Star Health and allied insurance company ltd -

Q2 and H1 Concall and results highlights -

Health Insurance is the largest segment in the general insurance industry, contributing to 39 pc of Gross Written Premiums ( GWPs ) for the Industry

H1 - Key performance indicators -

GWP - 7847 vs 6680 cr, up 17 pc

Retail health insurance renewal ratio - 94 vs 99 pc

No of agents - 7.42 lakh vs 66.6 lakh

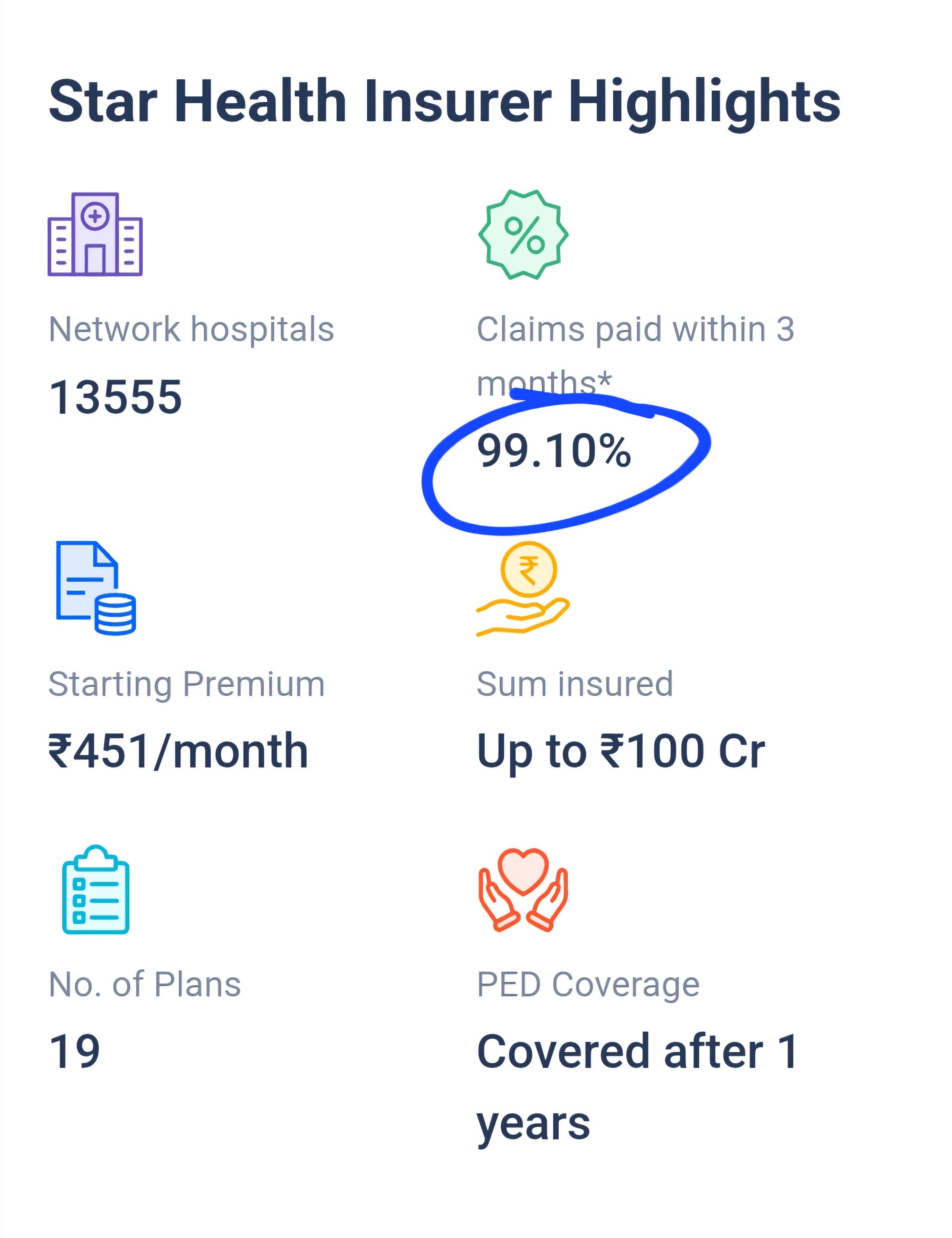

No of hospitals covered - 14.4k vs 14.2k

No of branches - 902 vs 881

Combined ratio - 101.1 vs 98.5 pc

Underwriting profit / loss - (-) 55 vs (+) 66 cr

Investment assets @ 16.4 k vs 14 k cr

Investment income - 650 vs 505 cr, up 29 pc

Investment yield @ 8.14 vs 7.38 pc

PAT - 430 vs 413 cr

Breakup of combined ratio in H1 -

Expense ratio @ 30.8 vs 31.4 pc

Claims ratio @ 70.2 vs 67.1 pc

Breakup of GWP in H1 -

Retail health + Retail travel + Personal accident GWP @ 7.1k vs 6.7k cr

Group health GWP @ 700 vs 500 cr

Company has bancassurance tie-ups with the likes of - KVB, PNB, UCO bank, IDFC First, BoB, Federal Bank, BoI

Other channel partners include - IIFL, Policy Bazaar, Tata Capital

Fresh to Renewal policies ratio for H1 stood @ 25:75

Avg sum insured for the company increased by 6 pc to 10.3 lakh per policy. 5 lakh and above sum insured policies now constitute 82 pc of company’s retail portfolio vs 77 pc at the end of H1 LY

Company has taken price hikes in H1 and those have been absorbed well by the Mkt

Channel wise contribution to business -

Agency - 80 pc, grew by 17 pc

Bancassurance - 8 pc, grew by 25 pc

Corporate - 4 pc, grew by 231 pc

Digital - 8 pc ( includes both - third party aggregators + company’s own digital channel )

15 pc of company’s premium is collected via specialised policies. These specialised policies include -

Star cancer care

Star senior citizens

Star cardiac care

Young star

Women care

Star Diabetes safe

Company has a whopping 31 pc mkt share in retail Health Insurance space in India. It’s a fast growing, under-penetrated industry. Company is the largest health Insurance company in India

79 pc of claims processed by the company were cashless in Q2

Company is investing aggressively in Preventive Health checkups, digital initiatives to detect and prevent online frauds. The preventive health check ups are costing the company @ 0.6 pc on the claims ratio - but they strongly believe that its an investment for the future and should yield good results

Company’s app downloads stand @ 74 vs 44 lakh YoY

Q2 - key performance indicators -

Combined ratio @ 103 vs 99.2 pc

Claims ratio @ 72.8 vs 68.7 pc

Expense ratio @ 30.2 vs 30.6 pc

Investment income @ 354 vs 255 cr

PAT - 111 vs 125 cr

Company reiterated their aspiration to reach GWP of 30k cr and PAT of 2500 cr by FY 28

Company was a victim of a cyber attack in Q2 which led to data leak iro its customers. They have responded swiftly, engaged cyber security experts and have taken down the stolen data from open sources

Q2 this FY saw an increased loss ratio due increased severity of seasonal disease outbreaks vs LY. Also, company’s Group insurance business share is increasing. Group insurance business always has higher Loss ratios vs retail business. Third factor behind increased loss ratio was medical inflation

Loss ratios typically moderate in Q3 and Q4. Company is hoping for a similar trend to play out in H2

Seeing the trend of elevated loss ratios, company has taken price hikes some of their products and is contemplating price hikes in some other products in near future. Despite the price hikes, company is seeing good business momentum across its products

Company aims to bring its expenses ratio down by 100 bps ( ie 1 pc ) for full FY 25 vs FY 24. On the claims side, it ll be challenging to bring down the claims ratio by 100 bps but they are trying to manage it by taking price hikes

Porting-in remains @ 10-12 pc of their new business

By end of FY 25, company believes almost 50-60 pc of their business will be re-priced upwards

Q1 and Q2 are always heavy on the claims ratio ( specially Q2 ). Claims ratios generally taper off in Q3, Q4. Company is hoping for the same to play out in current FY as well

Company intends to reach 18k cr of GWP for the current FY and they think that they r on track to achieve the same

The digital distribution channel is the fastest growing channel for the company and they r investing heavily behind the same

Company feels the premiums in Mid Corporates and Big Corporates are becoming unattractive and company intends to scale down this portion of their group health business. However, the premiums in small corporates and MSME group health insurance business are attractive

The total quantum of price hikes that the company intends to take before the end of current FY ( on 50-60 pc of their portfolio ) is expected to be around 10 pc

On way to counter medical inflation is to direct more people towards their preferred network of Hospitals ( the ones that don’t over-charge )

The medium term objective for the company is to reach a combined ratio of 96-97 pc

As an industry leader in Health Insurance, they continue to expand the market by investing behind field force, branches in the tier - 2,3,4 towns. This is what is driving the volume growth for the company

Disc: hold a tracking position, may add more if the business performance improves, not SEBI registered, biased, not a buy/sell recommendation