One big news coming up.

Can someone explain the part where ril is planning to buy from open market for price 375 and CMP is 430+.

What happended to other companies in similar situations?

Disc - Invested

Discussion about Sterling and Wilson Renewable Energy Limited’s current and future plans.

I believe it’s positive news for SW.

It sent the stock rocketing. It’s hugely positive. IMO it will steady down and give chance to buy.

Reliance Industries Limited arm grants ₹750-cr Loan to Shapoorji Pallonji Company. Is this anyway create impact to Sterling and Wilson? Any views.

Good News (I think)

18.48% of Pledged share of S&P group has been released by HDFC.

Any opinion?

Q4 FY22 conference call audio

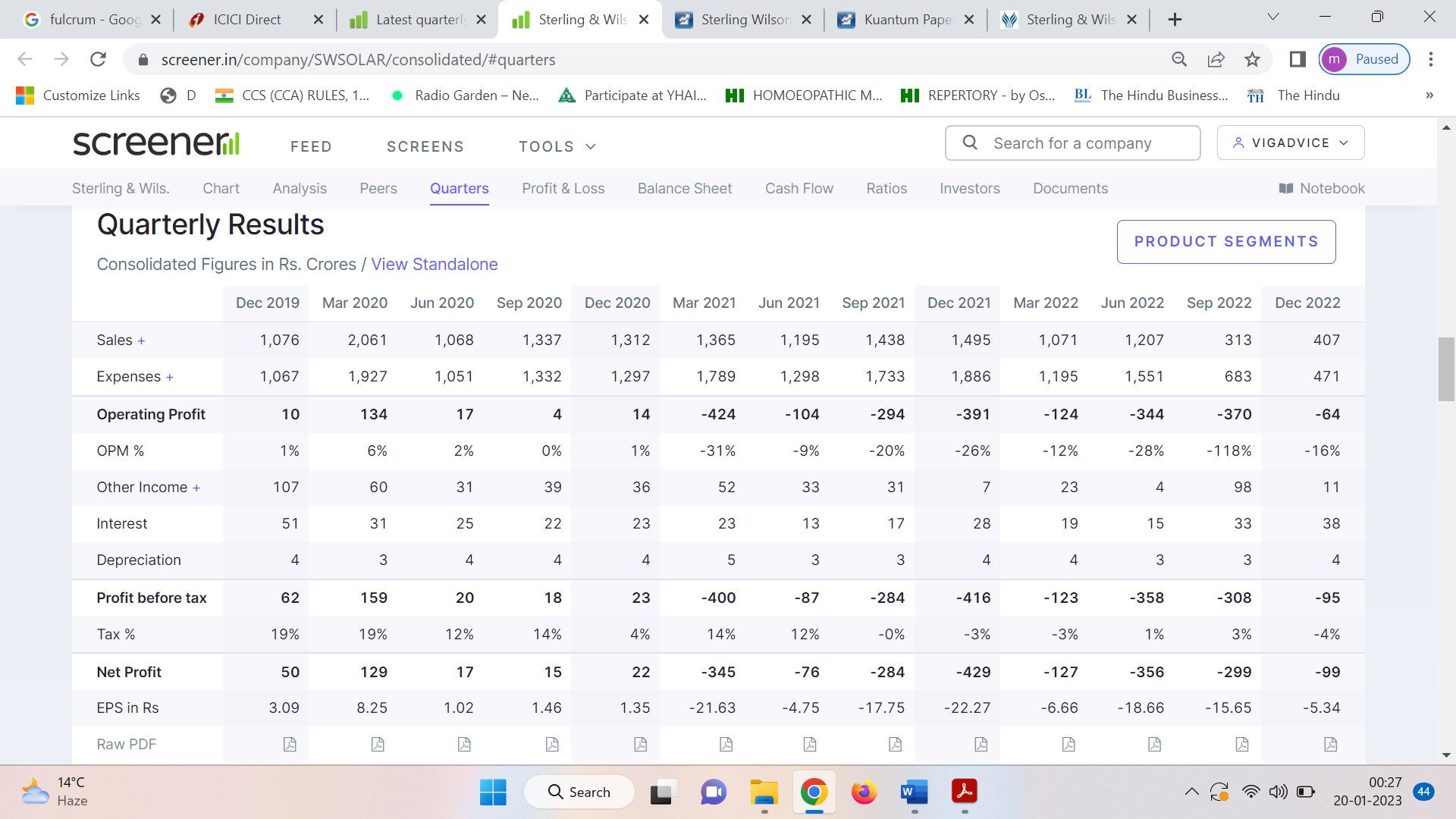

SwSolar has posted another quarter with very weak results. Inspite of continuous comentary from management about improvement in performance, still things are getting worse and I can’t see improvement in any financial parameter. its becoming really frustrating. Few key lowlights from Q2 result.

- Significant and sudden drop in revenue

- Gross margin continue to remain -ve and moving continuously into deep negative trajectory

- Equity infused after RIL joined as promoter has almost disappeared in few quarters.

- Gross borrowing has also increased by almost 1000 cr during the quarter

In addition to the bad quarterly performance, i think company is also trying to act cute. They have released NTPC order win again just after release of results. Many people thought that that was a new order win. Below are few queries, I am unable to unable to understand.

- Does the order book of ~2600 cr includes NTPC order or that will be accounted in Q3

- Why company exited orders worth ~900 cr in Q2

- What is the reason for suden increase in gross borrowing.

Would request others to comment who are following the company or sector closely.

This is an old article. May be some of the observations are still relevant.

Sterling Wilson Renewables Energy Q2: Is it really a disaster?Sterling Wilson Renewables Energy Q2: Is it really a disaster?

@rajbiluve @Waynef225 Hi sirs- you used to follow this company very closely. What’s your current views on this ?

Can see that borrowings have gone up so much, OP is higely negative . Any insights would be helpful. Thanks in advance.

Yet again very bad quarterly results reported by SWS. Inspite of continuous assurance from the management that things will return to normal, we still see losses and net worth has turned negative on consolidated basis. Few key highlights from concall and ppt

- Quarterly P&L: impacted by the provisions of around 270+cr due to the cost overruns, quality issue and desired output challenges on projects related to legacy book. Also, there was significantly low execution during the quarter. Inspite of management guidance of Gross margin positive for last few quarters, we see huge -ve at GM level. New guidance is to be Ebidta positive from Q2FY24 (only time will tell)

- Order Book: Current order Book stands at ~5000cr incl ~500cr legacy order. Management guidance of cost/revenue neural for legacy order and no more big losses from this legacy book.

- Targetted gross margin 10-11% for remaining orders. This is blended margins incl domestic, international and O&M

- Expected to close Nigerian contract by Q1/Q2FY24. There is delay in the closure due to general election in the country. Expected inflow of 1.5$bn. Execution expected to start from Q4FY24

- Addition to this, there is high visibility of orders totalling 4000cr+ domestic and another 5000cr from international

- RIL order inflows: Still discussions are going on but no clear timelines or roadmap on expected order size and time period.

- Indemnity and other Receivables: around 1200-1300 cr cash is blocked due to indemnity and other receivables. Approx 450-500cr expected to be recovered from Promoters in Sep 2023. Balance to come in following years post crystallization of indemnity after final arbitration. Company will have to bear the interest cost.

- Gross debt stands at 2000+ cr. Borrowing current rate is 9.5%. May go up as repo rate will go up.

Inspite of all the assurance in the past, we continue to see losses and complete errosion of equity infused post stake sales to RIL

There is one report from Nuvama regarding this. Report captures company situation correctly.

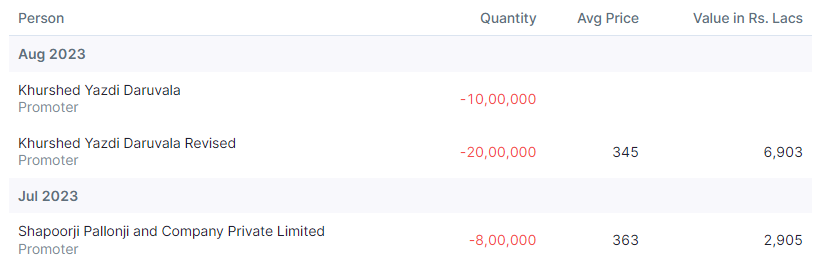

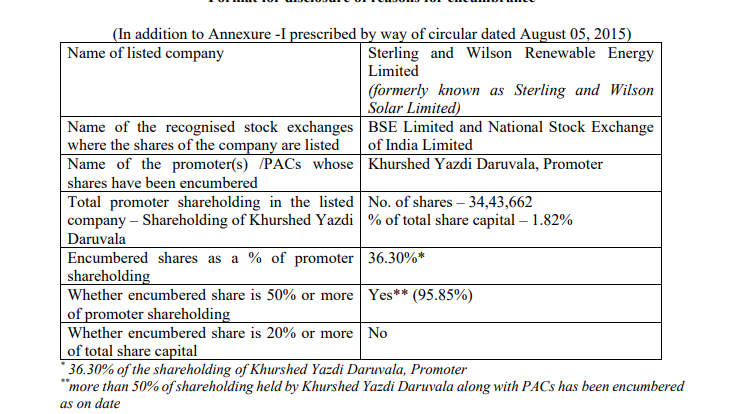

One more concern is pledging & selling of shares from Cyrus family. Their 90% of stake is pledged.

Good thing is company is looking to reduce the debt using QiP as per recent exchange notification.

Note: I’ve invested in Company recently as I think, PAT will follow recently.

The filling mentions that this pledge is create collateral against a loan to be taken by promoter held subsidiary.

This QIP i have a feeling that there are expecting more orders which is why they want to raise capital. Very recently they said they want to eliminate all debt. Would be great if you could share what is the purpose of QIP funds.

But more importantly, I am keenly following orderbook. 4.9K at end of Q1 + this extra 1.5K from NTPC. Eager to see

a. Repayments (to alleviate debt)

b. Nigerian order

c. Reliance Orders

Disc: Invested

rating downgrade to default due to missed payments. Co also cancelled earnings at the last moment.

Great deep dive on the business of Sterling & Wilson Solar by @Tar

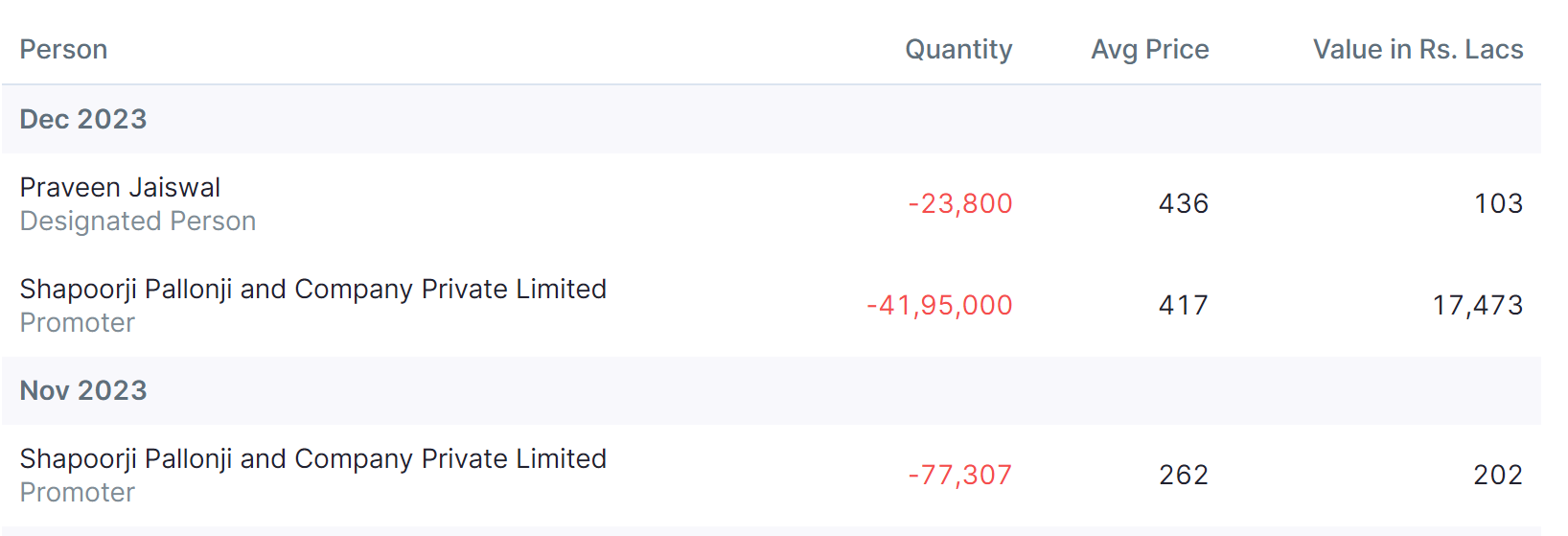

Since they have successfully raised money through QIP debt overhang should go, also promoters are selling continously since there is management change with entry of reliance whose stake has reduced to 32.57 after QIP what are the major triggers for the stock as current order book is around 6835 CR and are the upcoming orders for reliance already priced in the stock and also what should be the margin profile will it be stable around 10% OPM as they have guided that most of the EPC orders are domestic and there is no price risk. On what metrics should be value this EPC business.

Q3FY24 Concall Highlights:

-

Orders Update: The company announced new orders and LOIs totalling approximately INR2,421 crores in Q3 . There was an order inflow of INR3,106 crores announced in the first half, our total order inflow, including LOIs in first few quarters of FY '24 has now touched approximately INR 5,527 crores. With these new orders, our unexecuted order book as on 31st December 2023 has increased to approximately INR8,750 crores with nearly 87% of the order book comprising domestic EPC projects, which are executable over the next 12 to 18 months.

-

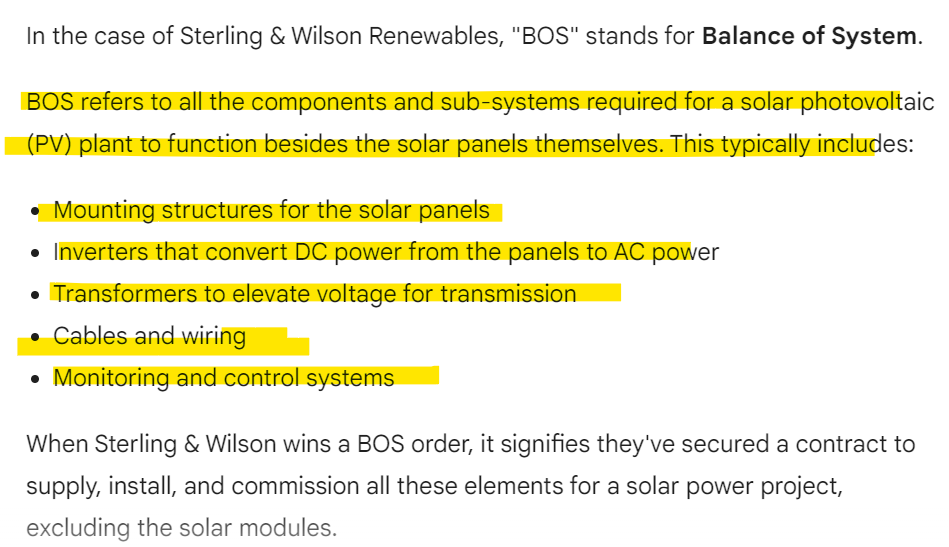

Its First large international EPC order in nearly 3 years is BOS order for a 221- megawatt DC project in Spain. Through this project, SWERL has achieved a key breakthrough in the European solar market: The scope of work includes design, engineering, supply, excluding PV modules and transformer, construction, erection, testing and commissioning. The total contract value, including 3 years operation & maintenance is approximately EUR 112 million. The order was bagged from ENI Plenitude. This is one of the major European utilities giants with a fast-growing presence in the renewable segment.

-

It has won a 220-megawatt DC floating solar project, which also happens to be one of the single-largest floating solar blocks awarded till date in the country. The scope of the project includes modules and EPC work and the project is located in the state of Jharkhand.

-

Through the relationship, it has bagged another project from Sembcorp India subsidiary for a 528-megawatt DC project in Rajasthan.

-

Bidding pipeline in Fy25: expecting almost 40 gigawatt of big pipeline to be bid out in the domestic market alone by FY '25 with the major chunk anticipated to come from PSUs.

-

Opportunities in FY25: In the Middle East alone, They are seeing several gigawatt field projects taking shape across Saudi Arabia, UAE, Oman, et cetera, which should bid out in the next 12 months.We are hopeful of tapping into big opportunities of mega projects subject to them matching our risk profile with cautious approach.

-

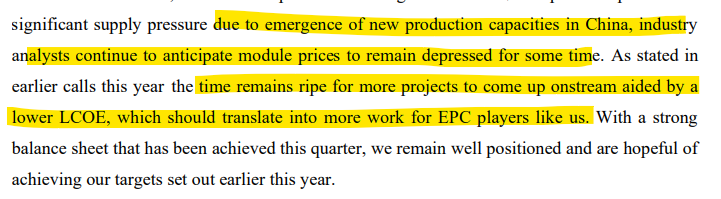

Industry Outlook: There has been a significant decline in the price of modules in the last 12 months, with module price now falling to less than $0.13 per watt peak.

-

Better demand in EPC biz due to low cost of modules:

-

Revenues for Q3: It was lower sequentially due to the execution challenges we faced from tight working capital conditions seen during the course of the Q3.

-

Working Capital improvements due to below 3 reasons:

-

QIP proceeds of approximately INR1,500 crores in December.

-

Promoter indemnity inflows at the end of November.

-

And third, proceeds from a settlement with a vendor which was received in the middle of December.

-

Domestic EPC margins: Margins ins q3 were approximately 9.5% and stand at about 10.5% for 9 months FY '24.

-

O&M segment margins were approximately 15% for this quarter due to certain one-off expenditures incurred post monsoon but it would be 25-30%.

-

Balance Sheet improvement: Cash & cash equivalents of approximately INR550 crores, and our net debt stood at INR27 crores and our net worth at INR982 crores.

-

The total repayments as at date, including those with earmarked fixed deposits is about INR1,800.

-

our projects continue to operate in a negative working capital cycle.

-

Bids in process and in pipeline: There is a significant bid pipeline of 6 gigawatts as we have said that orders remain – order booking remains lumpy based on various quarters.some of the tenders that have been already submitted, which we are awaiting for reverse auction and a lot of bids are yet to be submitted in this quarter, with quite a few we are expecting to conclude within this quarter.

-

So, with respect to the Nigeria project, we are expecting it to get concluded soon, discussions are – at a very high level are still going on, and we expect to get it concluded soon.

-

Capabilities: we are already working on hybrid projects involving batteries. So in various geographies, we are bidding for those projects and in-house capability exists for standalone battery projects or battery projects coupled with solar.

-

Green Hydrogen outlook: major projects are yet to take off the ground, major action, whatever is happening is right now electrolyser manufacturing space. So whenever the substantial projects start hitting the market, so we’ll address that accordingly

-

We can expect traction with respect to standalone battery projects and the pure solar projects, both in Australia and New Zealand markets.

-

Net debt of 377 crores left as it had paid out INR1,600 crores out of 2,178 crores, and we had prepaid another INR125 crores in January.

-

Litigation in process: It relates to an issue on the customer with which we had a surety bond assurance. And what is the situation on that because we could enforce that surety bond. Resolutions in favor would result in cash from them.

-

TAM: So the total bid pipeline we expect in the next 5 quarters is more than 40 gigawatts.

-

Pledge by the principal shareholders, which is essentially, Shapoorji Pallonji and there is a long term loan against it.

-

Revenue for EPC company: So the standard way to recognize revenue for an EPC contract is percentage completion as the project progresses.

-

Timeline to execute the orders: 12-18 months for 8700 crores order.

-

Operating leverage would be in play with increase in revenues.

-

The company is still cashing out somewhere between INR850 crores to INR875 cr. and 400-450 crores is something that could crystallize by this September.

-

All of these projects are negative working capital. They are all cash positive.

-

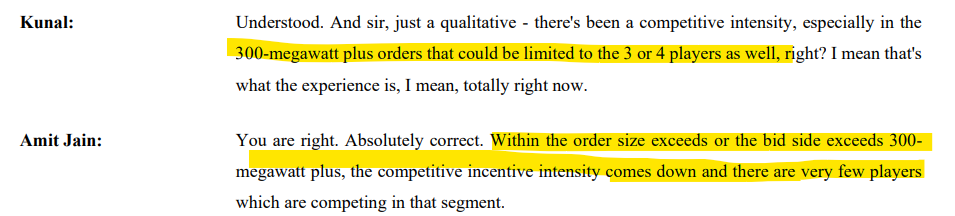

Competitive Intensity over 300 mW+ is very less as there are only 3-4 players in this space and SWSolar and L&T are the ones:

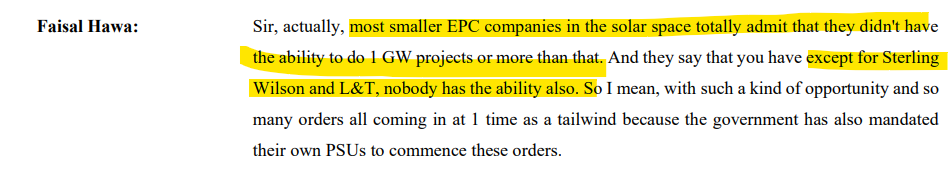

- L&T and SwSolar are the only player to do EPC with 1GW ability:

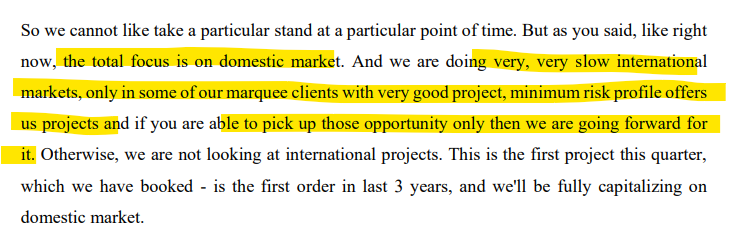

- Being choosy while picking international EPC orders to minimise risk which happened due to covid :

- Bank guarantee compared to project size:

Disclaimer: tracking, only for educational purpose