Excellent Quarterly Results Sonata Software

Stock P/E:19.9

ROCE:43.7 %

ROE: 37.2%

Last 10 years’ CAGR is 67%, though for the last 3 years is not so impressive 16%.

Another negative is that it has risen by about ₹90 in the last one month.

Good Sets of Results from Sonata Sofware in a tough environment.

The company is making key bets, especially in the AI and generative AI space. Sonata aims to lead the AI wave from the front with its AI power solutions of Harmoni.AI and we expect that to be a 25% of our revenue in two to three years’ time from now.

Dividend of Rs. 7 per share ( Record Date: 1. 7th November, 2023)

bonus issue of 1 (one) equity share for every 1 (one) equity

Hi, it’s been an year. Did you choose to invest in Sonata Software? The revenue increase has been as per management guidance, and Sonata’s 20% profit comes up from BFSI. I am positive about it’s upcoming result.

The market is highly rewarding good result in IT (OFSS), and punishing bad results (LTIM)

Good results but overall loss in quarter due to Quant Systems acquisition.

Also company had to pay extra 17 Crore extra due to change in valuation of Quant.

The recent correction makes the stock a very compelling buy.

The company is operating in an industry which has severe headwinds where the large players are taking a beat.

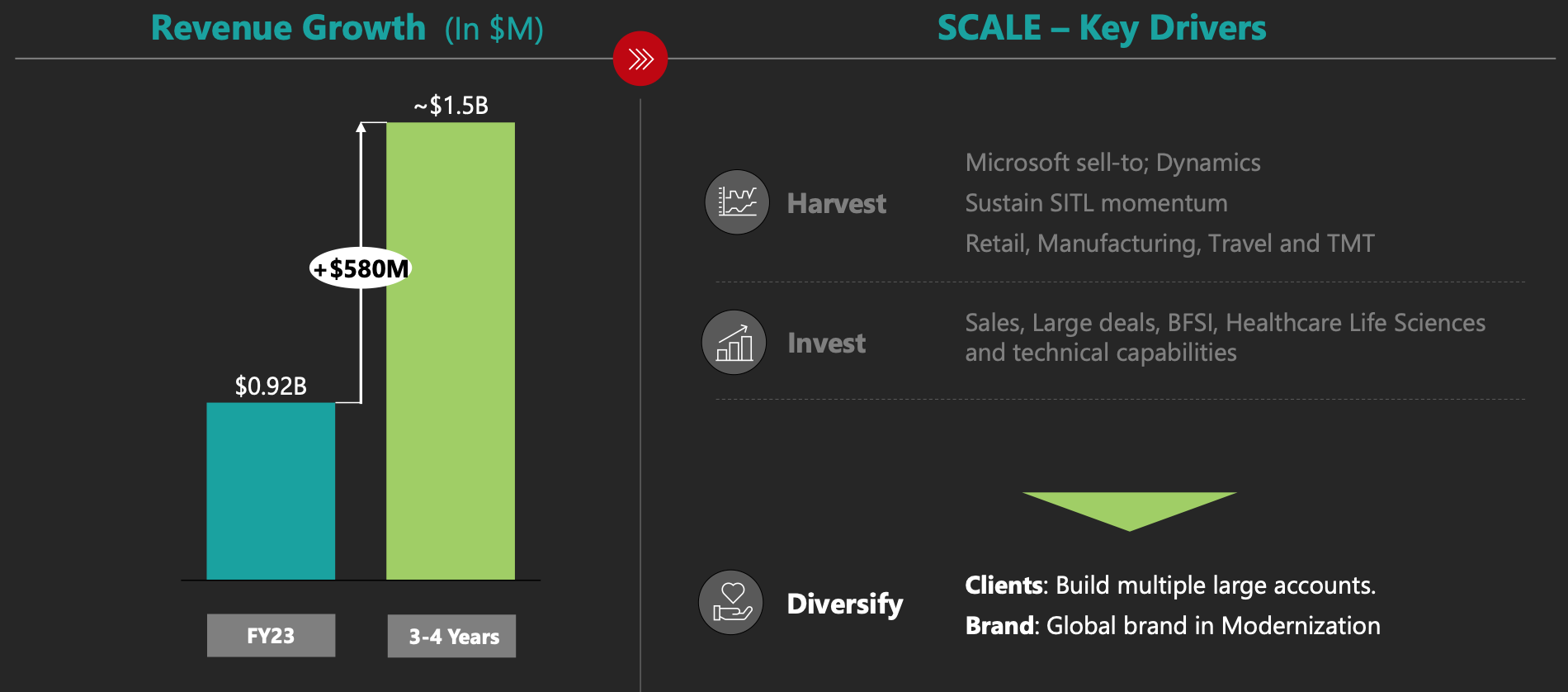

However, the bet is extremely favourable (imo) as it operates in very lucrative and growth industries like * Healthcare, Life Sciences, BFSI, Retail Manufacturing, and TMT across key geographies. Aiming to reach $1.5 Billion revenue by FY26.

Need some help to understand sonata business better as I was looking at operating margins for over last few years and they have always been in single digit(8+9%). I compared it against the other IT players and almost all of them have numbers in upwards of 15-25%, except tech Mahindra currently. Is this part of strategy for sonata team to keep numbers low to win the deals and why are these abysmally low compared to its peers. I am trying to learn about if this will always be the case for sonata in future as well OR if margins will eventually move closer to the industry benchmark

Aims to achieve $1.5 billion in revenue by the end of FY '26 for its international business, with an EBITDA margin in the low 20s.

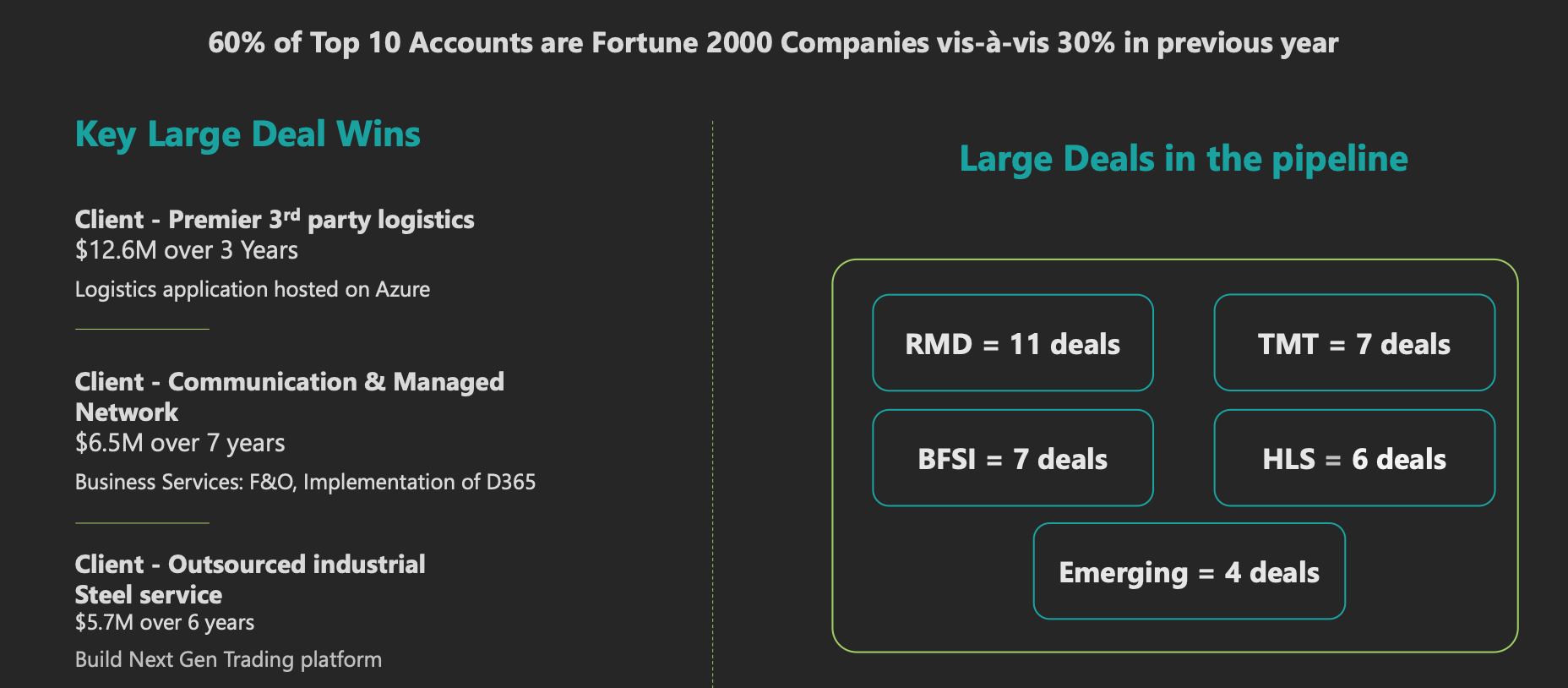

3 new big deals: Healthcare company in US (a 7 year deal), Manufacturing in Australia, BFSI in US. The Healthcare deal requires some initial investments in AI, which will lead to some short term margin impact. It’s onsite right now and will be taken offshore in a few quarters.

Sonata’s pipeline in cloud and data now represents 52% of the total pipeline, compared to 15% two years ago. The book-to-bill ratio stood at 1.24 for the International Services business, indicates a healthy demand.

Sonata now has 21 clients with an annual revenue run rate exceeding $3 million, compared to 16 last year.

There are 4 verticals in which Sonata is: Healthcare and Life Sciences, Banking, Financial Services, and Insurance (BFSI), Retail, Manufacturing and Hi-tech TMT (Technology, Media, and Telecom). Tailwinds in Healthcare and Life sciences while headwinds due to delays in deal decision-making and slow project completion in the UK, Europe and retail manufacturing. Also, the new Healthcare deal will be dilutive for the first two to three quarter and get profitability at the end of the fiscal year.

There was impact on Profitability due to: Forex losses, change in taxation due to SEZ moving into the second 5-year bracket and investments in AI for the new client.

The declines in ROCE and RONW is due to increase in borrowing from $43 million to $75 million.

The guidance for $0.5 billion to $1.5 billion target was that it will be delayed by 2-4 quarters. Healthcare will be bouncing back sooner while BFSI is taking time.

Earlier, large deals were closed in 1-2 quarters, but now this timeline has extended to 3-3.5 quarters due to decision delays (industry headwinds).

The Domestic business model is volume-driven with inherently low margins, to measure this business the better metric to use is absolute gross contribution rather than percentage margins.

Revenue wise H2 will be better than H1 however there will be margin pressure because of the deal.

High Tech, BFS, Healthcare verticals are key growth verticals, while retail (consumer-facing retailers) will remain soft for the next 2-3 quarters.

Some headwinds in Q2 & Q3 due to salary hikes, also, the healthcare deal is slightly margin dilutive compared to the company’s average margin, but it is not loss-making.

There are green shoots in BFS largely due to increase in discretionary spending. Also, Quant which was one of their acquisition is seasonal in nature (Q4 being softer).

The repayment of the loan for the acquisition of Quant has been delayed due to a procedural issue with the RBI. This issue is still ongoing and may take a couple of more quarters to resolve.

@swapnilr they are resellers of licensed for Microsoft products like O365, sharepoint,azure.started doing Aws and other cloud providers also recently

This business runs on significantly lower margin like <5 percent but is high on revenue

Its still a high roce recurring business but it makes the blended margin of the company(when taken with the traditional IT SERvices business ) around 8-9 business

The software reselling business is high on working capital