Conference Call Notes- Star Health Insurance-Q4FY2023-24

Profitability: We have achieved underwriting profit of ₹204 crore with a combined ratio of 95.3% and an overall PAT of ₹619 crore, which is the highest in our history.

FY2023-24 will be one full year with price increase that we have taken, we should return to healthy ROEs of 16% to 18%. Once we implement IFRS where the cost is deferred over the policy period (today only the premium is deferred as the cost is upfront), ROE will improve by 300-400 basis points.

Risk-based solvency will ensure that the solvency for us will be very, very comfortable (mostly because of granularity and growth). If risk-based solvency comes, we will be in a position to pay dividend as well.

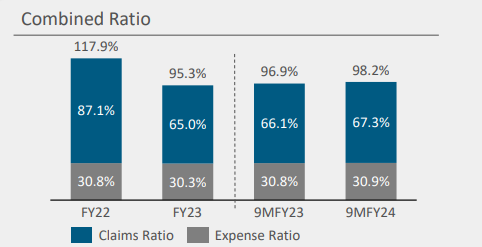

Combined and Loss ratio: Combined ratio for FY2023 has improved to 95.3% versus 117.9% in FY2022. For Q4 FY2023, we have achieved a combined ratio of 91.3%. Loss ratios for April 2023 is also better than the previous year. We will improve the loss ratio compared to full last year number. (I am not sure how they can be sure about this? What if there is another Covid wave or some other health emergency?)

Expense ratio has improved despite a significant cutback in the group business which has a lesser expense ratio.

Revenue and market Share:

For 12 months, FY2023, our retail health has grown by close to 18% versus the industry’s retail health growth of 15.3%. i.e. 1.17 times the industry growth rate despite a very large base.

For FY2023, our retail market share is 34% against 33% of the last financial year, which is 3 times the second largest player in the industry. Star Health has registered close to 40% retail health accretion market share in FY2023

We continue to aspire to grow higher than the market growth rate and increase our retail health market share every year.

We have also made a very strong start to the new financial year in FY2024 as we speak up to the date, our premium growth for the month is more than 27% and we expect to close this month with around 25% growth.

Group Business: Group business strategy of running down the book was up to the last financial year. We have continued to focus on profitable group business, which is largely the SME segment and so the growth is coming back in group business. This is a quasi-retail model (he probably meant SME segment).

Investments:

Investment assets have grown to ₹13,392 crore in FY2023 versus ₹11,373 crore in FY2022. for FY23, investment income grew to ₹835 crore versus ₹793 crore for FY2022.

Portfolio yield for Q4 FY2023 rose to 7.34% versus 6.71% of Q4 FY2022. We continue to invest in equity portfolios through ETFs. 4.1% of the portfolio is in ETF, we have decided to increase this upto 7%.

Distribution:

Agency business continues to contribute around 82% of the overall business. Our agency strength has increased to 6,25,860 agents. For the full year FY2023, we have added approximately 76,000 new agents over the previous year.

Digital sourcing from our web sales and tele-sales models has grown by 28% in FY 2023 to ₹625 crore for the over the previous. Our app downloads have reached 2 million downloads

We tied up with some leading banks namely Standard Chartered Bank, India Post Payments Bank and ESAF Small Finance Bank for distribution. Premium contributed from this channel has grown by 43% during the year. EoM regulations as well as the opening up of Banca business to 9 players will help us to get into newer channels and continue to grow our profitable mix of business.

Revenue drivers:

The average sum assured of new policies has increased by 13% on a year-on-year basis to ₹9 lakh per policy. ₹5 lakh sum assured and above now constitute 70% of the health insurance portfolio which was 64% in the last financial year. FY2023, growth 50% contribution by volume and by value. We had grown by 18% in retail health business. 9% is policy growth and 9% is value. For FY2023-24, around 55% to 60% growth in revenue will be achieved through price hikes (value) and 40% to 45% by volume growth.

Claims:

Four pronged strategy- a) prudent claims settlement based on our rich medical expertise, b) volume based pricing arrangement with our network hospitals, c) technology enabled, fraud detection and mitigation and d) risk based pricing through micro segmentation of portfolio.

73% of number of paid claims in the financial year 2023 are through cashless versus 63% in the previous financial year.

With Anti-fraud detection, there is a 1.3% incremental benefit in terms of lower claims ratio in FY2023 versus FY2022.

Miscellaneous bits-

We are launching a new Wellness proposition for our customers as well as non-customers who will benefit from our telemedicine expertise and also earn rewards from leading healthy lifestyles. This will lead to ‘leads’ for prospective customers.

We get around 200 plus applications from different hospitals for admission in agreed network. Our empaneled hospitals have crossed 14,000 and there is a constant effort to convert most of these empaneled hospitals into our agreed pricing. There is an exclusive team in Star to talk to hospitals and arrive at a fare pricing for identifying surgical procedures and also to fit a proper price for medical management, room rents, professional charges, common diagnostic tests and all that.

about 2.5% of our policies are coming from long term plans. on the online platform or digital channels, almost 50% of our new customers in the recent past is coming from long-term plans. So, we will be focusing on these plans going forward.

Disc- Invested