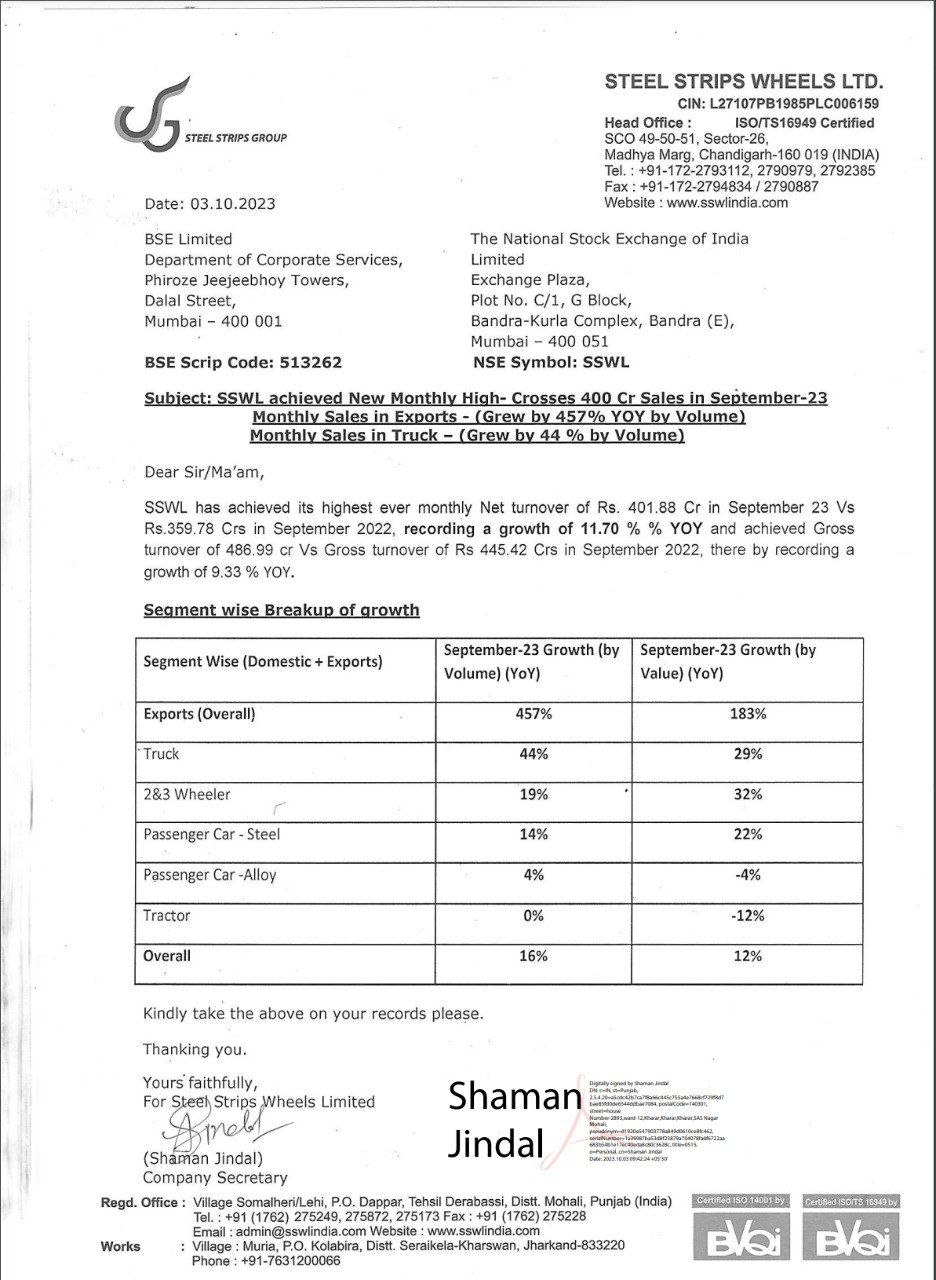

SSWL reported highest ever monthly turnover Rs.401.88 sales in the month of September 2023.

Exports grew 457%

SSWL reported highest ever monthly turnover Rs.401.88 sales in the month of September 2023.

Exports grew 457%

Recently started following the company, no investment as of today. The company looks impressive with high growth potential, increase in margins, operating efficiencies, and good market standing. However, there are few questions still troubling me here

The market share figures in each segment are

PV - 50%

MHCV - 53%

Tractor - 44%

OTR - 70%

These numbers have remained constant across quarters for 2-3 years. In every ppt, there is almost zero deviation from the numbers. I find it very strange. There has not even been a 1% movement in any category for years. Their client-specific business share exactly the same across quarters as well.

For 4-5 years, investors were expecting margin improvement from alloy wheels and exports but not much improvement in numbers here. Covid and inflation might take some blame here though.

The negligible presence of FII/DIIs for a 4000 Cr. company raises some concerns.

Hoping to get some answers here

@Prankush_Bansal Your observation for the market share figures are quite right and I also found out that that the company has used the same figures in 2016 investors presentation which sounds very strange and makes us question their lack of due dilligence about the factual inaccuracies present.Although we can comprehend that way that the managment either might be using rounded of estimated figures.

They have changed the Market share data for passenger vehicles in OCT 2023 IP.

Who took their 5% market share?

Might be wheels india or some other import player beacuse they are not focusing much on steel wheels but more on alloy wheels to grow that category with high margins

This is partly due to pledged equity, nearly 5% is still pledged. Institutional investors have this as one of the primary health checks.

Yup, valid reason. If the management keeps up with it’s promise of zero pledged shares soon, we might see an inflow of institutional investors then

Some notes from concall dated 10/30:

Capex:

AMW Autotech Acqusition:

Steering Knuckles

Exports:

Debt Status:

Misc:

Overall, this 7 Mil capacity at a very reasonable valuation (~150 Crs) by way of AMW acquisition is very positive for the company - more so when they are already hitting upper end of capacity utilization on existing sites. AMW may also be margin accretive being into Heavy agri/truck segment.

Alloy wheels expansion by 60% is another positive unfolding well. Is a brownfield with ~3x asset turn with better margin business. There is definite market traction and they are able to garner share both domestic and in export markets.

On the other hand, this call has moderated all expectations from new steering Knuckles foray - at least in medium term. Though there is synergy with current product basket however an 1.2x - 1.3x asset turn venture with say 12% - 13% EBIDTA margin funded by debt wont leave much money on table. Even the scale-up is not swift enough to compensate for - phase 1 scale-up itself is going to take next 1.5 - 2.0 years. May be little early to call this as small avoidable distraction?

Thanks,

Tarun

Disc: Invested

How much will the depreciation be qtrly after they inccur the whole capex?

Thanks for sharing Tarun.

One additional detail which was conveyed by the management during the concall was that the effective tax rate of the company will come down from current 33℅ odd to 25℅ in FY25. This is expected to have a positive impact on the EPS from FY25 onwards.

To put it in nos -Q2FY24 EPS would have translated to Rs. 3.80 from current Rs. 3.34 due to such reduction in tax rate - resulting into an EPS growth of 13℅

Thanks,

Souvik

Disc: Invested

Steel Strip wheels Q2 highlights -

Total plants - 04

Current capacity -

Steel wheels - 20 million +, by end of FY 24 - another 7 million wheel capacity would be added

Alloy wheels - 3 million + , by end of FY 24 - another 1.8 million capacity would be added

Employees - 7000 +

Last 5 yr revenue, PAT CAGR @ 15, 19 pc

Tata Steel holds 6.9 pc stake in the company

Nippon Steel holds 5.5 pc stake in the company

Domestic Mkt share ( steel wheels ) -

45 pc in PVs

53 pc in MHCVs

44 pc in tractors, 70 pc in OTR

30 pc in 2-3 wheelers

Sale contribution from steel wheels - 72 pc

Sale contribution from alloy wheels - 28 pc ( it was 3 pc in FY 19 )

Q2 financial outcomes -

Sales - 1134 vs 1081 cr

EBITDA - 124 vs 117 cr

PAT - 52 vs 55 cr

Volumes - 5.1 million vs 4.7 million

Cash and cash equivalents @ 44 cr

Capex spend for H1 FY 24 @ 190 cr. For full FY 24, expect capex spends @ 320 cr

Out of this, 190 cr are being spent on Capex of Alloy wheels capacity

Intensity of capex to reduce going fwd into FY 25,26

H1 export performance -

H1 exports volume @ 2.1 vs 1.5 million

H1 export sales @ 331 vs 294 cr

Trade receivables have increased in H1 due greater growth in export sales. Export sales have higher receivable cycles

Export customers, dialling down their Chinese imports and ramping up their India imports - a huge positive for the company. Expect alloy wheel exports to further pick up by next FY

Hopeful of getting alloy wheel orders from Maruti Suzuki. That should come as a nice trigger for the company

Uptick in the CV cycle is another tail wind for the company

Company setting up capacity of steering aluminium knuckles. To have a revenue potential of Rs 220-250 odd cr by FY 25. It’s an import substitute, no other manufacturer in India. This business can grow 5-10 times in next 5-7 yrs as industry shifts from steel to aluminium knuckles. Here, the margin profile should be similar to alloy wheels. Total capex for this to be around 200 cr. Out of this 50 cr odd to be spent this yr and the rest in FY 25

Alloy wheels is a high growth Mkt as more customers opt for alloy vs steel wheels

Current Debt on books at around 800 cr

Company has acquired AMW auto components for about 140 cr. Expecting a revenue of aprox 150 cr for FY 25. Should pick up further in FY 26. AMW auto components is into manufacturing of large steel wheels

Avg EBITDA margin difference between domestic alloy vs domestic steel wheel supplies is around 400 bps ( ie 4 pc ). For exports business, this margin gap is lower

FY 24 revenue guidance @ 4500-4700 cr odd with slight margin improvement in H2

Disc: holding, biased, not SEBI registered

Here is an interesting article on the alloy wheels market in India. Alloy wheels: A preliminary analysis in the Indian context | Team-BHP

TLDR

Some brief notes from the management meet that I attended recently:

• Exports should be around 600Cr for the whole year

• Exports can kick in and ramp up the volume growth further – 1L in first half itself (40k in last year) – $300m+ size opportunity – we are looking to get 1-3% market share, if not more – huge opportunity size in exports and we are looking to grow along with the demand and market scenario that is there in front of us – all the domestic companies can be winners (including competitors) – European players losing ground – time for Asian players to be aggressive

• Even if the OEMs plan to shift 5-10% of their procurement from China – India may not even be able to serve it – that is the size of opportunity in front of us and Wheels India, Minda, etc.

• Expects revenue from knuckles to be around INR35-40 crores in FY25 (no revenues to be recognised this FY)

• Margins going forward can be around 11.2-13% - as the mix tilts more towards alloy

• Steel Wheels – Volumes are high but the growth in volumes is low

• AMW may take 5-6 months to become fully operational after Dec this year – focus will begin from CV Segment

• FY26 will be the year when AMW will meaningfully start contributing to the revenues

• No meaningful difference in margins in AMW segment – in fact, consolidated margins may be slightly lower for the next 2 years because of the high fixed cost – but the company is trying its best to not have an adverse impact on the existing business margins

• Can expect some good progress on the Maruti deal front in the next concall

• Company level ROCE should sustain above 20%

• Revenues should be around 4500Cr for FY24 and 5200Cr for FY25 (some changes can be there due to value changes due to RM price changes)

• Volume Growth should be 12-13% this FY and 10-12%+ for next FY

• 4W business is protected due to BIS and anti dumping duties – similar protection is not available for 2W

• 4W Segment – imports have come down dramatically from 50% earlier – not seeing it go back to those levels again

• Market share is most critical – our aim is to get more market share

Management seems to have a lot of clarity and confidence in the business and its growth potential. Really like the tone of the mgmt. Let’s see how it pans out!

Disc: Invested

SSWL Sales Volume Up by 14% yoy, in November 2023

Monthly Sales in Exports - (Grew by 344% yoy by Volume)

Monthly Sales in CV Wheels - (Grew by 22 % yoy by Volume)

52bac71b-f68d-4383-a288-d093fff2fd4a.pdf (334.1 KB)

I was going thorugh the insider trading data

I found SSWL mgnt itself is selling holdings.

Rajesh Trikha: Executive director of SSWL

Sold: 8,02,455 on 20-Dec

Naveen Sorot : CFO SSWL

Sold: 10,78,052 on 20-Dec

SUNENA GARG: Promoters

Sold: 7,92,35,280 on 14-Dec-23

Is something fishy ongoing ?

6,46,042 sale by promoter in August 2023 is just 0.41%

The recent sale is less than half of that. The promoter holds over 62% stake in the company. So this share sale need not be given much importance, IMHO.

Q3 FY24 sales is at 1100 cr vs Q3 FY23 sales of Rs. 938 cr. That’s a 17% jump. Although sequentially its down by 3%.

There is a de-growth is alloy segment which is supposed to be margin accretive.

Couple of Research reports for useful info

Steel Strips Wheels Ltd - Q2FY24 Result Update - 31102023_31-10-2023_12.pdf (721.7 KB)

638342793414708097_Steel Strips Wheels Ltd - Q2FY24 Result Update - SMIFS Institutional Research.pdf (1.1 MB)