Check production numbers

Trucks production is not down to the tune at which their volumes is declining

1 Like

Promoter has only sold around 1.7% in last one year. That cannot be called as steadily selling. And they might have sold to make their shares pledge free and for working capital requirements or may be some other reasons.

2 Likes

Prepayment of debt is also a good sign.

2 Likes

I checked FCF of this company is negative in this year but was positive in previous years

1 Like

Notes from Investor Presentation Q1fy25

Company Overview

• Operational Wheel Capacity 24 Mn

• steel wheel - 20Mn Alloy wheel - 3.6Mn

Strategic Partnerships

- TATA Steel Limited, India (6.9 % Stake in Steel Strips Wheels Limited)

• Tata Steel Limited (through its then wholly Kalimati owned subsidiary Company namely Investment Company Ltd, which has now merged with Tata Steel Ltd) had entered into a Strategic Alliance Agreement in January 2008 with SSWL.

• Through this relationship, Tata Steel supports us with more flexibility in areas such as supply chain management, enjoying priorities and stronger support for new grade developments, etc. - Nippon Steel & Sumitomo Metal Corporation, Japan (5.4 % Stake in Steel Strips Wheels Limited)

•Sumitomo Metal Industries Limited, merged with Nippon Steel Corp and now known as Nippon Steel & Sumitomo Metal Corporation (NSSMC), has entered into a Strategic Alliance Agreement in December 2010.

• This relationship helps in bringing international expertise in steel quality and newer technology exploration.

•Sumitomo Group, which has 400 years of manufacturing history, founded Sumitomo Metals in 1897 and it is one of the world’s leading steelmakers.

Products - Steel Wheels Rs. 732 I ncl. Exports crores (~ 7 1 %) ( Q1 FY2 5 Revenues)

- Alloy Wheels Rs. 294 I ncl. Exports crores (~ 2 9 %) ( Q1 FY2 5 Revenues)

Product Capacities & Utilization

Steel wheels

•Phased addition of 70 lakh steel wheel operational capacity

•Resolution plan successfully implemented in January 2024 by payment of ~Rs 138.15 Crs. (Rs. 5 Crs. Equity and Rs 133.15 Crs. Inter Corporate Loan)

Alloy Wheels

•Alloy Wheels Capacity to be expanded by 33% i.e. 12 Lakh Wheels to 48 Lakh Wheels in a phased manner at Mehsana Plant, Gujarat

Plants

•Dappar, Punjab - capacity10.8Mn :- Catering to PV, MUV, Tractor & OTR

•Chennai, Tamil Nadu - 7.5Mn - catering to Pv & CV

•Jamshedpur, Jharkhand - 2.2Mn - catering to HCV / LCV

•Bhuj Gujarat - 7 - catering to Hcv , tractor, PV

•Mehsana , Gujarat - 3.6 Mn - catering to PV

•sareikela, Jharkhand - Backward Integrated Plant for Steel Wheels

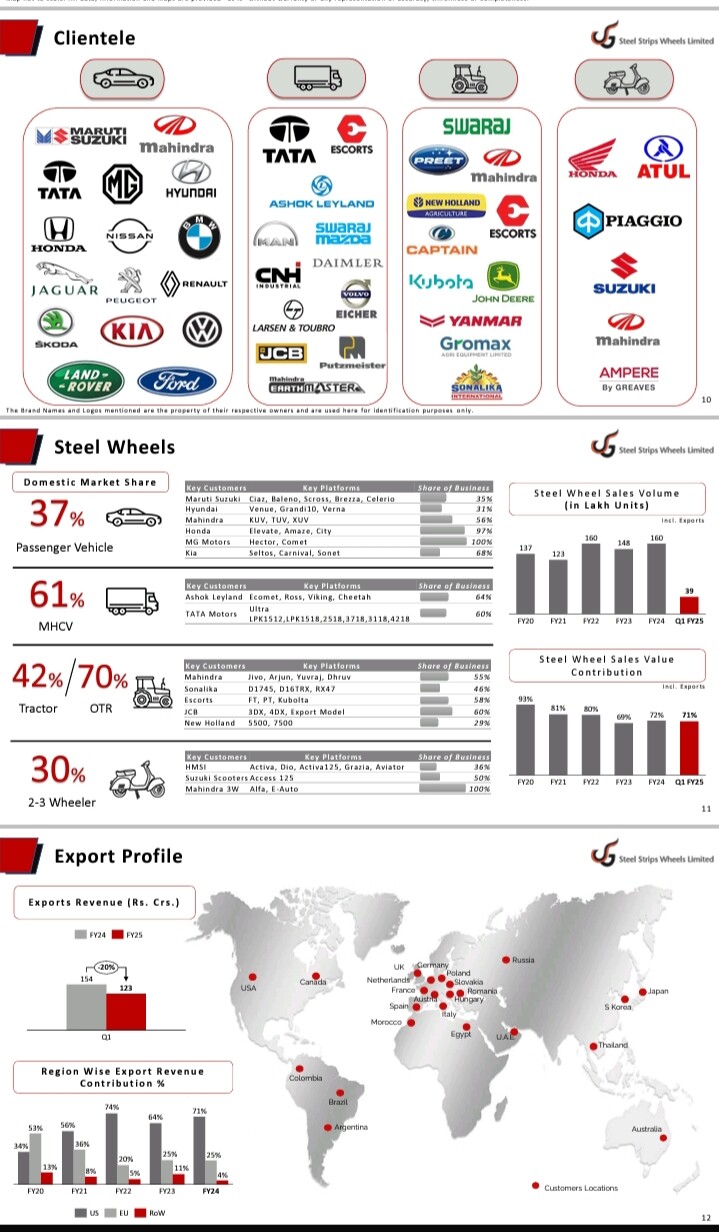

Clientele, Steel wheels Breakup And Export profile

Growth Drivers

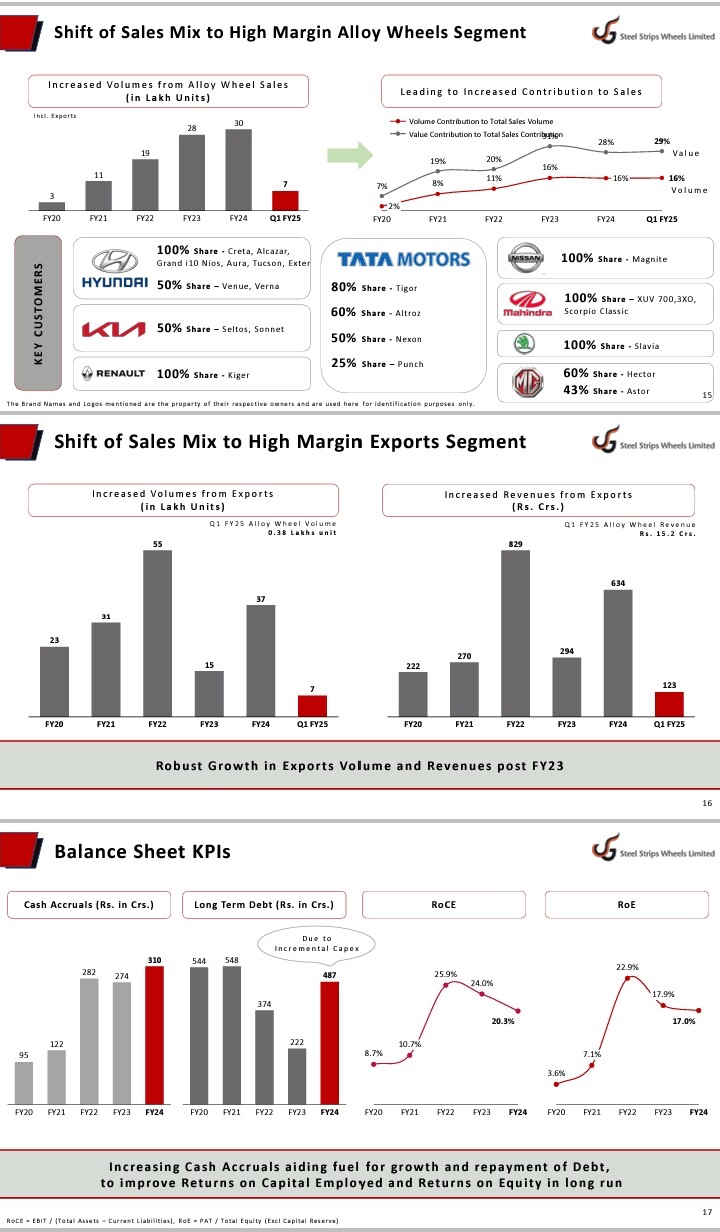

•Sales Mix Shift Shift of Sales Mix towards High Margin Accretive Segments - Alloy Wheel & Export

•Development of Robotic Automated Operation process for Operating Cost Rationalization

•Exploring various avenues to foray into EV Segment

•Steel Wheel Market to grow at 8% p.a. whereas Alloy Wheel Market to grow at 12% p.a. over next 5 years

•Strengthening Balance Sheet thereby Improving Return on Capital Employed & Return on Equity

Shift of sales Mix And Balance Sheet KPIs

Increasing Cash Accruals aiding fuel for growth and repayment of Debt, to improve Returns on Capital Employed and Returns on Equity in long run

Q1Fy25 financials

Disc- initiated a tracking position , not a recommendation to buy or sell

3 Likes

Steel Strip Wheels -

Q1 FY 25 results and concall highlights -

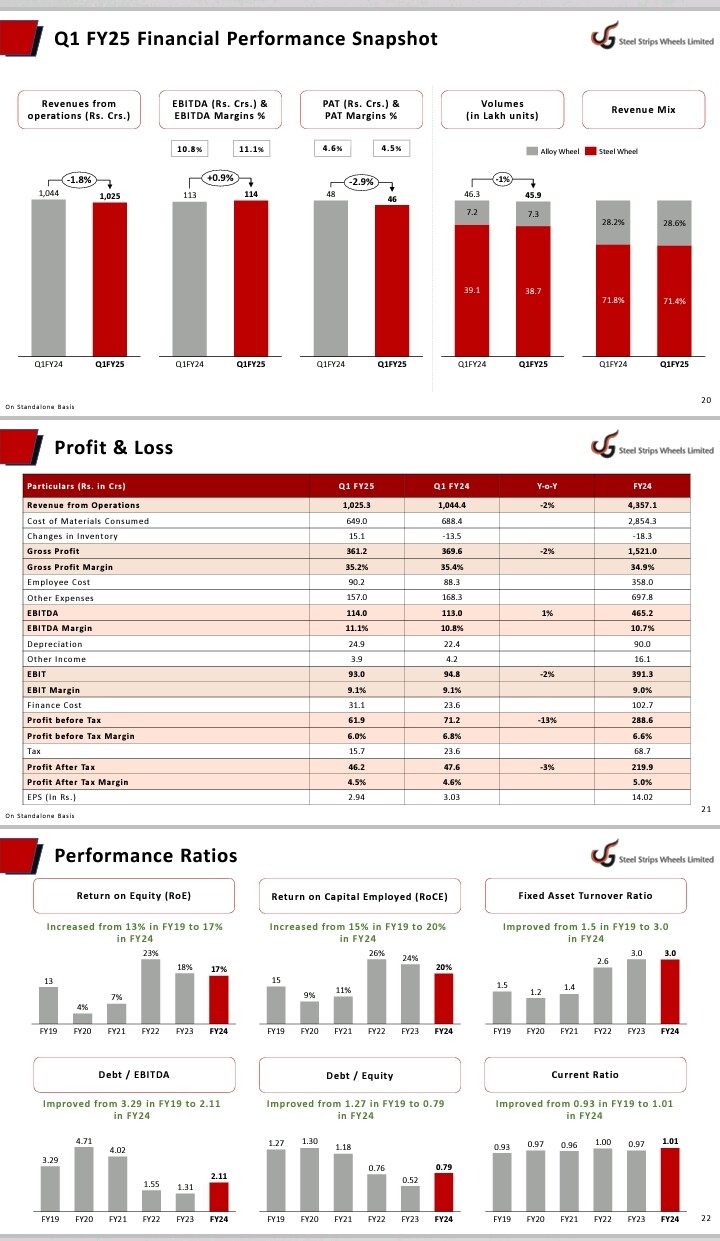

Revenues - 1025 vs 1044 cr

EBITDA - 113 vs 113 cr, flat

PAT - 46 vs 47 cr ( due reduction in interest costs, despite higher depreciation and interest costs )

Gross Debt @ 965 vs 1050 cr on 31 Mar - a reduction of 85 cr

Revenue breakup -

Steel wheels - 732 cr @ 71 pc of sales. Sold 3.87 million steel wheels in Q1 ( vs 160 million steel wheels in FY 24 )

Alloy wheels - 294 cr @ 29 pc of sales. Sold 0.73 million alloy wheels in Q1 ( vs 30 million alloy wheels in FY 24 )

Current capacity -

Steel wheels - 20 million - expected to go upto 27 million by year end

Alloy wheels - 3.6 million - expected to go to 4.8 million by year end

Manufacturing footprint -

Dapper - Punjab - Steel Wheels - 10.8 million

Chennai - TN - Steel Wheels - 7.5 million

Jamshedpur - JH - Steel Wheels - 2.2 million

Bhuj - Gujarat - Steel Wheels ( AMW’s acquired capacity ) - projected capacity of 7 million

Mehsana - Gujarat - Alloy Wheels - 3.8 million

Company’s mkt share ( segment wise ) -

PVs - 37 pc - key clients - Maruti Suzuki, Hyundai, Mahindra, Honda, MG, Kia

MHCV - 61 pc - key clients - Ashok Leyland, TATA

Tractors - 42 pc, OTR - 70 pc, key clients - Mahindra, Sonalika, Escorts, JCB, New Holland

2-3 Wheelers - 30 pc - key clients - Honda, Suzuki, Mahindra - 3Ws

Q1 EBITDA / Wheel stood @ Rs 257 vs Rs 253 YoY

Q1 export sales @ 123 vs 154 cr YoY ( out of which, alloy wheel exports stood @ 15 cr )

Export mkts showed weakness in Q1 due supply chain disruptions and rising global inflation. Despite this, company is sticking to its export revenue guidance of 675 to 700 cr and they are confident of achieving the same

Expecting a 6-7 pc growth in steel wheels business in the domestic mkt for FY 25

In 2 wheelers, company is expecting 15-17 pc growth from the EV segment

In the tractors business, growth should hit double digits due long term supply arrangements with some prominent customers

Company entered a new line of business in last FY - that of aluminium knuckles. Expect additional revenues to start flowing in wef Q3 this yr. These are used primarily in SUVs to improve the vehicles manoeuvrability

Company is comfortable with their PV mkt share of 36-38 pc. They ll not chase mkt share if it comes at lower margins. They r ready to forego the lower margin business

Export mkts are generally slow in Q1. They generally pick up wef Q2. Same should happen this yr too

Company feels the aluminium / alloy knuckles will slowly replace steel knuckles like the alloy wheels are replacing steel wheels. This line of business should see good growth for next 4-5 yrs

Aluminium Knuckles is an import substitution product. Company is is discussion with 02 big customers ( to which the company already supplies alloy wheels ). Company is confident of good business prospects in this line of business

As the auto industry moves towards more premium vehicles, wheels mkt should move towards 45-50 pc penetration of alloy wheels vs 35-40 pc penetration at present. This should be a nice tail wind

Aluminium knuckles should be a better EBITDA margin business. This yr, they should be able to do a business of 30 cr or so in this segment. Next FY, expecting this to be a 60 cr kind of business with commencement of contribution to the bottomline

For full year, finance cost should be around 105 - 110 cr due steady debt reduction as was seen in Q1. ( interest cost in Q1 was 31 cr )

Over long term - India as a geography should gain mkt share for exports to EU+US ( vs China ). This should be the long term trend going forward

The next leg of growth for the company should come from export markets. They intend to take their business from current 700 cr / yr to 1000 cr / yr to 2000 cr / yr from the exports mkts ( over next 3-4 yrs ). And a lot of this will come from the alloy wheels, where the margins are better

Also, the they intend to take their Knuckles business to > 500 cr/yr in the next 5 odd yrs

Capex guidance for this yr @ 200-220 cr for alloy wheels + aluminium knuckles. From next yr onwards, Capex intensity should cool off. Also, 1050 cr of Debt on 31 Mar 24 was company’s peak debt. It should only keep reducing from here on

Disc: holding, biased, not SEBI registered, not a buy/sell recommendation

5 Likes

So what I can understand, Alloy wheels will be a key trigger for generating higher margins (also knuckles). Mgmnt has clearly stated they’re not chasing lower margin business, ideally i would expect this suggests they’re not looking to increase market share in various segments, instead would be looking to ramp up exports, which would be of alloy wheels more than that of steel wheels.

Alloy wheels would contribute approximately 210-220 cr EBITDA.

And with 85% utilization of 27mn capacity Steel wheels can do 450cr EBITDA. This would get us to Roce north of 25%.

But then what next? As this might have been already discounted into price, and if growth is coming in the industry it may not match with the reinvestment aspirations of the company.

Relatively pricing is cheap, absolute maybe not.

2 Likes

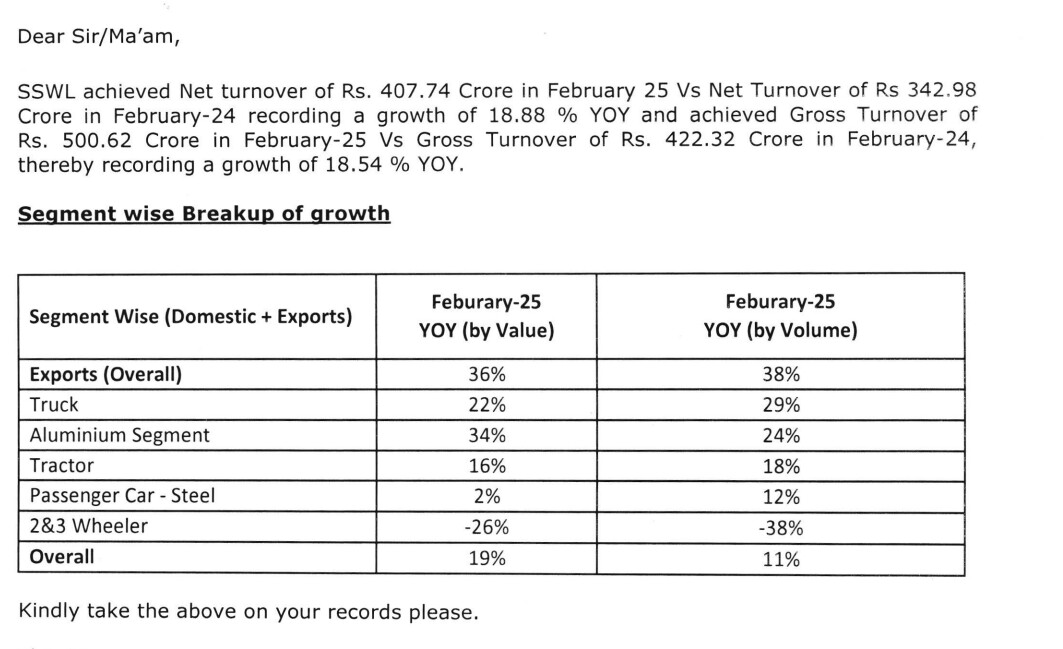

SSWL Clocked Highest Ever Monthly Sates in January 25 (up by 8% YoY)

Highest Ever Monthly Sales in Aluminum segment (up by 26% YOY by Value;

Tractor Segment Monthly Sales (up by 31% YOY by Value)

4 Likes

This stock looks really undervalued to me with Capex increase of 32% in Steel wheel & 17% in Alloy wheel by end of FY 25 and Asset turn of 1.3x, and utilisation of 75% - 80%, it looks a straight upside potential of ~30-35% growth in PAT just based on capacity increase.

I am not sure why it is not factored in the prices as yet, trading at crazy valuation of PE of 14

Am i missing something here or some gap in understanding the business?

3 Likes

As per the management there’s no tariff on wheels.

5fe70cbf-3810-49a6-af41-1345e7aed294.pdf (658.0 KB)

3 Likes

This is strange. What was the need of this clarification? Nobody asked for it.

2 Likes

May be market will reward it only after delivering real EPS growth as in past its operating profit has been flat and EPS growth came from other income.

The real EPS growth will be reflected from March 2025 quarter onwards. Their aluminium knuckles business have already started generating revenue in March 2025 quarter. Moreover, they are likely to report their highest ever quarterly revenue. The share of high margin alloy wheel segment in total sales has also increased. Also, aluminium knuckles segment margins is in high teens. CV segment is also gaining traction. Only concern is slowdown in passenger vehicles sales.

3 Likes