Hi,

Would like to know views about Steel Strips and Wheels Limited. Why it is traded at 11 PE, Market Capitalization is 50% of Annual sales when other 2 peers trading, Wheels India @42 PE, Enkai Wheels @57 PE accordingly.

Some Inputs …

Stock Price - 370,

Trading PE 11 Vs Industry PE 45,

EPS is increasing with margin expansion: 34 rs

2015H1 earnings 18 crores Vs 2016H1 earnings 27 crores

First Interim dividend declaration,

Higher Operating margins than peers New allotment @640 rs, premium of 270 rs from current market price.

Tata Steel, Sumitomo(Japan), GSSC (South Korea) holds nearly 17% stake in this company.

Promoter regular purchase from Open Market

P/E ratio should always be seen in conjunction with the debt of the company. Half yearly balance sheet of company mention

Long Term Debt = 261 cr

Short Term Debt = 262 cr

Also company has negative working capital

Current Assets = 481 cr

Current Liability = 485 cr

I am also surprised with the Kalink willingness to subscribe at Rs. 640/- per share because they can easily acquire 2 lac shares from open market at much lower price. The amount of their investment is very small approx $2 million. It is like a seed amount for a start-up.

@Bhavya,

Thanks for sharing an interesting Idea.

I googled about Kalink and seems to be a good company . Further Kalink Co has manufacturing facilities at South Korea and China with a total manufacturing capacity of 4.5 million wheel rims per annum and is supplying to major original equipment manufacturers (OEMs) such as Volkswagen, Nissan and Chrysler, etc.

@Gauravx,

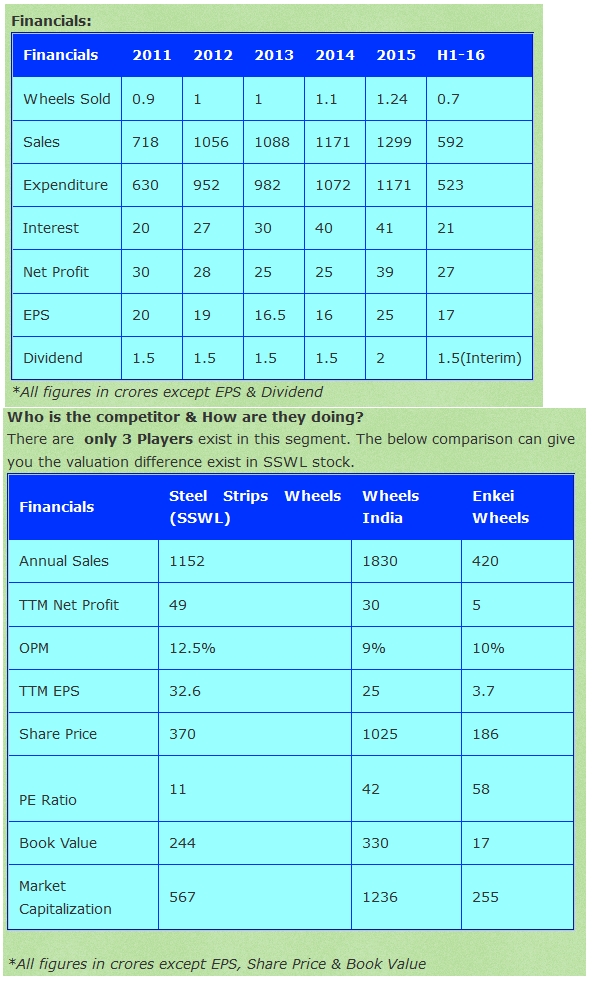

Here is the exact comparison between the 3 listed players (Fig in Crores).

here are some links https://www.kalink.co.kr

for the Korean maker

Here is the old news item about alloy wheel tie up with Kalink and the investment at 640

PS - got a tracking position today at 384. Debt to Equity certainly scared me and I was fearful of another Ahmednagar forging type story (now, Metalyst )…what made me change my mind is the tie up and improving margin…if u take out the outerlayer of march’14 out, the rest of the net profit looks bearable, if not making you fall out of the chair. looking for no miracles here and hence expectations are low

Kalnik and SSWL has joined hands to start a plant in Gujarat for manufacturing Alloy wheels - where Kalnik already has mastery in making and SSWL has market knowledge. It has to be an agreement between both the parties to take a stake in the company at 640/- and have a decision taking authority at the board level (for Kalnik). If Kalnik goes and get the shares from the open market (simply it can get in next 2 days - daily volume of 2lac shares), it would not get the control required for doing business. I think its a green flag.

The worry to me is the ROE and ROCE - ROE is around 11.94% and ROCE is much less around 7.50%.

If we conduct du pont analysis - financial leverage is high enough, NP margins are higher than the peers or almost same, the problem seems in the Asset turnover. Sales are not growing at good rate. Company claims to have bagged great orders recently, but the same is not getting reflected in its performance. Sales of other peers have grown decently. Any clue/hint here.

What about the mgmt - I feel mgmt is decent enough - TATA steel and other global players are its partners. But, need to dig more into integrity of promoters. Anyone having inputs here?

Management quality is probably worth looking if you are looking at a structural growth story…this looks like one of those mispriced one and has to be treated accordingly…

PS - disclosure given above

SSWL reports good performance compared to both peers on EPS/ PE/ PEG/ OPM/ NPM fronts.

Sales are big concern for me. Sales for the peers have grown - for wheels at 4.59% and Enkei at 25% last year. What is the problem in SSWL? Topline growth has to be there for long term growth. ROE and ROCE are also somewhat a concern (almost similar to the peers).

The recent orders bagged by the company can really change the outlook - but am I correct on this?

As per my understanding, SSWL is big in OEM sales and very less presence in after market, hence sales increase is less, almost in tandem with automobile sales. However, Enkei is big time into after market sales and hence higher sales. Also, scope of margin expansion will improve for SSWL if they establish themselves into alloys. It needs to be seen how they venture into alloys sales, through OE sales or focusing on after market.

Disc: Not invested.

Thanks lot Vikas. Your logic might be correct. So its good to hear that the company has taken steps to enter into after market segment this year. Hope to see some improvements this quarter.

W.r.t Management quality, considering Tatas, Sumitomo on board. Previously in 2012, when the share price trading @200, management allotted themselves @300rs. If you see the recent BSE disclosures, they are buying more from the open market even @370 levels. Similarly they are regular in informing the exchange about monthly sales etc…With the above points i am of the view that management is trustworthy.

W.r.t sales turnover SSWL stands 1.4 Vs Wheels India @1.8, but SSWL is having higher margins than others. I feel the current valuation gap with peers will be covered going forward.

Things are clearly changing for the company if you go by their recent order wins.

The Egypt order win is a new geological entry for them and as they claimed, it is going to be repetitive moving forward.With in a week they bagged one more order from Egypt, this gives me the trust that management are dependable. These order wins/ new entry to export markets should improve the Sales turnover giong forward.

Recently i am paying closer attention to the companies where promoter buying is happening from open market as a big positive move. To share specific details , Tera Software used to trade around 35rs, promoter purchased huge quantity from open market, After sometime they got 320cr order from Andhra Pradesh govt, thereafter the journey halted only @100 levels now ( My Tera Soft example should be taken in promoter open market purchase context only).

Which auto segment (Car,Two wheeler, LCV ,HCV) does steel strips caters to and what about competitors?

this will help in understanding the valuation gap?

What kind of RM price increase/Decreases are passed on to the customer?

Thanks krishna. But i guess these orders are of small quantities - which will add to revenues few 50 crores only. Now this looks too small looking at the topline of 1100cr +. Correct me if I am wrong.

Also, company has entered the after market sector. Has it entered into after market sector in india as well? Since they have bagged orders for after market from Korea and other foreign countries and not yet from India.

Is it true that there are only these 3 companies operating in wheels sector?

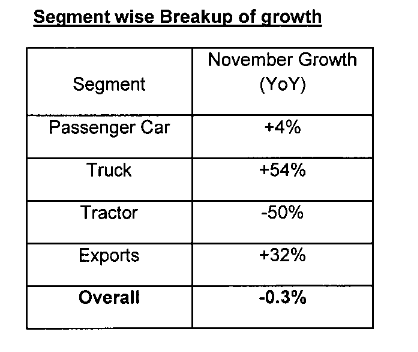

The level of disclosure by the company is excellent. Below find table from sales figures for the month of November (source: BSE website)

Tractor rim sales is negative. My interpretation is this may not improve until monsoon. Also it is not know how next monsoon will pan out. Therefore company growth may be questionable for next one year at least. Other interpretations invited.

@Gaurav_Agarwal,

Yes the the management seems to be keeping things simple.

My way of interpretation is, Management offsetting the local de-growth in Tractor segment with good growth in export aftermarket of same segment. Hence the export growth is 32% & 44% in the last 2 months. Clearly this is company’s marketing effort because if it happens in only one month it may be one time opportunity, but it is showing the growth month by month.

Few more things to notice

Promoter bought 1.2 Lakh shares from open market in the last 1 month, clearly management know something, which we don’t know yet.

First Interim dividend declaration

Company’s Risk Framework policy is very good goes by AR15.

Disclosure: Understanding the business before putting the investment

For a 1200 cr top line firm, this order is not much …about 17cr an year but locks in a 85 cr sale, over 5 years…all the same, Kubota is a world renowned name in tractors. The export bucket seems to be trickling in. I need to get more conviction before going in for the plunge and I am looking for some more pointers, as this thread develops…

PS - got a tracking position, couple of days ago.