I have taken total Health segment data for HDFC ergo.

Source: Public disclosure

@murali603

Though logically, it looks like higher settlement ratio attracts more customers, a combo of 85% settlement ratio+lower premium can also attract customers.

Because based on the 6 year data that you have provided, HDFC Ergo is consistently ~97% and Star is consistently at ~85% but still even after 6 years of such consistency, both Star and HDFC Ergo are growing at 18% and are targeting 18% in future too.

So higher settlement is not helping Ergo to grow its premium. If the gross premium is not increasing, one should assume market share is also not increasing significantly. Is there any data of Ergo’s health care market share historically?

2 Likes

For most of the people claim settlement is important even if the premium is 2-3k higher as compared to other insurance companies.

If i am paying 20k premium and claim is rejected means there is no meaning of paying 20k for 5-6 years, rather i prefer paying 2k extra every year and make sure that they will settle claim

2 Likes

The claim is getting rejected for only 15% of the insurers who may be the category of people who does not disclose the facts/limitations that are specified in the policy or unknowingly opted for the policy without knowing certain features/limitations that are not covered. On the other hand, Ergo may be covering most of the features for a higher cost and hence claim ratio is high.

What i mean is this slightly lower claim ratio may be due to customers with limited knowledge about policy.

Anyway we will get to know the facts in the next 3 yrs if Ergo significantly increase its market share because of having highest claim ratio in the sector. I still believe Star may loose market share slightly or remain same at 30% due to very high competition in this sector.

3 Likes

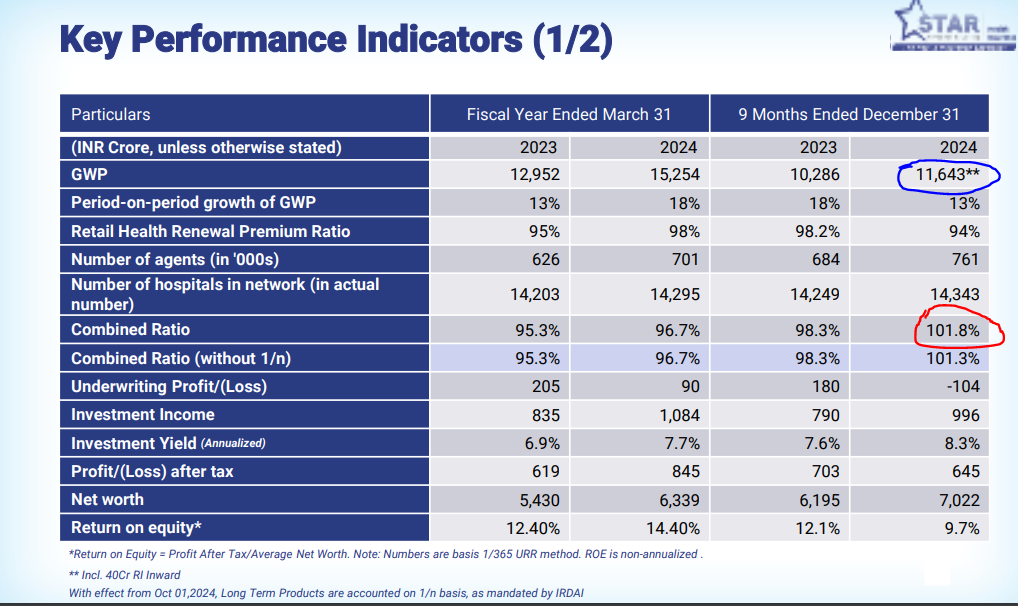

Q3FY25 Result

Overall GWP grew by 16 and retail health grew by 13%.

Mktcap/GWP = 1.48

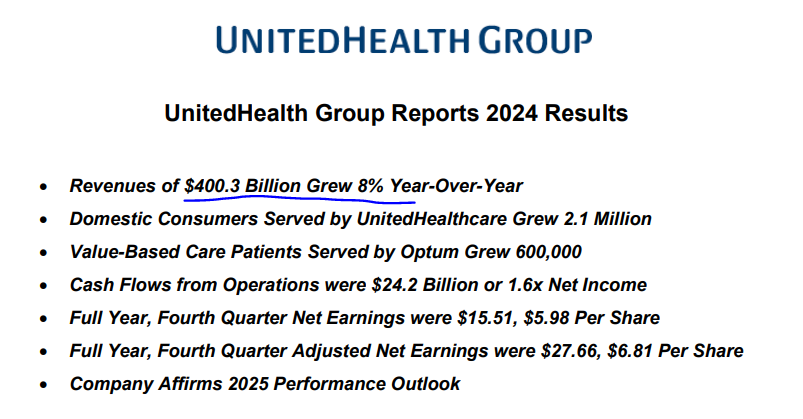

United Healthcare Latest Result (US health insurance leader )

Mktcap/GWP = 1.25

At mkt cap/GWP of 1.48, this sector leader looks cheap considering its growth prospects.

If combined ratio mean reverts to 96% and hence metrics like RoE, then this stock must get rerated.

I have 2 questions.

Can i assume this combined ratio of 101% is just a short term issue?

What is the appropriate valuation multiple in terms of Mktcap/GWP for health insurance company in India?

4 Likes

Deal of Magma Insurance is done at ~ 1.25 Market Cap/GWP. Magma is a general insurance company.

https://www.google.com/amp/s/www.business-standard.com/amp/companies/news/patanjali-buys-majority-stake-in-magma-general-insurance-for-rs-4-500-cr-125031301122_1.html

Zurich Kotak deal was at a valuation of 7 times GWP-

https://www.google.com/amp/s/www.business-standard.com/amp/companies/news/patanjali-buys-majority-stake-in-magma-general-insurance-for-rs-4-500-cr-125031301122_1.html

Both are general insurance companies, so it is not like to like comparison. Combined ratio appears to be north of 115% for both these companies.

1 Like

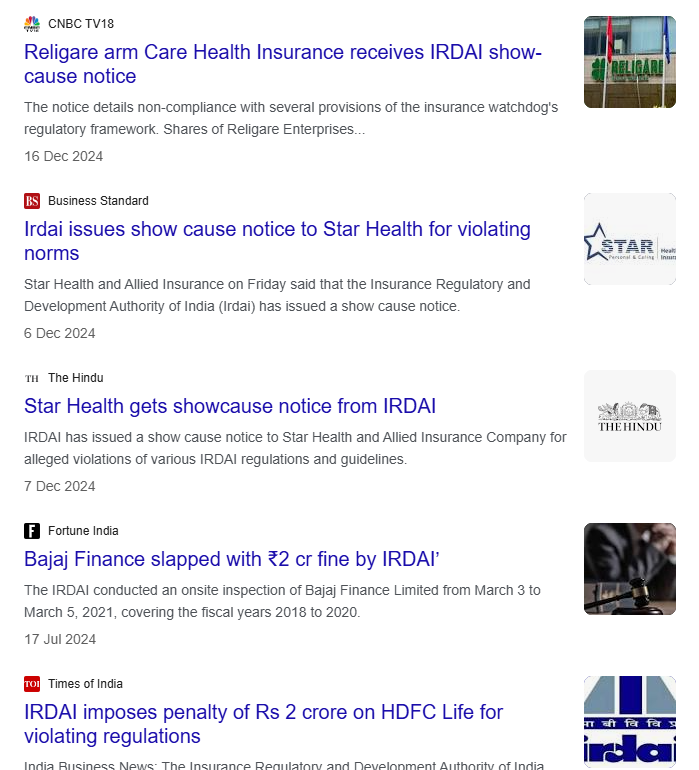

This can be a serious issue for Star Health to get new business. Need to see closely

1 Like

The company has issued a clarification for the same.

The IRDAI audits and thematic inspections part of its regulatory oversight. These type of audits and inspection are commonly reported about different insurance companies and some NBFCs, and sometimes also involve financial penalties ( 1 to 2 cr).

It is my personal view that are minor operational issues and should not be construed as failure on the part of company or management.

Disclosure : Invested

An influx of unquantifiable pessimistic news can sometimes be a sign that buying is around the corner.

Personal views, not invested.

This issue has been going on for quite some time now.

This following link is of a news article dated September 11, 2023 wherein it is mentioned that Star Health had issued notices to >100 hospitals in Gujrat and asked them to stop cashless claims alleging fraudulent claims.

(Star Health: Star Health clashes with Ahmedabad hospitals over 'fraudulent' claims - The Economic Times)

I know from an acquaintance that such instances are more prevalent than we tend to believe (not alluding to Ahmedabad Hospitals or Star Health Insurance).

My employer provides medical reimbursement and have empanelled hospitals wherein cashless claims can be availed. I have observed that hospitals tend to overcharge for various services and prolong patient stays unnecessarily when they are aware that the expenses will be covered by a third party, such as an employer or insurer.

I am sure Star Health would have legitimate grievances regarding billing practices of certain hospitals.

P.S. - Citing low charges and unjustified deductions, Ahmedabad-based hospitals and nursing homes have announced the indefinite suspension of cashless services for policyholders of Tata AIG General Insurance, Care Health Insurance, and Star Health and Allied Insurance with effect from April 2, 2025.

The large corporate hospitals has a high capex investment, which primarily done on anticipation of consistent inflow of patients for surgery and high value procedures, through insurance companies, which often account for more than 50 percent cases , and in some hospitals more than 2/3 of cases. These hospitals often attract patients because of their cash less empanelment with insurance companies , not the because of their reputation.

In cases suspension of cash less services, some of the larger hospitals will loss significant business as people tend to converge to more reputed hospitals and clinics if they have to pay from their end or get the insurance bill settled later.

Either of the case, some of the hospitals will be at greater loss from this arrangement than others, so it’s difficult to maintain the unity in this protest/ Suspension for long.

Over billing and over treatment and the settlement by few hospitals is a genuine concern which continuous tug of war between hospitals and insurance agencies.

On this issue, the patients, government agencies and insurance companies are on same page, that some hospitals do sometimes charge more than it should be. Patients ends up paying higher primium and insurance companies ends up having un sustainable combined ratio. Even government have a similar view because they find it difficult to implement Aayushman Bharat scheme which have relative lower rates of reimbursement for procedures than the prevalent hospital rates.

At the end of the day, if there is any settlement( brokered by government agencies), it’s going to in the favour of Insurance companies which means benefit to patient ( lower premium) and against the intrest of hospitals.

Till then this tug of war will go on.

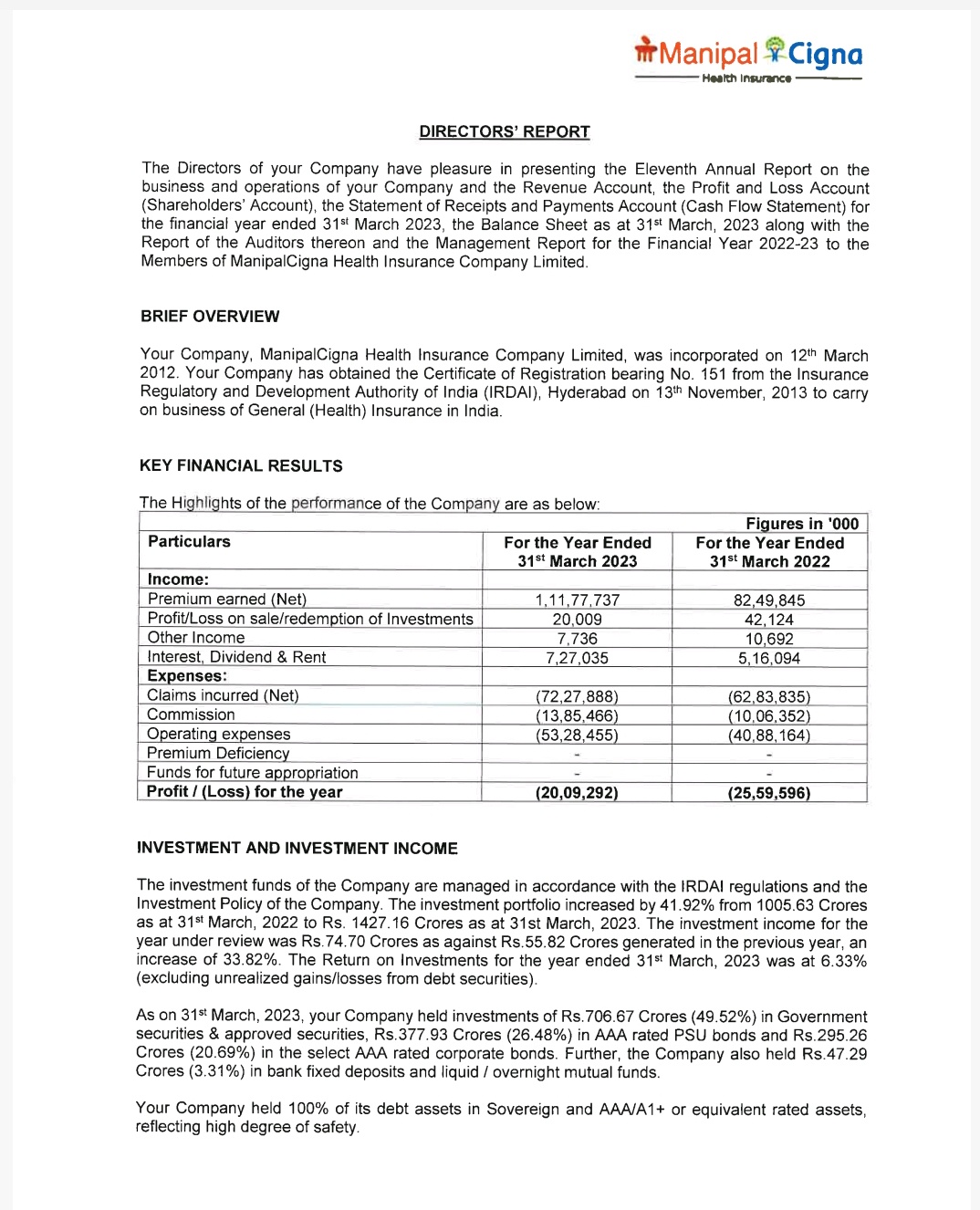

LIC- Manipal Cigna deal is at ~ 2 FY24 GWP. LIC set to buy 40-49% stake in ManipalCigna; primary and secondary deal values company at Rs 3,500 crore - The Economic Times

Star Health marketcap is at 1.4 times FY 24 GWP. Manipal Cigna claim settlement image is no better than Start Health. A lot of future negativity is in built in Star Health stock price.

3 Likes

If we look at the results of Manipal Cigna 2023, company has claim losses of around -722 Cr and Investment Income of mere 20 Cr. This resulted in the total loss of more than -200 Crs for that financial year ( commission and operational expenses including).

If you look at the similar values for Star health , it has claim profit of 706 Cr plus the investment income 333 Cr , which resulted in a gross profit of 826 Cr ( again including commission and operations cost).

I have no similar data for manipal signa for 2024 but it is available for Star health

The claim income increase to 860 cr and investment income to 442 Cr.

I have opinion that comparing the valuation of Star health and Mahipal cigna, on the basis of market to GWP ratio doesn’t paint a right picture. On this issue I have following take

1.Going forward, we may witness times when star health have fluctuations in claims ratio and earning, but the investment income is going to steadily increased.

2. The scale and operation efficiency ( agent count and hospital association) is a dificult capability to achieve especially those which lack the firstover advantages.

3. Health insurance is still under penetrate so there is a growing market size. It will allow many new player to come and grow. If they can replace Star health from its position, is something to look for

Disclaimer: invested ,

I am not a Sebi registered research analyst.

3 Likes

This makes for an interesting read. Interview with the Chairman.

Star health posted good set of numbers with steady growth in premiums. Claims ratio was higher YoY as a result of which combined ratio also increased YoY. Net profit growth according to IFRS accounting increased at healthy pace and was mainly owing to jump in investment income. Going ahead, the loss ratios are expected to improve.

2 Likes

Wouldn’t CARE or any digital first player erode away STAR’s market share?

CARE has been aggressively gaining market share by going digital first and keeping its sales teams lean. STAR’s moat is its 8 lakh agents. If STAR starts offering lower premiums on its website or through PolicyBazaar to match CARE, its agents lose their their commissions and stop selling STAR (A channel that gets 80% of the business)

So basically CARE can price aggressively without upsetting anyone. I wonder how Star can compete.

A second unrelated and short term focused point. In Q3 FY26, Star increased its equity exposure to ~18%. Hence due to the recent market correction I expect a reduction in profits this quarter.

1 Like

We may need to think about all these things if customers are willing to buy star health insurance, but in my opinion its not the case.

Last 6 quarters top line is almost constant but bottom line is struggling with instable margins.

Star trying to keep premium as low as possible but issue is rejecting claims to protect their balance sheet. Star health & CARE claim issues are spreading like anything and one day no retailer would dare to buy insurance from these fraudsters and pay some extra premium to ICICI Lombord or HDFC Ergo and protect their family from claim rejections.

How remote insurance provider can decide whether patient needs admission or he can survive with OTC medicines? Its just hamulating the insured person and the health care providers.

They will badly punished for such illogical things and they can’t afford to correct these things in the future as well.

1 Like