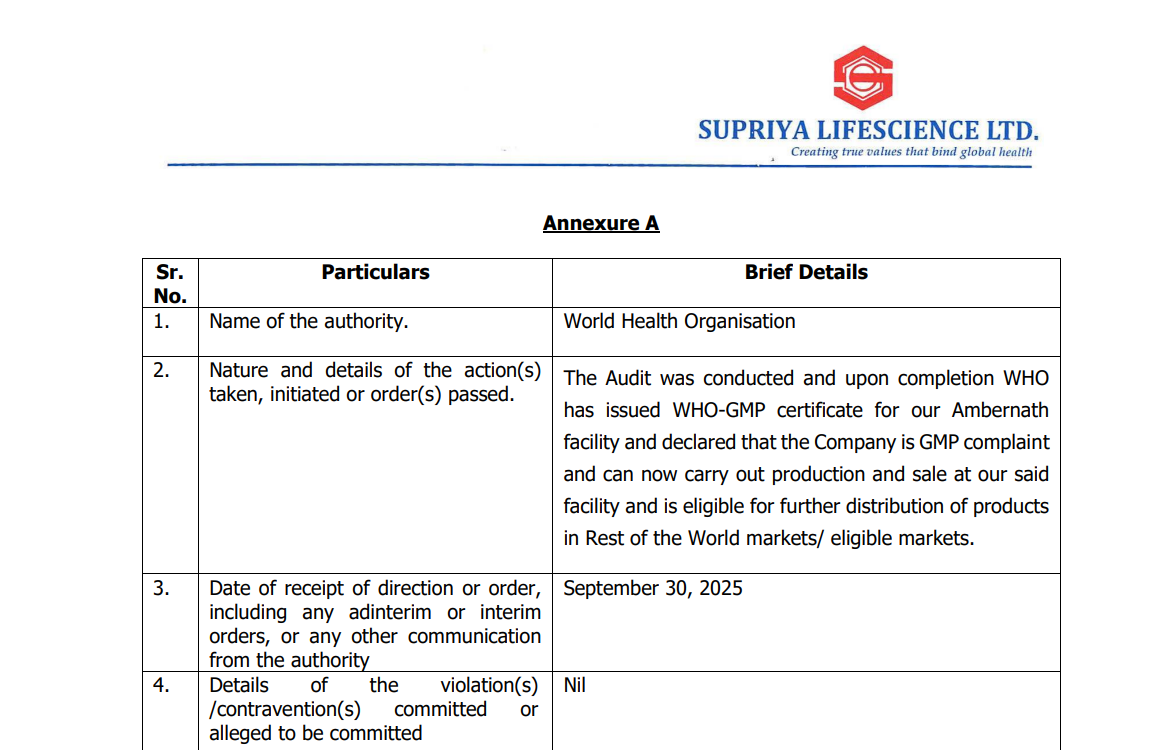

- CDMO is expected to contribute 20% to the business, an EU audit is anticipated in the second quarter of next year, and Latin American and European markets will remain major revenue drivers.

6 Likes

Might get the benefit of less reliance on US market (5%)? Could this be the dark horse of Pharma sector?

6 Likes

supriya lifescience concall update- FY26 guidance is 20% rev growth which in my opinion is high bar as there is only 1 single new product launched in Q4 and existing products will increase their mkt share. Evidence in their balance sheet does support the high inventory they are carrying along with receivables they haven’t billed but shipped. Along with this there is a cdmo contract from DSM firmenich for vitamins close to 30-35cr for this fiscal year. On a revenue base of 700cr they have to do incrementally 140cr to meet guidance(20%). 110cr has to come from their generic API business which i think is a high bar without new products. Margin guidance is 33-35% so eps growth will be 10-15%. It is trading at 31 times ttm pe which i believe is pricing in 20% growth.

Fy27 story is strong as formulations facility will clear regulatory audits like EUGMP, ANVISA, USFDA(not sure on the timeline), cdmo contract will increase to 70cr, contrast media apis 2 products will be launched in Q2fy26 but for regulatory permits to Europe, Latin America, USA it will take 3-4 quarters. Ambernath facility also will scale as there are no other suppliers outside China for their product choice(Desflurane) personally checked it they are correct. Module E is already commissioned which will scale as more products are launched like atorvstatin from n-8 ksm. Another ADHD product I am not sure what this product is due to competitive reasons they haven’t revealed will be launched in FY26 but scale up will happen in FY27. Lisdexamphetamine Dimesylate is the adhd product sourced from their website this is my guess.

Right tail events are any new cdmo api contracts or advanced intermediates this is very likely(as evident from other companies press releases) but after signing contract it will again take like 15-24 months for validation, regulatory permit.

16 Likes

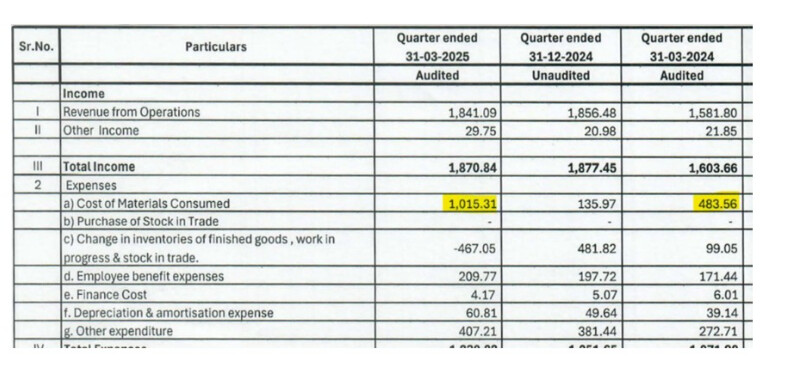

Guidance is excellent and results are well received. I just do not understand spike in cost of raw materials for a backward integrated company. No insight provided in con call. Company seems fairly priced as 5 year profit growth has been in line with 20%

1 Like

raw material costs is net of changes in inventory so latest qtr cost is Rs 54.8 Crs vs Rs 61.78 Crs in previous qtr and Rs 58.26 Crs in same qtr last year

3 Likes

I suppose per IND AS there is a separate line for Inventory there, so it cannot be net of inventory ? Negative value for “Change in Inventories” means that inventory has increased. Perhaps what you mean is the increase in COMC is due to the inventory built up

EBIDTA margin moderation not attributed to pricing pressure and products diversification will materialize in Fy 27.

The four new products which we are launching, first we have already launched in Quarter 4,but that particular product, the global market size is about $300 million. And the three new products what we are launching in the next financial year, one of them which is coming in the ADHD category is about 90 million, contrast media is about 500 million. And then we have some cardiovascular drugs which is about $100 million. So, if I put together all this, we are closer to $1 billion in terms of API market size. We are targeting these molecules because globally today for these particular molecules the supply dependence is there only on one manufacturer predominantly for most of these it is from China and as you know the global trend people are looking for China plus one manufacturer. I think we can benefit a lot in these molecules.

We have been working on them for the past 2-3 years. We have really focused on

end-to-end backward integration.So, what is happening in FY’26 is that the newer products are also getting launched and typically whenever we launch a new product, the initial scale up of these products happens in the semi regulated market where the average selling price for the product is not high as regulated markets. So, we are anticipating some compression in percentage margin. We are very confident that in

terms of the absolute EBITDA value or the PAT value, you will see good growth.

Whey protein, which was the starting point for us going into the market with the product. After that, we are in discussion with one of the largest distributors in the country, who is basically a large stockiest for whey protein. So, we are in discussion with them. We are very close to signing our first contract with them. The volume this year would not be very high. We are expecting somewhere to the tune of 100 metric tons because this is a completely new product for the Indian market.But if the market acceptability of theproduct is good, it can really scale up in the next 2 to 3 years and we are targeting at least in the next three years, it should touch about 1,000 or 1,500 metric ton.

3 Likes

the changes in inventory is basically the semi finished goods in various stages. When required the processing is done and it can be converted to finished goods. This inventory is used to make the final goods so the raw material consumption is always calculated net of these 2 line items.

For this qtr material cost is shown as 29.78% which is 54.8/184.

The first line item is basic raw material which is not yet processed and procured in the quarter, processed in the quarter and converted to finished goods and sold, the 2nd item is the carry over or bought out goods which are in semi finished or partially processed state which will be converted to finished goods, these are not yet converted to finished goods or not yet sold as finished goods hence shown here.

2 Likes

4 Likes

I have been thinking quite on this . they had a major maintenance in plant d and the revenues will recover in Half year2 FY 26 . Plus they also mentioned that there will be maintenance in plantA and B . And also the capacity is already at 75% utilization . I guess the reveneues will flatten for some time . When is the ambernath facilty ready for utilzation

6 Likes