Since I could not find any discussion with regard to the captioned company,i am starting a new thread on the same. I think that Sunteck makes for a good investment opportunity. Please find below my investment thesis which i have also published on my blog. I have initiated a position in this and safe to assume that my views are biased.

Sunteck Realty

I have been looking at Sunteck Realty stock with a lot of interest lately and my conviction has increased quite a bit over the last couple of weeks since I have been researching the company. It all started when i noticed the beautiful projects of Sunteck (Signature Island, Signia Isles and Signia Pearl) in Bandra Kurla Complex (BKC) where I go for running. I dug a little deeper and found that they have an existing JV with Piramal Realty (Piramal Enterprises being my largest holding) and that Ajay Piramal is invested in the company in personal capacity. That was enough to arouse my curiosity and send me scurrying for more. Here is what i found:

Summary

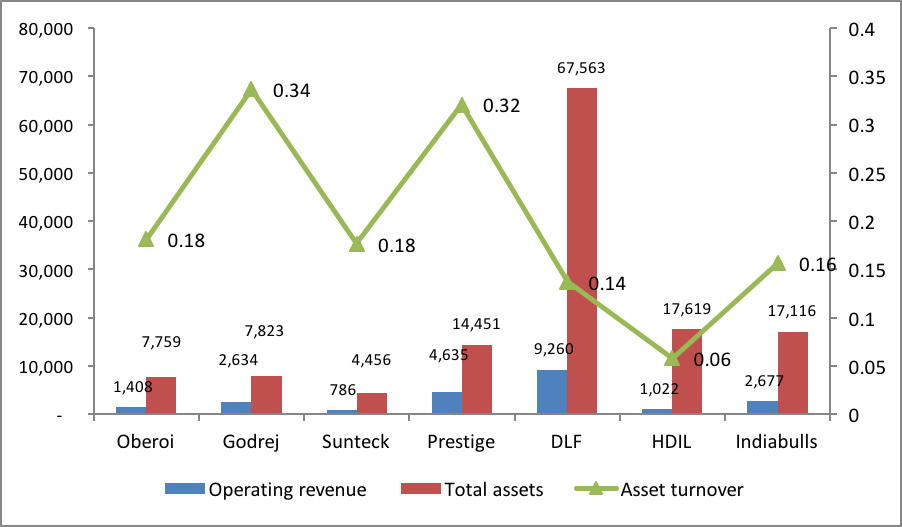

Business: Real estate is a difficult business due to a variety of reasons but it can earn a good return if it is being run by a disciplined and honest management. Additionally it is a cyclical business whose fortunes are tied to the health of the economy. Sunteck is a quality real estate company which has got a first rate management. It is even more cyclical than a typical real estate company because it plays in the luxury end of the segment. Currently, the stock price of Sunteck is depressed because of couple of reasons - 1) Real Estate industry is going through a protracted downturn, 2) There has been a lot of volatility in reported financial numbers of Sunteck as they use the project completion method unlike the more commonly used - percentage completion method.

Sunteck Realty began operations under the brand name Sunteck in 2000 as a corporate business center operator in Bandra Kurla Complex, Mumbai. It acquired Insul Electronics, a BSE listed company in July 2005. After acquisition the name of Insul Electronics was changed to Sunteck Realty and Infrastructure which was further changed to Sunteck Realty in Nov 2007.

Sunteck caters to the ultra-luxury and luxury residential segment in addition to commercial segment. It currently has city centric development portfolio of about 23 m sq ft spread across 25 projects at various stages of development and 4 rented assets with annuity income streams.

Performance so far

During the last 8 years (FY09-FY16), Sunteck has started recognizing revenues from completed projects in only 3 years - FY14-FY16. Before FY14 none of their projects had reached completion and so they did not recognize any revenues from these as they follow project completion method. Their average return on equity during these three years was 13%. Average over the past 3 years is a better way to measure their returns due to lumpiness of the revenues. While the returns are not great, when looked at the backdrop of dismal state of the real estate industry it is not too bad. I’m sure there is scope for improvement in their performance in the future. This will happen as they get better at execution with experience and the state of the real estate industry improves as the demand comes back.

What makes Sunteck different:

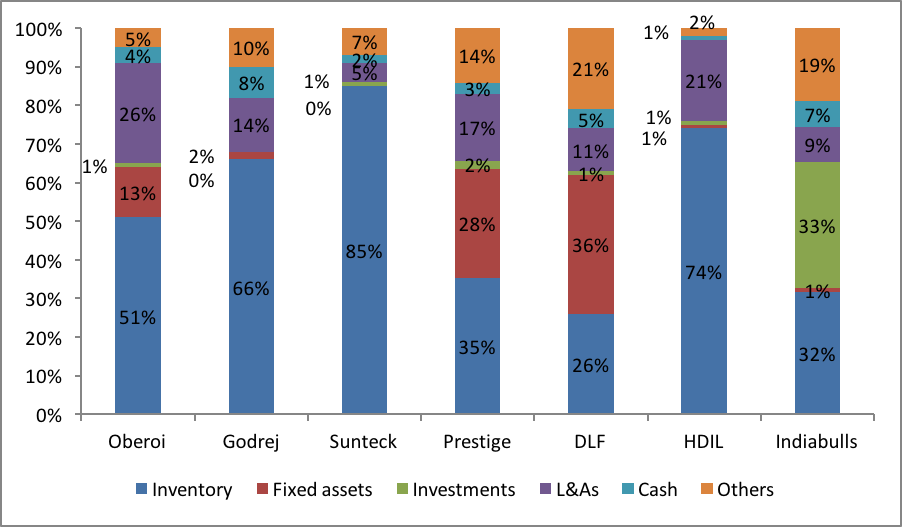

- Land as an inventory

Many real estate companies purchase and maintain large land banks for future development. In the meantime they show the land as an asset on the balance sheet. When a company does that, their capital in the form of land does not earn any returns which depresses the return on capital.

Sunteck on the other hand does not treat the land as an asset but as an inventory. All the land owned by Sunteck is under development and in this way they are able to churn their assets quickly and earn better return on their capital. Which brings me to the next thing - financing.

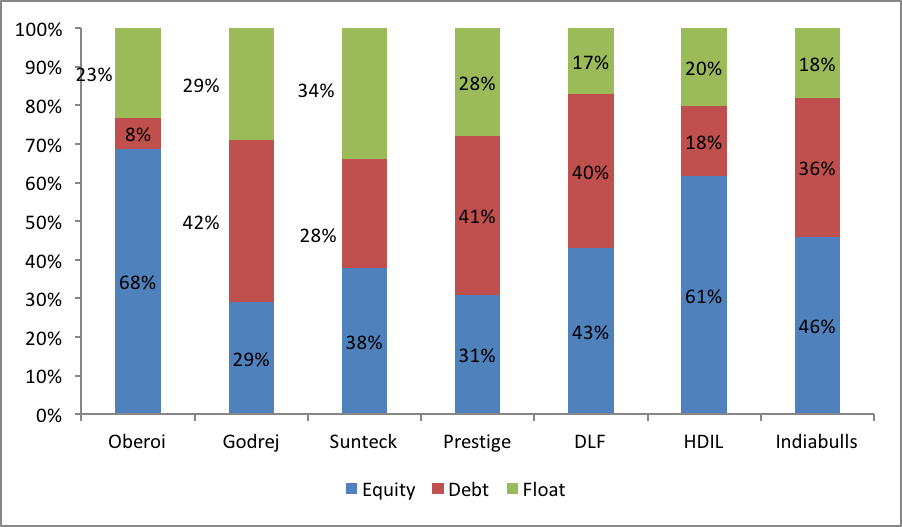

- Financing

In an effort to maintain huge land banks, lot of real estate companies have over-leveraged themselves. However, it is never a good idea to have too much debt and it is outright criminal to do so in a cyclical industry. Because when the downturn comes, which it inevitably will and the demand suddenly goes out, the overleveraged ones are caught with their pants down at exactly the wrong time. In this case, they are forced to sell their assets to bring down the debt to manageable levels, again at exactly the wrong time since they are likely to get depressed prices for their assets (land) due to the recessionary demand.

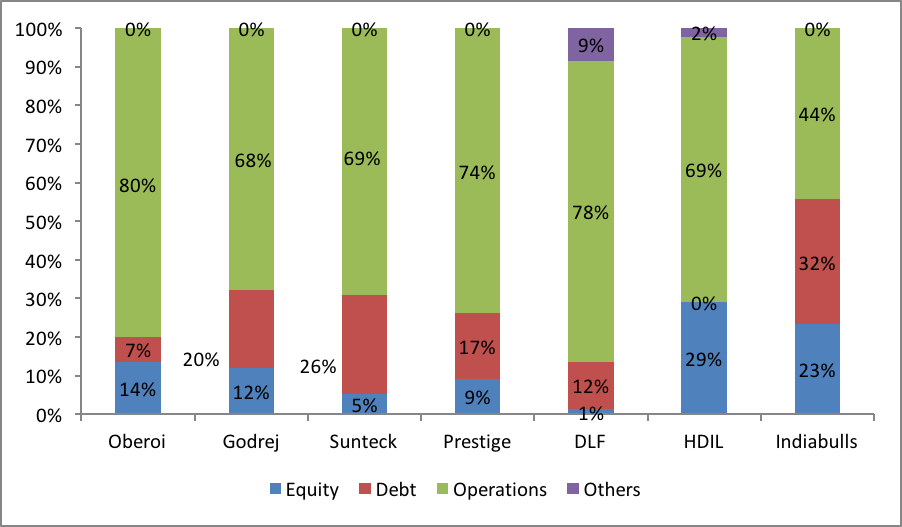

Here again Sunteck has used minimal leverage historically due to conservative nature of the promoters. First of all their land as an inventory policy has helped them and they do not need as much capital. Secondly, they have used a good mix of equity (very little), debt and customer advances to fund themselves.

-

Timing

Like in all cyclical industries, timing is of great importance in real estate as well. Generally like in other commodity industries, in real estate as well companies follow herd mentality and they all rush in to add capacity at the same time which sows the seeds for the next downturn. In terms of timing, what usually happens is most of the capacity addition takes place at the top of the cycle when the prices are at their highest. Sunteck on the other hand has a contrarian approach and have been buying land at distressed levels in the current downturn from other real estate companies who are forced to sell to bring down their debt. -

Promoters

The company is led by Kamal Khetan who is a first generation entrepreneur who founded Sunteck in 2000. The promoters have consistently increased their shareholding by buying shares in the open market from 65% in 2010 to more than 73% in 2016. Piramal Group has also reposed their faith in Sunteck - they have an existing JV with Sunteck called Sunteck Piramal Realty. In addition, Ajay Piramal has invested personally in Sunteck by picking up a 3.5% stake in the company in March 2014 and later increased the stake to 4.63% by March 2015. Coming to the remuneration of the promoter, Mr. Khetan has been taking quite modest salary from Sunteck - 2010: 35 la, 2011: 59 la, 2012: 70 la, 2013: 75 la, 2014: 2.97 cr, 2015: 1.6 cr.

However, what really sets the promoters at Sunteck apart is that they voluntarily decided not to take any dividend during FY2014 and FY2015. During these years the dividend was distributed only to non-promoter shareholders and the promoters voluntarily waived their right to get the dividend. They forego of dividend which would have amounted to INR 4.65 cr in FY 2014 and a similar amount in FY 2015. I can think of very few promoters (unthinkable in real estate) who would do such a thing. -

Valuation

Currently, Sunteck is available at very attractive valuation of INR 1400 cr. Let us look at valuation from couple of perspectives.

a) If as an owner of Sunteck, i want to do a firesale, how much would i demand from a prospective buyer as a minimum consideration. This should be equal to the amount of funds i have put into buying land and construction of the ongoing projects. In other words this would be value of inventory (which is funded through equity, customer advances and debt) less customer advances less debt. At the end of FY16 this value comes to 3768 (inventory)-917 (customer advances)-1208 (debt) = INR 1643 cr. As we can see this quality real estate company is selling at firesale valuations.

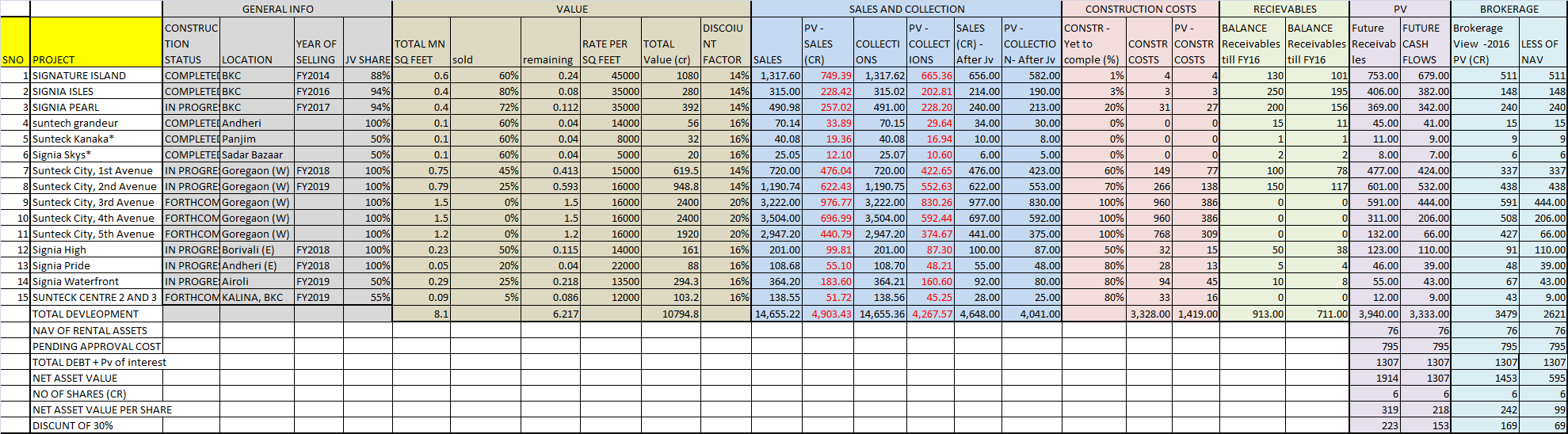

b) Secondly, let us try to do a valuation from cash flow perspective. For that please take a look at the table below taken from the Q3’16 update from the company. The table gives details about the ongoing projects of the company. All figures in INR cr. Since the company uses project completion method for revenue recognition, they have yet not recognized any revenues from the projects which are not 100% complete. Revenue to be recognized from the ongoing projects comes to INR 7,600 cr. - inventory for the first five projects and project size for the remaining projects. Assuming that all the projects will be completed over the next 8 years gives us average sales of INR 950 cr per annum and average net profit of INR 235 cr (assuming 25% net margin). This gives us a conservative valuation of 2,350 cr assuming a P/E of 10. This also assumes that they will not have any revenues from any other projects over the next 8 years.

Completed Project size Sunteck Share Pre sales Inventory

Signature Island Yes 2,570.7 100% 1127.7 1,474.0

Signia oceans Yes 62.9 50% 62.9 -

suntech grandeur Yes 101.4 100% 57.7 43.3

sunteck kanaka Yes 69.4 100% 26 45.0

signia skys Yes 56.9 50% 18.8 38.7

signia isles No 1,376.0 100% 941.3 417.0

signia pearl No 1,469.7 100% 883.4 557.1

sunteck city 1st avenue No 1,208.2 100% 329.5 768.7

sunteck city 2nd avenue No 1,324.2 100% 232.4 1,061.1

signia high No 289.6 100% 126.1 162.0

signia pride No 97.9 100% 10.9 83.3

signia waterfront No 263.3 50% 26.2 238.7

sunteck center II No 122.5 100% 0 128.5

Finally let me talk about the big picture and the overall prospects of the real estate industry specifically in Mumbai. Although Sunteck has presence outside Mumbai in a few places including Goa and Nagpur but their focus will continue to remain on Mumbai in the foreseeable future. While a lot of people tend to believe that Mumbai real estate market is saturated with so much development happening, in my opinion we are just scratching the surface. The landscape of Mumbai will be transformed over the next 10-15 years. Mumbai is developing like a hub and spoke model - with multiple hubs (such as BKC, Goregaon) which contain mixed commercial and residential developments and connected to other hubs through spokes.

So here we have a company which is a quality real estate developer. The company is conservative not only with respect to leverage which it uses sparingly but also in its revenue recognition principles. Additionally this is being run by management with a lot of integrity who are managing the company for the long term benefit of their stakeholders and do not mind taking some short term pains for the same including foregoing personal wealth. They want to create wealth for their shareholders over the long term and not off of them as is usually the case with real estate industry. It is no surprise that stock market does not like this company because stock market is obsessed with short term performance and abhors too much volatility in revenues. It is penalizing this company for their conservatism.

But i have not doubt that in the future as more of their projects get completed, they will reach a higher plateau in terms of revenues. Additionally, the real estate market which is in the dumps right now will inevitably come back roaring. The reversal in the market sentiment is a matter of when rather than if. And when that happens, the stock market will take notice. The trigger for the correction in undervaluation is three fold here - 1) Even if there is no change in sentiment with regard to the industry and the performance of the company remains as it is, I have shown above that the company is still undervalued 2) Their performance should improve over time 3) The real estate pendulum will swing again from from too much pessimism to too much optimism. As all of this takes place i’m happy to hold on to this and wait for the rewards alongside the management.