SSWL is a leader in designing & manufacturing Automotive wheels – both Steel & Alloy Wheels category

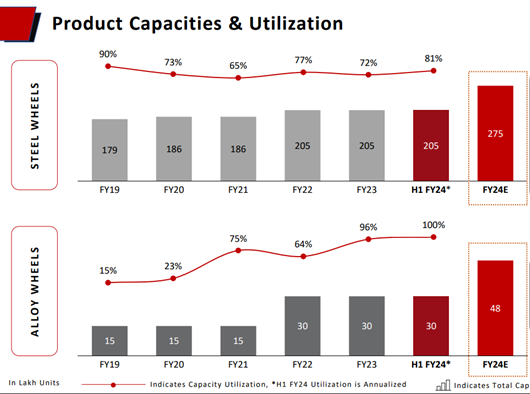

By FY24 end, 70 Lakhs Steel Wheel capacity to be added in phased manner, post-acquisition of AMW Auto Components Limited

Alloy Wheels Capacity to be expanded by 60% i.e. 18 lakh Wheels at Mehsana Plant, Gujarat

Exploring various avenues to foray into EV Segment

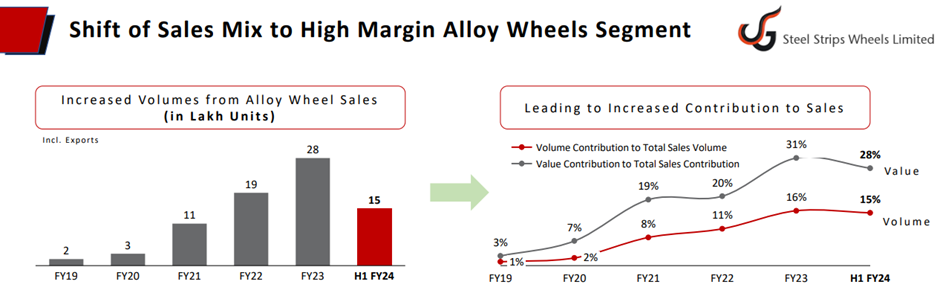

Sales Mix Shift Shift of Sales Mix towards High Margin Accretive Segments – Alloy Wheel & Exports

Steel Wheel Market to grow at 8% p.a. whereas Alloy Wheel Market to grow at 12% p.a. over next 5 years

Margin differential between alloy wheels and steel wheels is approximately 700 basis points

Strengthening Balance Sheet thereby Improving Return on Capital Employed & Return on Equity

INR190 crores spent on capex in H1 FY24

Total capex for FY24 expected to be around INR320 crores

NCLT order for acquisition of AMW Auto Components Limited for INR138 crores

Total expected capex for AMW acquisition is INR158 crores

AMW plant in Bhuj expected to become commercially operational by Q1 FY25

Expanding capacity for Steering knuckles with a total capex of INR200 crores

Revenue potential of INR220-250 crores By July FY24

Revenue guidance for FY24 is INR4,500-4,700 crores