Results released today for Q3 FY 23, Underperformance in each and every aspect. Just waiting to see what the excuse they want to say. Last 2 quarters asking Investors to see the Q3 and Q4. Now Q3 also out. Company has to improve on excuses along with operational performance

4 Likes

In Concall they have informed that CEO has resigned because of personal reason, CFO-Krishna-strengthened our team, Going forward R&D higher management and Manufacturing related personnel -will be strengthened further and updates related to this will be informed going forward.

Based on Concall, One thing is clear - Margins which were impacted may not be able to pickup soon as management is not sure of China Business volumes, However other markets North America volume increased. Hence revenue remained flat mostly. They are working on de-risking of portfolio from over dependence on China to other regions and also want to reduce product portfolio concentration. Situation may slightly improve for next 2 quarters, doubling of revenue by FY 26 with 30% margins is expected in best case situation.

7 Likes

Seems like the management is maturing. This is a much more measured commentary compared to the aggressive guidance given in previous interviews. Looks like they have learnt from the fiascos that were Q2 and Q3.

Disclosure - Invested

9 Likes

Decent set of numbers in the quarterly results that came on 3rd Aug

Press release

Saloni’s interview in CNBC…key highlights

Recent adds by promoters

PS - invested

2 Likes

https://www.equitybulls.com/category.php?id=335952

The primary purpose of this collaboration is to bring the optimized protein into the Indian market. ioProtein is a patented process (patent pending in the US) This revolutionary protein powder is designed for use as protein supplements and boasts a significant advantage, and it is highly bioavailable. This means that higher amounts of proteins are absorbed quickly by the body, providing consumers with a more effective and efficient protein supplement.

.

During the term of the agreement, Supriya Lifescience Ltd will lead the manufacturing and marketing of ioProtein in India. This marks the introduction of a new category of protein powders in the Indian market, and it is relatively healthier compared to other popular protein powders available through various Gyms, general stores, and digital marketing channels.

5 Likes

Even though June quarter has seasonal impact on results, however this June quarter, Supriya Lifesciences did really well. Looks like bottom in margin is behind now, able to maintain above 30 %.

1 Like

It seems now that both the year pre listing with 40%+ OPMs and the terrible Q2/Q3 numbers due to the China situation and de stocking were exceptions on extreme sides of the scale. Looking at Q3 results and the concall following that, this could be a consistent 30%+ OPM business comfortably growing at 20%+ currently quoting at a 1 year forward PE of 21-22.

Valuations versus a well respected small cap peer like NGL Finechem seem attractive, and versus the behemoth that is Divis this is very well priced (But obviously due to scale and history this is not a like to like comparison).

Some interesting aspects of Q3 commentary were that the business revenues are not too constrained by capacity - the revenues can increase/decrease depending on what product mix they end up selling and in what markets - my inference here was that probably margin/sales peaks happen in favourable times (Q4 21 and Q2 22) and very bad times could be troughs (Q2 and Q3 23).

Disclosure : Invested in the last 30 days, biased

3 Likes

One take away from concall on the china part, situation is very grim and sales would be limited as well considering the anti dumping duty by china if company crosses 45KL of any material by company. Company did catchup with other markets like North and Latin America in sales part. Otherwise the sales would have been worse.

2 Likes

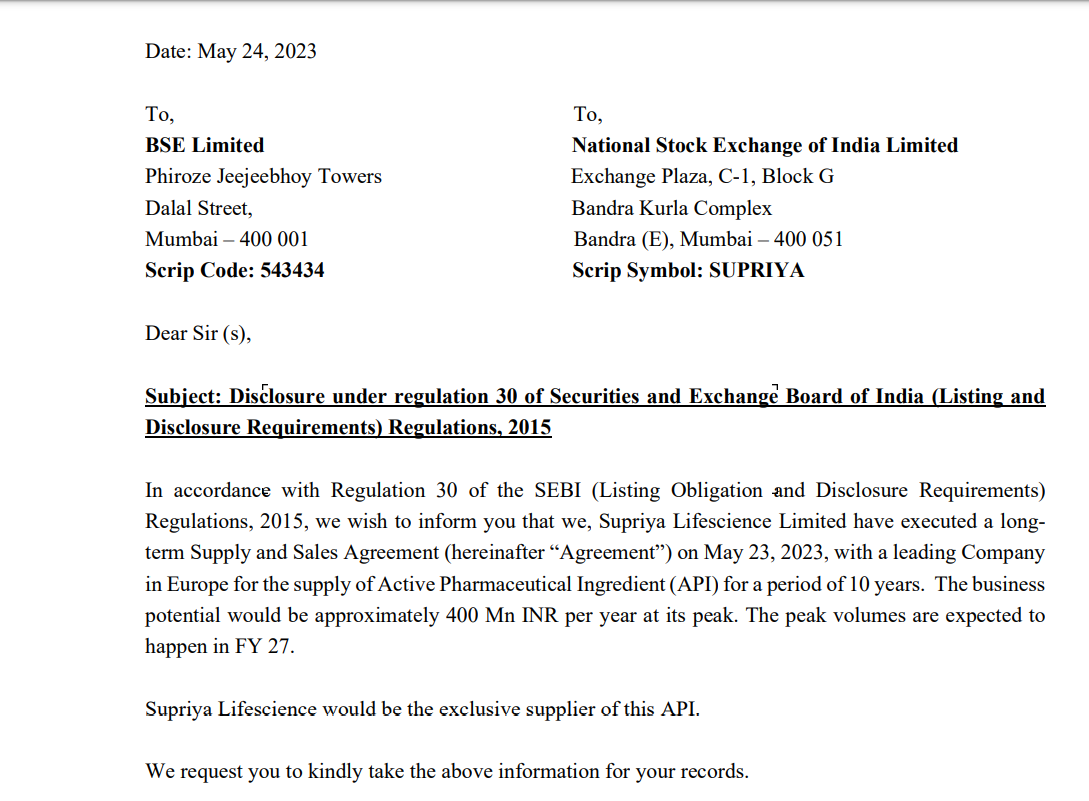

Microsoft Word - Cov Letter.docx (bseindia.com)

“Supriya Lifescience Ltd signs agreement with Kalinga Institute of Technology for development of first-of-its-kind novel oral cancer detection kit”

One thing missing in the company is patents. If the company is able to get some patents, it can propel the company into the next ladder of the value chain.

6 Likes

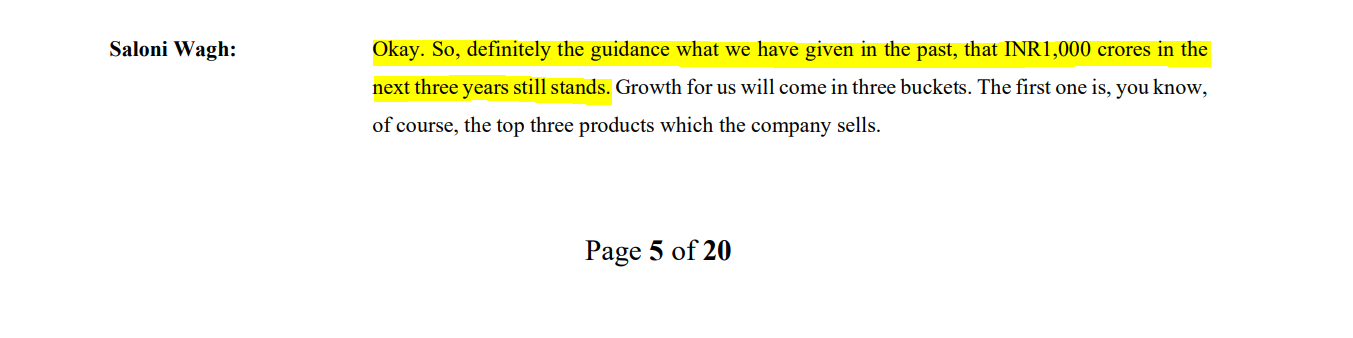

Started to look at the company recently. A few positives that I liked are…the company makes decent margins (28-30ish), is debt free, investing in expansion and R&D. The target which the mgmt has given that they could do 1000cr topline by FY27 could be achieved by following triggers (these triggers would also contribute growth beyond FY’27):

- 10 year vitamins API contract with DSM (european customer) which will have peak revenue of 40cr by FY27

- Contract with Plasma Nutrition for ioProtein, exclusive manufacturing and mareketing for Indian market involving tech transfer from the client.

- Contract with KIT for oral cancer detection kit, revenue from FY27

- Contract with KIT for GelHeal

- Revenue from regulated markets for the next 8-10 products, scale up of revenues from US and Brazil.

Considering the above triggers/drivers, feels like the company can achieve a growth rate of about 20% which will help reach 1000cr by FY27. They could surprise on the upside if all the above triggers fire. Assuming a NPM of 19% and a P/E of 20, they could double the market cap from current levels (1000cr x 0.19 x 20 = 3800cr) in about 4 years. That looks decent.

However,I have the following queries/doubts to which I will try to seek answers:

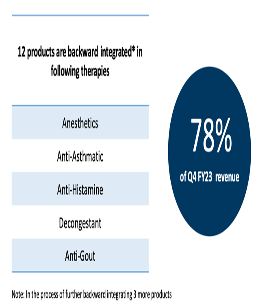

- When will their products count increase from current 38?

- The latest presentation states that 15 products are now backward integrated (earlier it was 12), with 3 more in the pipeline. Is this correct, and if yes, by when the backward integration will be achieved for the 3 pipeline products.

- When China market was doing well for us, what led us to believe that the pricing for the key product wont fall because based on that single product the company was hopeful of sustaining 40% margins (assuming that the volume cap was present even when we were getting good price leading to high margins).

- What is the expectations on CMO/CDMO business. It was expected that by Q1FY23 the contribution from CMO/CDMO would start. Has it happened, and what is the %. What is the medium term expectation. Would be great if the company can start quarterly disclosure of CMO/CDMO revenue.

- By when can we start seeing the contribution for the top 3 products start going down, and any medium term plan/expectations would be good to know.

Looks like it is possible to achieve 30% and above margins in API business. Divis had 35%+ for a long term, GLS also earns 30%, Supriya also is around the same. I have read that if in an industry more companies earn good margins, then valuations may not be high. Divis trades at high valuations, GLS trades at low valuations, Supriya is slightly higher that GLS. I havent looked at other peers, but Supriya looks like a decent investment idea which could give a 15-19% CAGR in around 5 years.

Disc: tracking

10 Likes

I have three questions with respect to their latest concall. They are as follows:

a) Inconsistent margins: The management mentioned in the latest conference call that they are entering more regulated markets like brazil and Mexico for better mix at the same time they also said that product mix is one of the leading factors in their ebitda levels. If we remove one of expenses. How much of a seasonality is there in the margins , what role is the product mix playing and what is the sustainable margins that they aim to deliver over a long term profile?

b)The new products that they are launching and have file patents for: how long does it in general take for patents and approvals like these to get approved? How certain is the management that they will get these approvals in the first place. Also company has already started capex on this, still there is no fixed timeline on the commercialization. The management says at least three years. Can it exceed that??

c)They said that 99% of the companies in china are failing to file for regulations for brazil. Why is that? and what moat do they have over the Chinese players as far as regulatory approvals are concerned?

have been tracking this company for few quarters, would love to understand these points from someone who has deep dived!

2 Likes

On the inconsistent margins, company has been informing in con calls that the different products has been introduced recently and the product mix that got sold in q1 and q2 is different. Hence based on the product mix it is inconsistent. However Saloni wagh was mentioning that they will try to maintain around 20 to 25. Currently their products are seasonal impacting. They are working on new products to reduce that as well.

One more great thing I have noticed is they have started bringing in key personnel in different positions to make organisation strong in r and d part and in production.

I guess this will take 2-3 quarters to show some change in numbers to be visible.

Lastly, the management started giving reduced guidance, down playing of actual situation. Looks like management has become sensible to stock market, a sign of maturity in their approach.

Disclosure: invested and my opinion might be biased.

4 Likes

Supriya Lifesciences -

Q2 FY 24 and company Highlights -

Revenues - 140 vs 112 cr

EBITDA - 32 vs 29 cr ( margins @ 23 vs 25 pc )

PAT - 24 vs 17 cr ( due lower tax outgo )

Geography wise sales breakup -

Asia - 35 pc

Europe - 44 pc

LATAM - 13 pc

North America - 4 pc

Others - 4 pc

Therapy wise sales breakup -

Analgesics/Anesthetics - 50 pc

Anti Histamines - 13 pc

Vitamins - 12 pc

Anti Asthmatics - 7 pc

Anti Allergics - 6 pc

Anti Malarials - 2 pc

Company produces a Niche product basket of 38 APIs. Exports them to 85+ countries

Company is the largest Indian exporter of 3 key APIs -

Chorpeniramine Maleate - Anti Histamine, used to relieve symptoms of allergy, fever

Ketamine Hydrochloride - An Anaesthetic

Salbutamol Sulphate - Used to treat Asthma, respiratory blockages etc

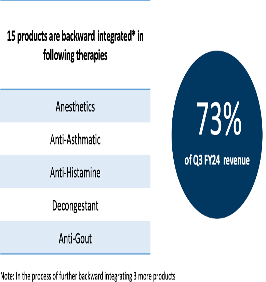

15 of company’s products are backward integrated and represent 72 pc of company’s revenues

Share of top 10 customers out of the total revenues - 45 pc

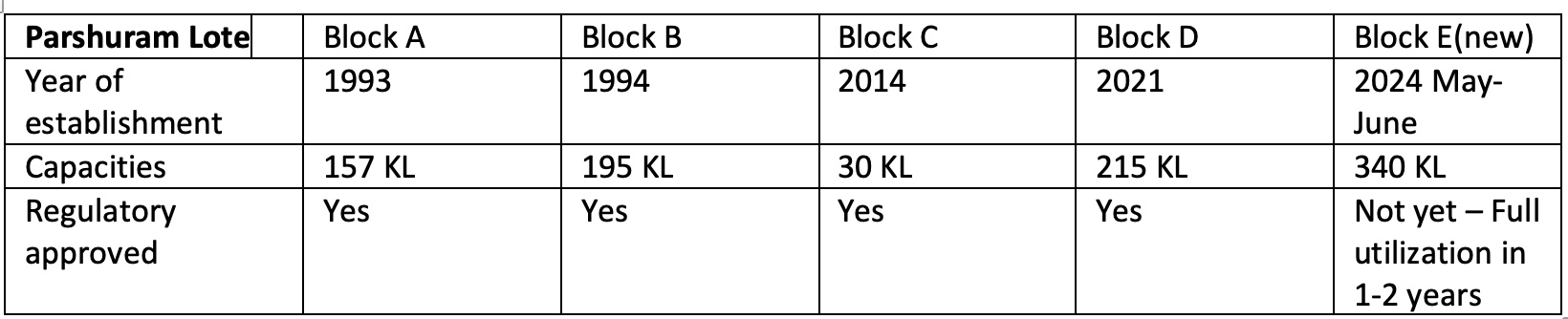

Company maintains 04 different manufacturing blocks - separated therapy wise. Land already acquired for future expansion

Total reactor capacity at 600 KL. Current capacity utilisation at 70 pc

Company’s facilities are recognised by key regulators - US FDA, PMDA, ANVISA etc

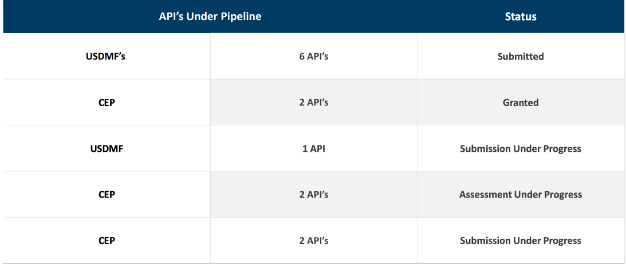

Company has already filed for 15 additional APIs with USFDA. This shall take care of company’s future growth prospects

Last 5 yrs -

Revenue CAGR - 13 pc

PAT CAGR - 18 pc

Leverage @ 0.03 pc

Company’s R&D centers at Lote Parshuram, Ambernath are involved in identifying APIs that will complement company’s current product profile. These centers are also engaged in lifecycle management and backward integration of existing products

Additional work is underway to set up 5th manufacturing block at Lone Parshuram which will have the capacity of 340 KL !!! Likely to be operational by Q4, FY 24

An additional manufacturing facility of 90 KL with a new R&D facility at Ambernath shall also come up by Q4, FY 24

All this will take company’s total manufacturing capacity to > 900 KL

Q2, FY 24 Concall highlights -

Company expects to generate a topline growth of 20 pc over the base of last FY ( that would mean, sales touching the 550 cr mark by end of FY 24 )

Tax rate for full FY to be around 26 pc

Company is practically debt free

Lower margins in Q2 due change in product / geography mix ( basically greater sales in semi-regulated and emerging markets )

Aim to maintain 28-30 pc EBITDA margins for full FY 24

Sales mix -

Exports : domestic - 81:19 pc

Regulated : semi-regulated - 46:54 pc

Most of the sales growth in Q2 attributed to volume growth

Generally, H2 is better than H1 for the company

In H1 … outside the top 4 products, the next 8-9 of company’s products did see a lot of traction in semi regulated markets and hence the strong volume growth

New products where the company is focussing are in the therapy areas of - cardiovascular, anti-diabetic and anti-anxiety products

Don’t expect any incremental volume growth from China business for next 2-3 yrs

Company is co-developing 02 revolutionary products with Kalinga university - oral cancer detection kit, fast wound healing gel. Both these are novel products and have already been developed at - lab scale. Expect Supriya to take them commercial inside 3 odd yrs. These can generate significant revenues for the company ( > 500 cr ). Company intends to manufacture them and out license them to global Pharma Majors

LATAM countries are aggressively pursuing procurement from countries other than China. This is likely to act as a huge tailwind for the company Management reiterated the same on multiple occasions

Expecting to grow revenues at rates > 20 pc for next 2 yrs as well

Disc: initiated a small tracking position, not SEBI registered, biased, not a buy/sell recommendation

11 Likes

Looks like product mix getting sold is changed for Supriya Life Sciences, as a result they are confident that cyclicality of reduced sales in first half of year would not be same going forward, as guided by management.

They are now targeting Latin America markets and aiming overall 28-30% EBIDTA margins.

20 percent overall revenue growth expectation remains same.

I see that with capacity utilization more than 2.5 times, they should post more than 20 percent, however lets aim for 20 percent growth. Iam happy to take this with both hands.

Overall good improvement in PAT numbers, even though top level was flat.

Anesthetics has good margins

2 Likes

Supriya Lifesciences

Sector: Pharmaceuticals - Indian - Bulk Drugs & Formln companies

About the company:

Supriya Lifescience Ltd. (SLL) is engaged in manufacturing of-:

-

Active Pharmaceutical Ingredients (APIs) with a backward integrated business model and advanced manufacturing capabilities.

-

Backward integration of API business, lead to better margins and reduce dependency on import of raw material

-

The company has diversified operational presence in 86+ countries with exports contributing to ~80% of its revenue in FY23.

-

SLL is the largest exporter of -:

-----Chlorpheniramine Maleate(45-50% export from india),

-----Ketamine Hydrochloride and Salbutamol Sulphate(60-65% export from india)

----with a niche product basket of 38 APIs as of 3QFY24. -

They were among the largest exporters of Salbutamol Sulphate contributing to 31% of the API exports from India in FY 2021 in volume.

-

Export contributes to 77.47% of FY2021 revenues, Company export to 86 countries to 1296 customers including 346 distributors

Strength and Investment Rationale

Niche product portfolio and robust launch pipeline

-

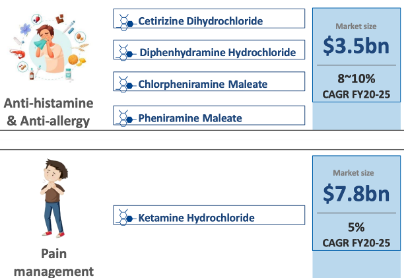

SLL has a niche product basket of 38 APIs with presence in therapeutic areas of Analgesics, Anti-histamine, vitamins, anti-asthmatics, anti-allergic and anti-malarial.

-

Company has tied up with Kalinga Institute of Technology for development of GelHeal and Quickblue Oral Kit.

Quickblue is an oral cancer detection kit which is cost-effective and efficient. Through Quickblue the company expects to create a 1%-2% market share in a USD 21.5 bn global cancer market

Quickblue kit to be commercially available in the next 3 years.

competitor is selling at INR32,000. trying to give it at a very cheaper price to common man , export is major target. -

Company has signed a memorandum of understanding with US-based Plasma Nutrition, which specialises in innovative consumer products, for manufacturing Ingredient Optimized Protein (ioProtein).

will get the sole rights for manufacturing and marketing ioProtein in India.

the trial batches and the samples have been supplied to all the large distributors of whey protein across India.

evaluating opportunity for exports also of this particular product in Southeast Asian market.

next quarter, will at least be having 20 to 30 metric tons of trial quantities from all the major distributors in India

Next financial year, it will commercialize about 100 metric tons. Let’s say quarter 2 of FY’25 is where we will see some significant volumes coming in.

next 2-3 years, anticipate that will be able to go to about 800-900 metric tons.

Robust manufacturing facilities

- Global agencies approved facility: USFDA, EUGMP, EDQM, NMPA, ANVISA(Brazilian), KFDA(Korea), PMDA(Japnese), TGA(Australia), COFEPRIS(Mexico), Taiwan FDA, Health Canada, CDSCO

- SLL has a total reactor capacity of ~550 KL/day with capacity expansion of 340 KL/day in the Parshuram Lote manufacturing block being commercialized by 4QFY24.

- The company is also on track to set up another pilot manufacturing plant and R&D facility in Ambernath by 1QFY25 which is set to increase capacity by ~70 KL/day.

- capex program at Ambernath site with an estimated aggregate capital outlay of INR 60 crore over the next 3 years

- With these projects the total capacity will increase from 597 KL to 960 KL by early Q1 FY25

- Company also setting up a bottling line in Ambernath for about 5 million bottles a year.

- In FY22, FY23 and 1HFY24 the company has incurred capex of around Rs 94.9 cr, Rs 107.8 cr and Rs ~50 cr respectively.

- The capex is majorly diverted towards capacity expansion to cater to growing product demand.

The capacity utilization rate as of 2QFY24 is 73%.

Strong focus on R&D

- New R&D facility Has one research lab in its Parshuram Lote facility with another lab in Ambernath to be operational by Q4FY24- Q1FY25.

- These centres will help to develop identified APIs which will complement existing product profile. Ambernath would be around 70 to 100 KL depending again on the kind of product mix, it is multiproduct facility.

- SLL’s R&D efforts are mainly focused across the value chain of API process development and consistent efforts towards

developing new products

improving existing products and drug delivery systems and

expanding product applications. - In FY21, FY22 and FY23 the company spent 3.9%/6.8%/4.8% of its revenue on R&D (includes capital and revenue expenditure).

Market Reach:

- Expanding the controlled drugs portfolio with identified APIs in the development pipeline.

- Evaluating product portfolio expansion in anti-diabetic and CNS segments.

- Strengthening presence in existing markets through a dedicated sales team and regulatory team registrations.

- Actively pursuing business expansion in North America, Japan, Australia, and New Zealand.

India is emerging as key player in CDMO segment

- Global pharmaceutical players are continuously witnessing cost pressures and looking for ways to shorten time to market.

Thus, the industry is looking for established CDMO partners, particularly in Asian markets such as India and China - India is a preferred destination for the procurement of active pharmaceutical ingredients (APIs), especially in regulated markets, compared with China

Initiated discussion with various companies ranging from big pharma to innovator companies to work as a partner for supplying products as per their needs - In Nov 2023, announced 10-year CMO contract with a leading European company - DSM Firmenich is expected to generate peak revenue of INR 40 crores/year starting from FY27.

received first commercial order from DSM Firmenich in FY24Q3 - Company has set up a bottling line of around 5 million bottles a year. On the finished formulation front, this product is extremely large. It is the most widely used anaesthetic globally.

current market value of the product is around USD300 million. And it is growing very, very strongly. It is expected to grow at a 4.4% CAGR year on year. - Expects this business to contribute ₹100-120 crore to the revenue in the next two-three years.

What went wrong in FY23?

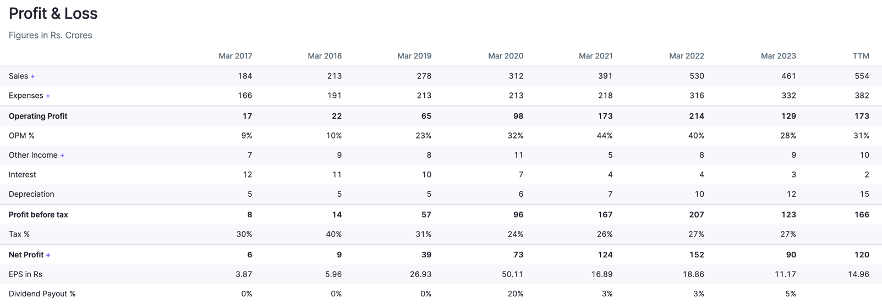

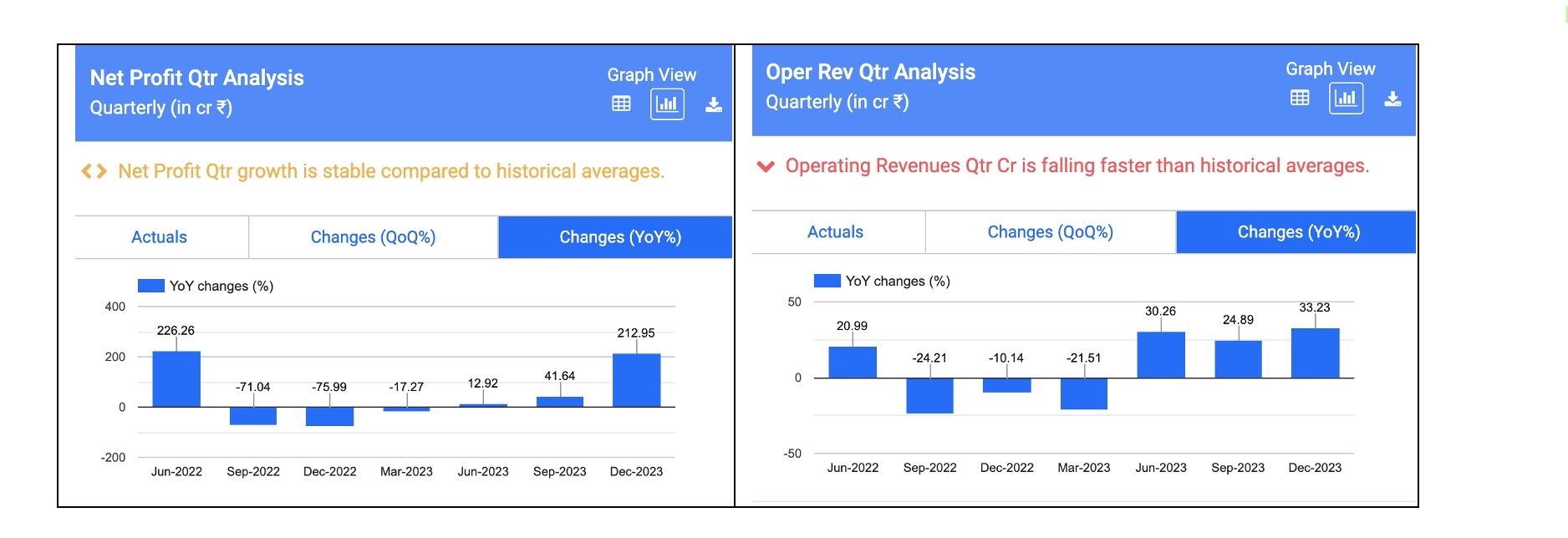

After strong set of numbers in FY22, Supriya reported dismal numbers in FY23. Revenue declined 13% while EBITDA/PAT declined by 39%/41% in FY23.

The fall in revenue was on account of low demand from the Chinese market for its key therapy i.e. Anti-histamine. Considering that China was the company’s largest export destination, marked by value-added exports, the impact translated into a decline in margins in FY23

Due to the COVID in China, usage of hand sanitisers and masks increased and people staying indoors; thereby the demand for its antihistamine range significantly dropped.

Management had highlighted that improvement will be gradual and it will take another 2-3 quarters for the situation to normalise.

Due to Covid cases inside China in FY23, a key material supplying country, raising the threat of interrupted production.

-

The company proactively stocked raw material inventory, protecting its manufacturing schedule.

-

Mitigation: The company entered in relationships with key material suppliers in India, moderating the dependence on a global supply chain.

Further, to mitigate this impact, Supriya is expanding regulatory market presence, optimizing manufacturing capacity, and diversifying product offerings and geographic reach.

Company initiated registration for other therapies such as Decongestion, Anti-hypertensive, Anti-Asthmatic, Vitamins and Antiallergic.

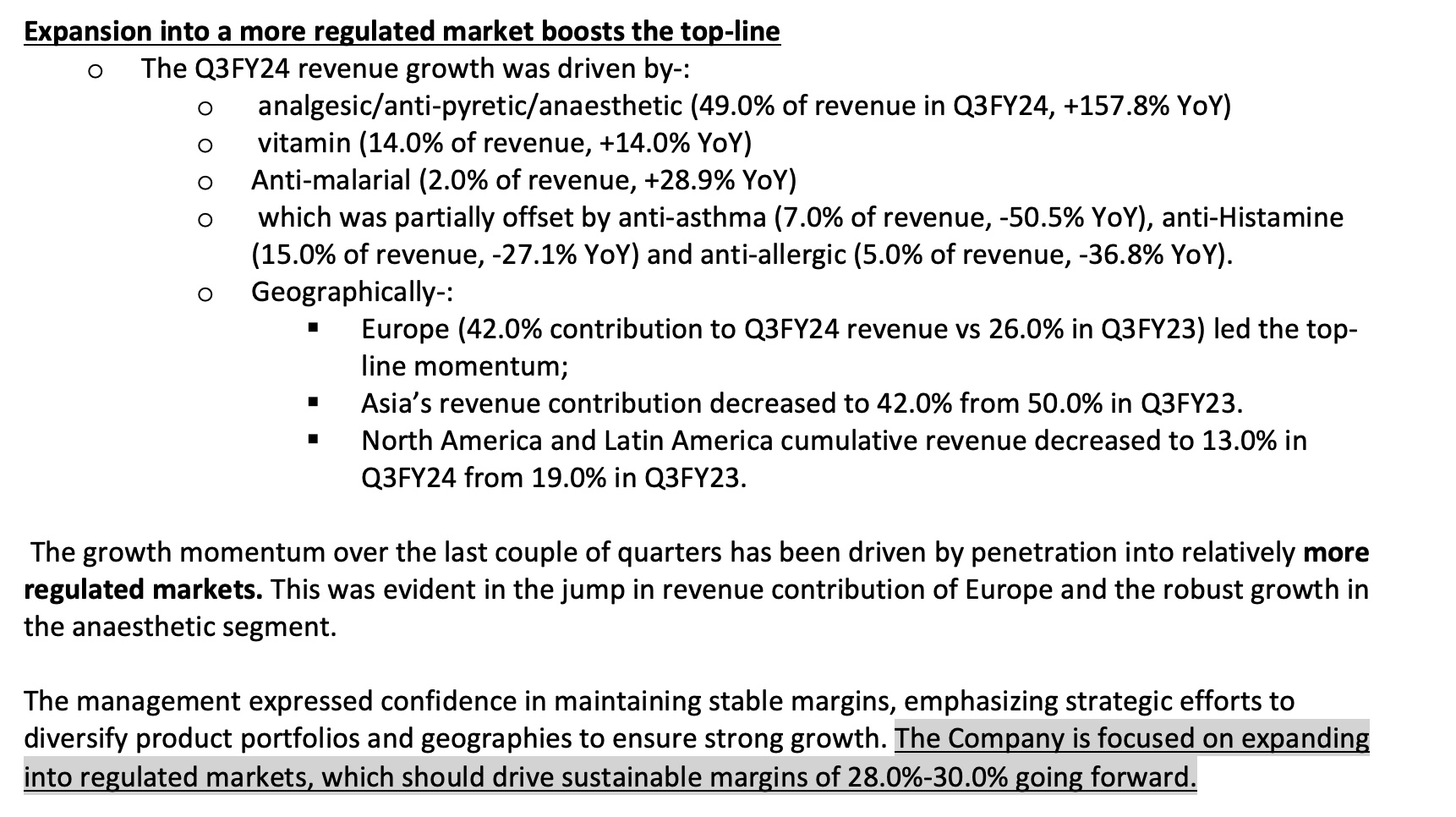

Result Highlights for Q3FY24:

Key Concal Highlights:

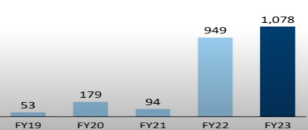

Product/Sales Mix – YoY comparison

FY22Q4:

FY23Q4

FY24Q3

Fundamentals

2022- 2023 was due to covid and recovery from issue with supplying to China , recovered by diversifying – geography , product range and getting a new broker for China buyers

Now recovered to IPO levels in 2021

Capex Spend

Company is using – internal accurals and 200 crore capital due to initial IP

Holding

Positives

Negatives

Industry Growth

• In 2024, Analgesics market revenue in India is INR US$1.12bn, an annual growth rate of 8.46% (CAGR 2024-28) is expected

• Anaesthesia Drugs market is to grow at a CAGR of 3.47% between 2021- 28. As of 2021, the market for anesthesia Drugs market size reached USD 7 Billion.

• Global Antihistamine product market was valued at US$ 263.9 billion in 2022 ,expected to expand at a CAGR of 8.6% and reach a valuation of ~US$ 647.7 billion by 2033.

• Global vitamins market is expected to be $6.7 billion in 2023 and more than $8.9 billion by the end of 2028, with a CAGR ~6.0% from 2023-28.

• Global small molecule CMO/CDMO market is around US$ 74,998.1 Million in 2024 , to exhibit a CAGR ~ 5.2% over the period 2024-34.

Pharma Growth

• Global pharmaceuticals market was valued at USD 1.4 trillion in 2021 and is expected to reach USD 2.06 trillion by 2028, growing at CAGR of 5.70% during 2022- 28.

• In 2023, North America is to account for 45.33% of the global market share. Asia-Pacific is expected to remain the second largest market with 24.07%, followed by the European market (20.24%), Latin America (7.53%) and Middle East and Africa (MEA) (2.96%).

The increase in the number of senior citizens who are prone to catching illness as well rising cases of illnesses such as diabetes and cancer is expected to contribute to this growth

Global API industry Growth

• The worldwide active pharmaceutical ingredients market was pegged at 222.4 billion in 2022 and estimated to grow at a CAGR of 5.90% from 2023 to 2030.

This growth is attributed to factors such as growing cases of cardiovascular diseases and cancer, conducive government policies for API production as well as changes in geopolitical situations

Indian API industry Growth

• By 2029, the global generic API markets are expected to grow at ~6%, whereas the Indian market is expected to have a CAGR of 13.7% from 2023-29.

• The Union Budget 2023 enhanced the fund allocation by 12x from H100 cr for 2022-23 to H1,250 cr for FY24 including drugs and medical devices

Over the last couple of years, the Indian API industry has received USD 4-5 billion investment, which also include venture capital

Leadership

**Dr Satish Wagh**

Established in the year 1987, Supriya Lifescience Ltd. is the largest producer of anti-histamines, anaesthetics & anti-asthmatics in the world and has put Maharashtra and India on the world map in the pharmaceutical sector. Dr. Satish Wagh is the Founder & CMD of the company. Additionally he was also the chairman of CHEMEXCIL for 22 years. He was also listed in ‘Forbes powerful Performers 2021’ and ‘Economic Times Most Influential Leaders of 2022’

Risk

Revenue concentration risk:

• Company faces product concentration risk as top-5 products contribute major portion of their revenue. Any delay in development and commercialization of newer products could impact future growth prospects of the company.

o Adding new products and in the process of implementing additional manufacturing facilities, effectively reducing the risk associated with location concentration

Foreign exchange fluctuations may impact the company as more than 80% of revenue come from exports sales.

• Company’s inability to effectively utilize its manufacturing capacities could have an adverse effect on the business.

Competitor Risk

• The presence of multiple prominent pharmaceutical firms enhances competition within the pharmaceutical sector.

• chooses products which are mature and where demand is not likely to taper off soon.

• This presents a difficulty for the Company to improve its market share and overall profitability.

• The Company’s extensive operational capacity, backward integration, and regulatory influence have enabled it to demonstrate an expanding order book from regulated markets

Customer concentration risk

• 48% of revenue from Top-10 customers, and the potential loss of one or more of these clients, their weakened financial outlook, or a decrease in their demand for our products could negatively impact our business outcomes. T

Company is experiencing positive momentum in its Contract Manufacturing Organization (CMO) and Contract Development and Manufacturing Organization (CDMO)

Market risk:

• The development and commercialization processes of new products is resource-intensive and time consuming

consistently create and introduce new products

IT risk:

• Pharmaceutical sector undergoes rapid transformations due to technological progress and scientific breakthroughs.

Company is engaged in establishing 2 additional manufacturing units while also enhancing its current infrastructure, emphasizing the integration of cutting-edge automation technology.

Credit risk:

• Handles credit risk through procedures like credit approvals, the establishment of credit ceilings, and ongoing assessment of the creditworthiness of customers

For export transactions, every sale is safeguarded by ECGC, while domestic sales benefit from trade credit coverage.

Regulatory risk:

• Failure to adhere to the regulations stipulated by governmental bodies and regulatory agencies can have adverse effects on the Company’s business, financial outcomes, and operations

• markets such as the USA and Europe where its products are sold, the Company’s manufacturing facilities and products must receive approval from regulatory authorities before distribution agents

• many of these approvals necessitate periodic renewal

Only Family in Board Leadership

- If Company doesn’t effectively utilize its manufacturing capacities it could have an adverse effect on the business.

Things that is not yet clear( Needs to be understood More):

- Inventory Turnover Ratio: 1.94 – Average-okish, previously during 2022 was very high as 4.5+

sales maybe slightly weak and product demand might be waning. This could result in excess inventory on the warehouse shelves and wasted space and resources. - Would be good to get company’s export data and see how the change in export trend is for company

My outlook for Supriya Lifescience

Reasonable valuation

• At current price, the stock trades at FY24E/FY25E consolidated PE of 21.2x/17.5x respectively. The company’s current capacity is ~550 KL/day which would be doubled in the next financial year to ~1070 KL/day adding topline growth of 20%-25% CAGR between FY23 to FY25.

o Company guidance - strong double digit revenue growth along with margin in the band of 30-32% in the next 2 years.

• Company intends to enter the pain management, anti-anxiety and anti-diabetic segments , vitamins and protein powders- sustainable growth opportunities.

• Company was able to continue the growth momentum by penetrating into regulated markets such as Europe where the revenue contribution has significantly increased.

• With consistent growth of 25% , company should be reaching revenue of 1000 crore over 3 years.

o Prediction(Subject to Risk and Market): FY24E Revenue(current) – 550+ , FY25E- 660+, FY26E -800+ , FY27E-1000+

• This should result over slow growth in stock and stock price growing from 350 to 700+ in next 3 years, yearly price growth average of 20-30%

Recommended Buy -Needs to be revisited on FY24q4

Sources : Trendlyne, Screener, company website, News Articles, Company presentations, Earning calls, HDFC securities report, and ofcourse Google

26 Likes

My only concern is why Malabar first entered and the. Exited quickly.

Disc. Not invested

2 Likes

In 2021 Dec, company got listed, 22-23 was a bad year for company due to heavy dependency on China and Covid impact. During the last 1-2 quarters, company shifted its focus from China to Regulated markets and that is reflected in margin from geographies. Also Capex spent was slightly delayed in terms of capitalisation by 1-2 quarters.

But a company which is doubling its manufacturing, getting into new markets(and getting traction), doubling its RnD, and also doubling its partnerships (albeit the outcome of partnership will materialise in next 2 years) is a stock to watch out in near future.

Companies which may have a temporary setbacks but have a strong roadmap ahead and is having multiple growth paths are the ones which we might get at a decent valuation.

Beauty lies in the fact that Capex is mostly going to be funded by its internal accruals and minimum debt.

Check this Video, Will give you little more insight about company, Chairman talks about supriya vision and you can see the insides of manufacturing factory -:

6 Likes

Supriya Lifesciences -

Q3 FY 24 results and concall highlights -

Revenues - 140 vs 105 cr ( up 33 pc )

EBITDA - 41 vs 14 cr ( margins @ 30 vs 13 pc !!! )

PAT - 30 vs 10 cr ( up 200 pc !!! )

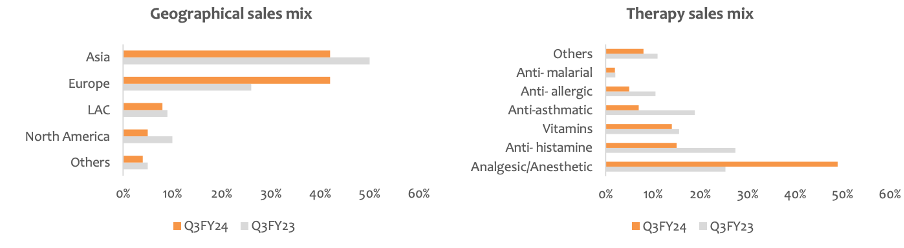

Geography wise sales mix -

Asia - 42 pc

Europe - 42 pc

LATAM - 8 pc

North America - 5 pc

Others - 4 pc

Therapy wise business mix -

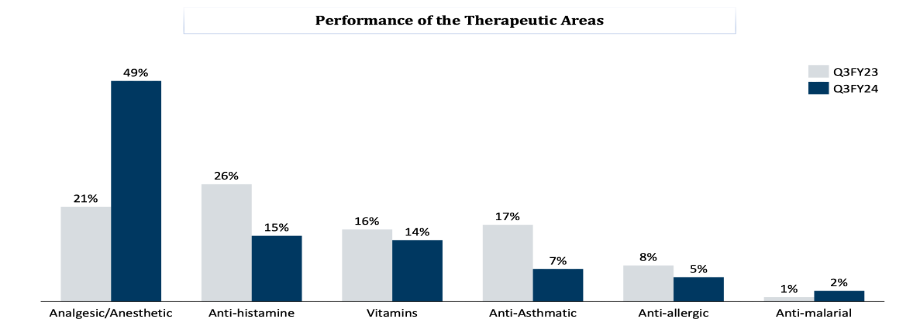

Analgesics + Anesthetic - 49 pc

Anti-Histamines - 15 pc

Vitamins - 14 pc

Anti-Asthmatic - 7 pc

Anti- Allergic - 5 pc

Anti- Malarial - 2 pc

Company overview -

Niche portfolio of 38 APIs

Exporting to 86 countries

Reactor capacity @ 597 KL / day

04 separate manufacturing blocks - separated therapy wise

Largest exporters of - Chlorpeniramine Maleate ( Anti - Histamine ), Ketamine Hydrochloride ( Anaesthetic ) and Salbutamol Sulphate ( Anti -Asthmatic ) from India

15 of company’s key products are backward integrated. They represent 73 pc of company’s sales

Export sales as a percentage of total sales @ 80 pc

Top 10 customers represent 45 pc of total sales

Company has acquired adjacent land parcel for future expansion. Have also purchased a land parcel 20 km from their existing site for backward integration projects

Company has spent 60 cr towards a new CDMO facility. Should go live by end of Q1 FY 25

Four new products from Anti-Diabetes, Anti-Anxiety and Aesthetic therapies are lined up for launch in FY 25

Company believes that a sustainable EBITDA margin for them should be between 28-30 pc for medium to long term. Company guiding for > 20 pc growth in revenue ( CAGR ) for next 3 yrs

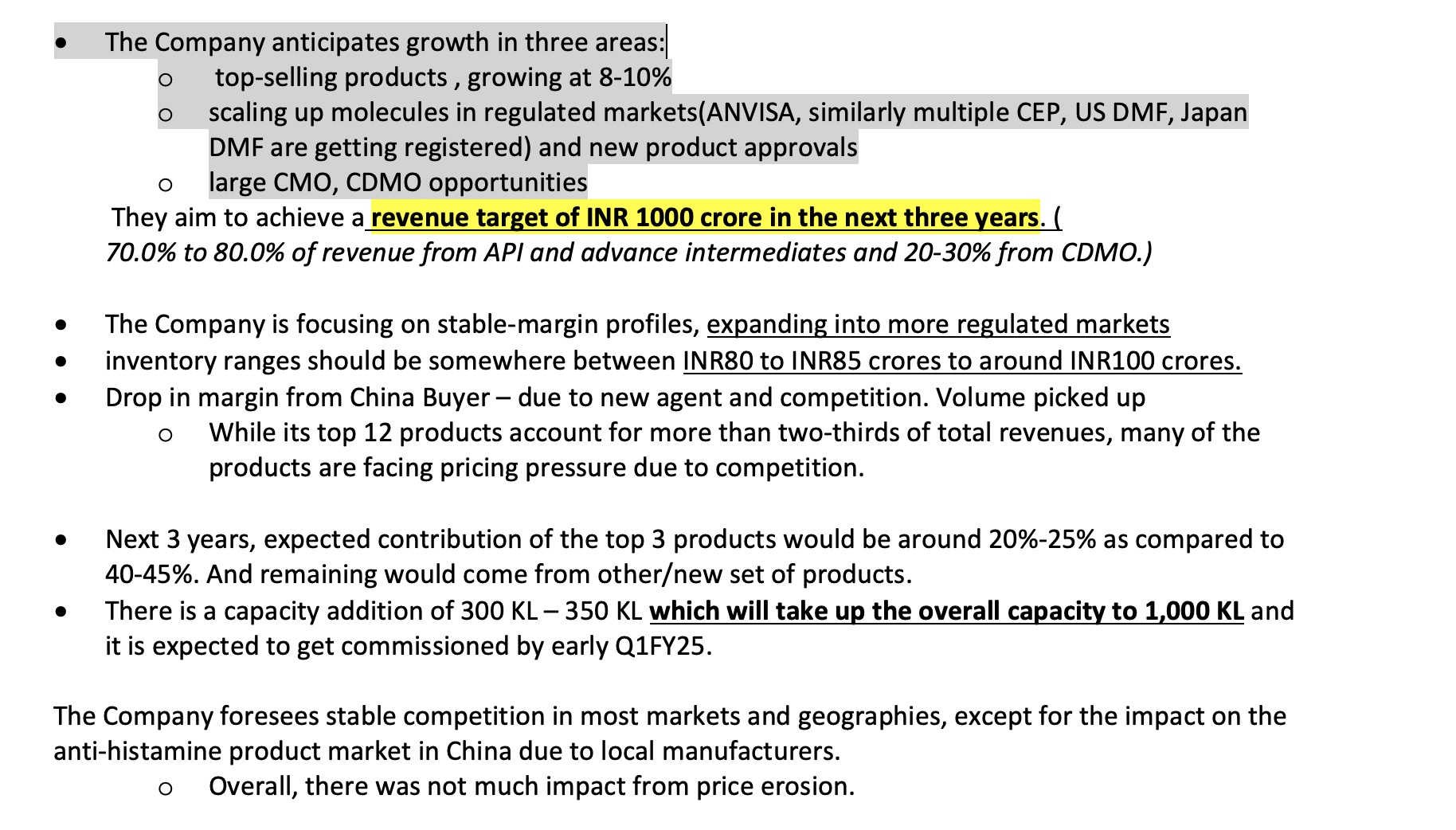

Aim to hit a 1000 cr topline in next 3 yrs. Major growth drivers should be -

Descent growth should continue in company’s top 3 molecules

Company has a basket of 8-10 molecules that are now scaling up well in the regulated markets

Company expects CMO/CDMO to scale up well. Already have got a descent size contract for an export substitute anti-anaesthetic molecule. Most countries including US, EU, India are dependent on China for this prodct. Once the company ramps up this product, it can potentially be a large molecule for the company. Plus the company is likely to get more opportunities

LATAM countries have completely revamped their regulatory framework. It has a become far stricter now. Company expects its LATAM business to accelerate going fwd as they have just cleared the Brazilian Audit in Jan 24

From Q2 FY 25, company will start commercial supplies of Whey Protein. This will further add to the revenue growth. Company expects to ramp up commercial supplies to 800-900 MT/yr iro Whey Protien

Currently, the top 3 products contribute to 45 odd pc of the revenues. In the next 3 yrs or so, company expects this to come down to 25 pc of revenues as other products ramp up

Expecting higher topline in Q4 vs Q3 with margins @ 28-30 pc

Disc: holding, added today, biased, not SEBI registered

8 Likes