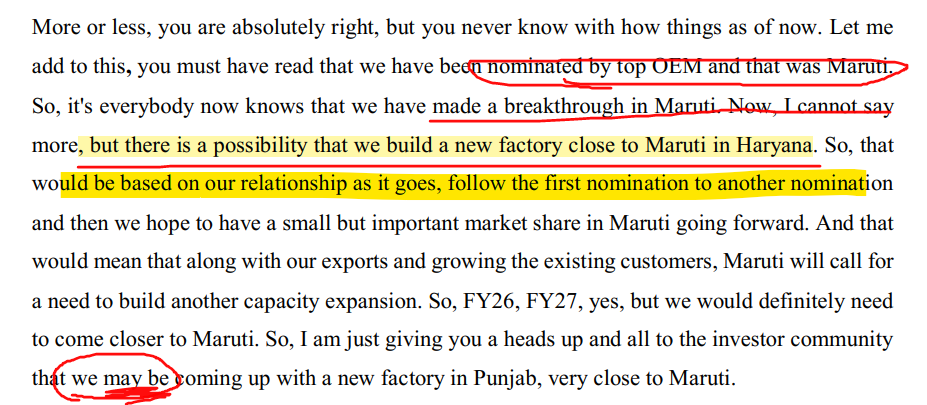

Even I am surprised why they haven’t. It is most probably Maruti Suzuki because they had mentioned that in one of their conference call transcript.

Ohh can be… I thought it has to be one of the newbies like KIA, etc. as they are focusing more on designs rather than the traditional players

Market cap of Wheels India is the reflection of lower return ratios and margins. WIL has fairly diversified into to different segments - Renewable Energy (machining and fabrication), Construction, Railways (bogie). Also, they are late entrants into to alloy wheels (entered in 2021 and COVID impact later years lead to lower utilization). Given the track record of WIL and long association with big OEMs in India, feel like they will catch with SSWL in alloy wheel segment. Risk reward ratio seems to be better in WIL.

2 Likes

How to join the link you gave at bottom?

http://smallcapvaluefind.blogspot.in/

Its showing you need to get invited?

How will they catch up with SSWL? At present Wheels India trades at a higher PE than SSWL.

@Rinkesh_Shah - PE is not the only criteria of valuation. PE for WIL looks inflated as newly started segments from 2021 are not profitable and have not reached optimum capacity utilization. Current margins are around 4.5 to 5%. As per the management, margins should revert to 7% from Q4FY24 onwards. Do calculate what could be the operating profits if margins goes to 7% and see EV/EBITA. Of course, in short term anything can happen. Directionally management doing all right things to improve return ratios.

2 Likes

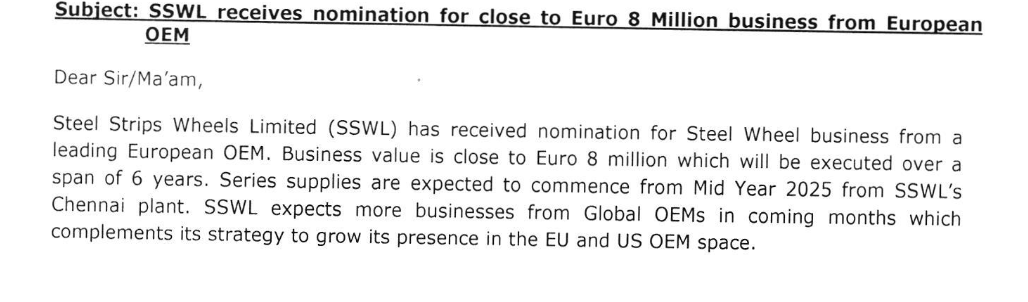

I do not understand what “nomination” mean? Did the company secure the order or something else ?

Amount - 720 Cr INR

2 Likes

It means the same thing as saying that the company has secured an order from a leading European OEM. They have arranged for an earnings call on 27 May 2024 where I believe more details will be revealed. Eagerly waiting for it. They also said they expect more busines from global OEMs.

Disclosure: Invested and biased.

3 Likes

Con-call Highlights - [#SteelStripsWheels]

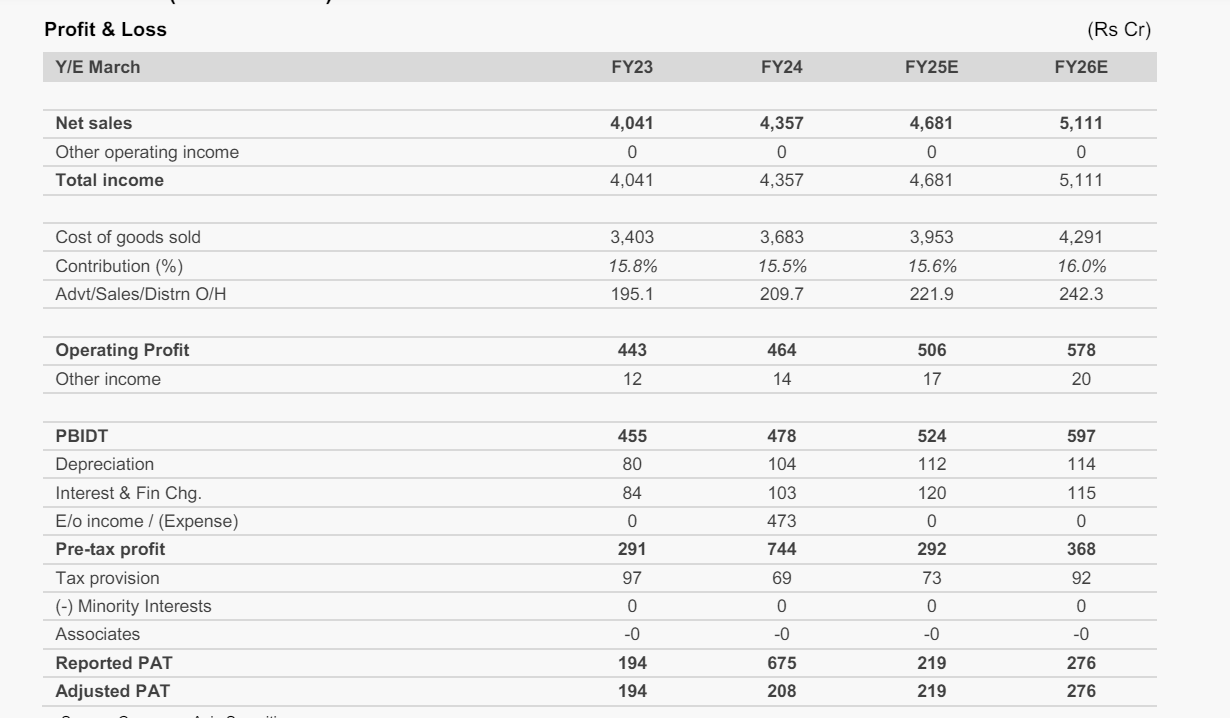

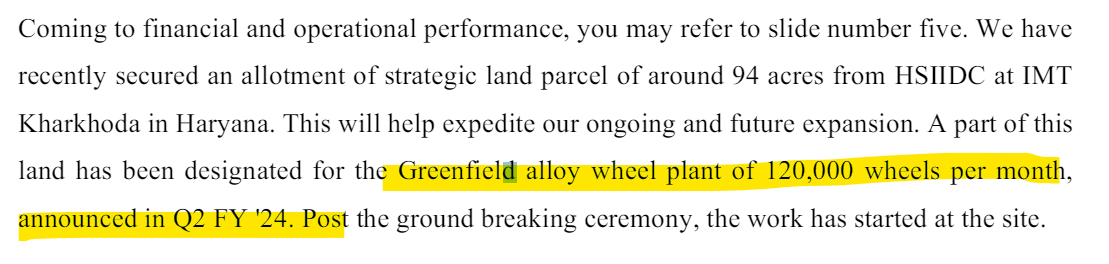

Steel Strips Wheels Limited (SSWL) - Q4 FY24 Earnings Call Key Takeaways for Investors Financial Performance (Q4 FY24 vs. Q4 FY23 & FY24 vs. FY23): * Revenue: Q4 FY24 revenue increased 6.3% YoY to Rs. 1,068.7 Crores. FY24 revenue increased 7.8% YoY to Rs. 4,357.1 Crores. * EBITDA: Q4 FY24 EBITDA increased 2.4% YoY to Rs. 111.1 Crores. FY24 EBITDA increased 5.1% YoY to Rs. 465.2 Crores. * PAT: Q4 FY24 PAT increased 27.6% YoY to Rs. 60.4 Crores. FY24 PAT increased 13.5% YoY to Rs. 219.9 Crores. Operational Performance (FY24): * Achieved highest ever yearly revenues, EBITDA, net profit and sales volume. * Experienced highest ever domestic CV wheel and alloy wheel volumes. * Witnessed traction in alloy wheel exports, with volume crossing 2 lakhs. * Successfully shifted to new tax regime, reducing effective tax rate to 25.17% from 34.94%. * Completed acquisition of AMW Auto Components Ltd. via NCLT order. * Implemented Solar/Hybrid project with expected annual savings of Rs. 9.5 Crores. * Increased steel wheel capacity to ~20.5 million wheels. * Expanding alloy wheel capacity to 4.8 million wheels at Mehsana plant. * Scheduled production start at new brownfield expansion at Jamshedpur plant by June 2024, adding capacity of 0.5 million wheels. * Anticipating revenue from aluminum knuckle production starting from September 2024 onwards. * Secured a nomination from Maruti Suzuki for alloy wheels and in discussions for additional business opportunities. Future Outlook: * Management expects 10% YoY revenue growth in FY25. * Projecting growth in domestic CV and aluminum wheel segments and the two-wheeler industry. * Forecasting growth in the passenger car steel wheels and tractor segments. * Anticipating 10% growth in exports business, with new product lines like off-road vehicle wheels being added. * **Exploring the potential for a new factory near Maruti Suzuki in Haryana based on further business development. Concerns: * Uncertainty surrounding the impact of the election year on CV industry demand. * Competition from Asian manufacturers in export markets. * Potential cost pressures, particularly employee costs rising faster than revenues. Other Points: * Management focused on providing volume-based guidance due to volatility in raw material prices. * Emphasis on shifting sales mix towards higher-margin products like alloy wheels and exports. * Highlighting the importance of operational optimization through automation and robotics to manage costs. * Positive outlook for aluminum knuckles, with revenue expected to more than double in the coming years. * Successfully negotiated price corrections with OEMs in the passenger car steel wheel segment. * Company aims to reduce debt levels primarily through internal accruals and scheduled repayments. Capex for the next year can be funded entirely through accruals.

2 Likes

The name of the OEM has been revealed in today’s concall. It is Maruti Suzuki. Now they’re even planning to set up plant at Manesar near Maruti’s existing plant.

2 Likes

Not sure why it fallen today. i feel it was decent results(excluding one off) and concall also given good insights. with volumes increasing in future and others contributing from sept 2024, revenues are bound to increase and they are also focussing on reducing debts.

what is its fair valuation anyone?

2 Likes

Don’t have any idea of fair valuation but Wheels India it’s closest peer is trading at a PE of 28 while this is trading at a PE of 16. SSWL has better margins and return ratios.

1 Like

Directionally the company might be going in the right direction in the long term but I assume FY25 guidance of 10% revenue growth was a dampener for the markets. I suppose the markets were already expecting it given the correction in the price in the last 2-3 months.

At 10% revenue growth, 11% margin, conservatively depreciation at 148 crs (annualized the 37 cr q4 depreciation, if I take it as 3.4% of revenues as in case of q4 it will be even higher) and interest of 112 crs (q4 int annualized) and tax rate at 25%, the PAT comes out to be 198 crs which is a degrowth of 10% compared to FY24 full year pat at 220 crs. At 15x TTM, I would say this might be fairly valued. The stock is under 30 and 40 weekly EMA, given FY25 is a non event in the view of the markets it can either fall further or consolidate. Around 214 and 194 seems to be strong support levels. These are just my estimates and I can be totally wrong.

Disc: Hold a tracking position which I might be looking to exit.

11 Likes

I think the main kicker would be margins as they have taken price hikes in existing steel wheel business. Also, key negative in the commentary was lower than expected growth outlook in alloy penetration in the like of Hyundai. Uno Minda has shown good growth in alloy wheels mainly due their presence in Maruti where premium mix has increased substantially but Hyundai already had high mix of premium (FY24 over FY23 mix)

Stock is fairly valued and I think the optionality comes from knuckle business and higher mix of alloy in export. However, high debt level along with aggressive capex remains a risk in medium term.

5 Likes

Debt levels are comfortable and they can service it with surplus cash flows and internal accruals which they have already said in their earnings call. I still feel it is undervalued considering the valuation of Wheels India. Holding it.

Some keys variables to track -

-

Management guides to improve the EBIDTA per wheel for its steel wheels (bread and butter business as it is called). EBIDTA per steel wheel was Rs 253 per wheel similar to previous year. Steel wheels is 72% of full FY24 revenue. The expectation is see positive side correction on 72% of the business as per the management.

-

Knuckles revenue shall doube from 35 cr to 70 cr and then 4x. First mover in Knuckles business developed in collaboration with Mahindra. Also, it is an import substitution play.

-

Co may consider to do a greenfield expansion very to the Maruti plant based on how the relationship with Maruti goes. (REMEMBER- “may consider”)

-

Uno minda is making a greenfield investment in alloy wheels. 1.44 Million capacity per year. Below image from UNO Minda,

-

Guidance of 4800 Rev for FY25 with 0% growth in CV and no revenue contribution from AWM

4 Likes

Are they losing market share in truck segment. ? because production and wholesale yoy seems to be flat to positive in truck and PV as well/

There is a slowdown in truck segment. They have already said this in their earnings call. Overall CV segment won’t do well this year. And after shocking election results share price also has taken a beating.

1 Like

Does anyone know why the promoter is steadily selling?