Here are the notes from Q3 FY22 Concall.

-

Revenue guidance is 20% growth for next year as a conservative estimate

-

EBITDA guidance remains in 12-13%. This quarter it is 15% however CEO mentioned it is exceptional due to some projects on verge of completion

-

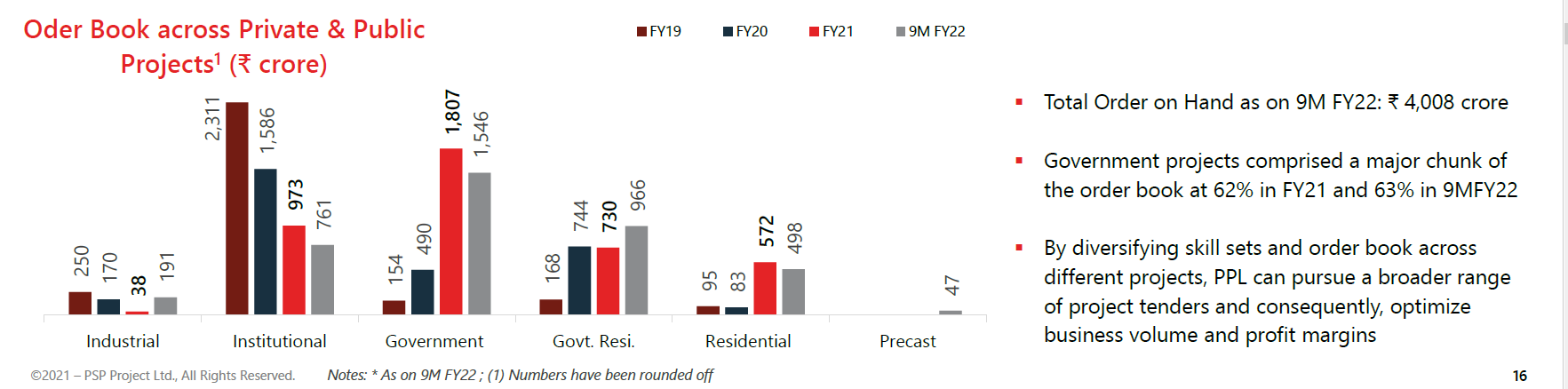

Existing Order book of ~3500 Cr which also includes 1171 Cr Central Vista project. The guidance given for order book is also 3500 Cr by Q4 FY22

-

CEO mentioned that starting from Feb 2022, once they complete Surat Diamond Bourse project (1775 Cr), they will be eligible for bigger projects i.e, more than 1000 Cr revenue

-

CEO hinted that they are looking for a project of expansion of Kashi Viswanadh dham project to other parts of India which will be more than 1000 Cr

-

The capex for the precast was 109 Cr and expected to recover the cost in 4 to 5 years. L&T has awarded the first order worth 46.5 Cr. The maximum revenue estimate for precast facility is 300 Cr per year.

-

Pandharpur project which is of order 150 Cr is right now at a halt. 20 Cr receivable amount is pending and the client is having financial issue

-

EWS Housing Bhiwandi is stopped as PSP did not find it profitable to proceed further as mentioned in Q1 FY22 concall

-

Gross Debt is 185 Cr and Cash Balance in bank is 215 Cr

-

US subsidiary is successfully divested for USD 10,000

-

The FY22 revenue guidance of 1600-1700 Cr provided in earlier con calls seems to be on track and management confirmed the same.

Valuation -

TTM EPS is 41.46 Rs

CMP 575.35

P/E ~14

D/E 0.32

CEO’s vision especially he is not interested to venture into any PPP projects and stopping projects wherever there is a finance default is commendable.

Overall, the execution seems to be good and the company’s growth trajectory seems intact. The central vista has around 15,000 Cr worth projects which are yet to be allocated. With Surat Diamond Bourse almost getting completed, the company will be eligible for projects worth more than 2000 Cr from Feb 2022. As the company recently completed the Kashi Viswanadh Dham corridor project in Varanasi and based on the concall, there is a high chance the company will be a strong contender for the subsequent roll out project which is meant to other parts of India.

With a strong balance sheet and diversified order book, CEO delivering as per the estimates, I believe the stock price will move further up. The only key risk I see is 63% of the projects are from government but CEO clarified that unless they see strong funding available, they are not planning to proceed. So far, only the Bhiwandi and Pandharpur projects from government did not turn out for better.

Discl - Invested 4% of PF.