Its b2b business. Margins are very low and microsoft gives very aggressive targets

2 Likes

But why software reselling needs high working capital? That too well known Microsoft software products.

1 Like

@Sudhakar_Subramanian everytime you get an order for O365 you first get activate the license from

Microsoft platform by paying them money

Then you deliver to customer and collect as per the customer payment terms

These tend to be 30//60 days in large companies

Plus the margin you hVe fromMS is 2-3 percent

For Azure and AWS it might be slightly higher but its significantly lower than the IT Services business

3 Likes

They haven’t declared dividend after H1, this is quite uncommon since last few years. Anyone has any idea or insight on why it is not declared this time?

1 Like

3 Likes

But why does microsoft need reseller can’t they target their audience through website online.

Noob question ![]()

1 Like

I have seen in many companies that they prefer to sell to businesses through the partners. I have seen it happen for both big and small customers.

Few things which get unbundled to the partner are:-

- lead generation and sale

- customer engagement. (Partner will have lower cost)

- first level technical support

- incentives to partner to sell more / service better

- bundled pricing to partner

2 Likes

1 Like

Drop of almost 50% within one year from the highs, series of meetings with Institutional Investors. Wondering if some thing is coming up. Invested in this company for more than a decade. Never expected one or two quarters of below expectation performance will erode the value so much. Still want to remain invested, but little worried if this is optimism bias? Is it a time to pull out? any views please.

3 Likes

This article mostly covers all the points related to Share Price Sharp Correction, which are already known, but might help to understand all business related perspectives.

1 Like

Thank you @gsapte …helped to understand to some extent, will be interesting to see how management responds. Meeting with Institutional Investors has not helped in terms of Share price, in fact price dropped further!!!

Under General Update to stock exchange, Sonata informed for lower revenue from the largest client and as a result lower revenue from international business for the quarter than anticipation!!! Not clear why such declaration ahead of results? The stock in down by about 10% as a result of this update. is it normal practice or the results are going to be real bad. Time to buckle up!!!

Any idea what is going on? No information seems to be available apart from this “generic” update.

FYI, I am invested in this stock for long.

2 Likes

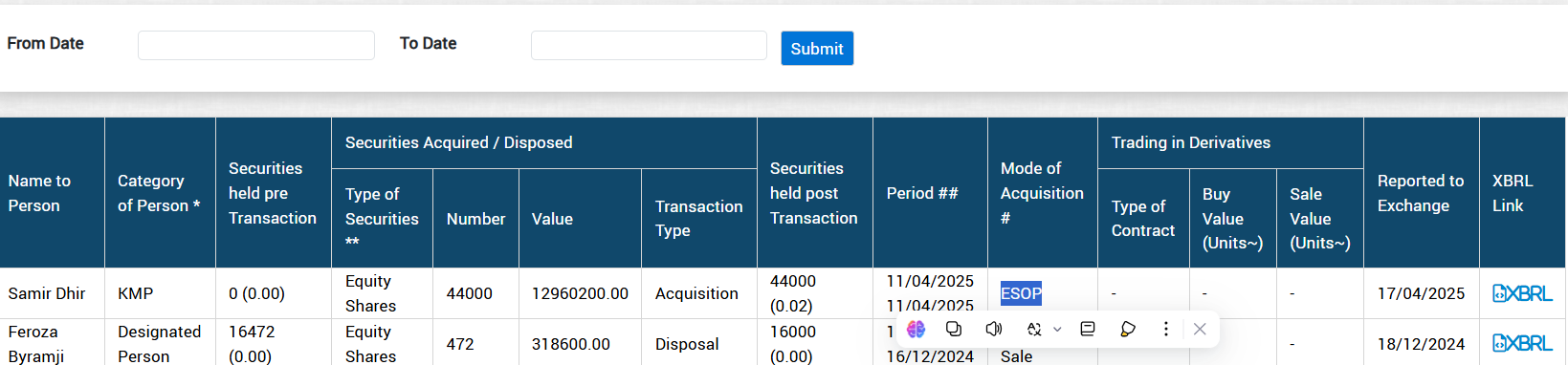

CEO of Sonata (Samir Dhir) acquires 44k shares on 11th April and followed by this update.

If the earnings goona weaker in a longer run, i don’t think CEO buys at this point?.

2 Likes

This are ESOP excercise and shall not be considered as open market purchase. ESOP are kind of incentive to top management, and generally issued at lower than prevailing market price.

Rs 1.29 Cr for 44,000 share give value of ~ Rs 295 per share as compared with Rs 315 per share current price.

I held Sonata software for very long period of time (first purchase in December 2015) as a dividend yield idea. Over a period, company went through mutiple ups and down and I also increased/reduced my holding depending on my comfort.

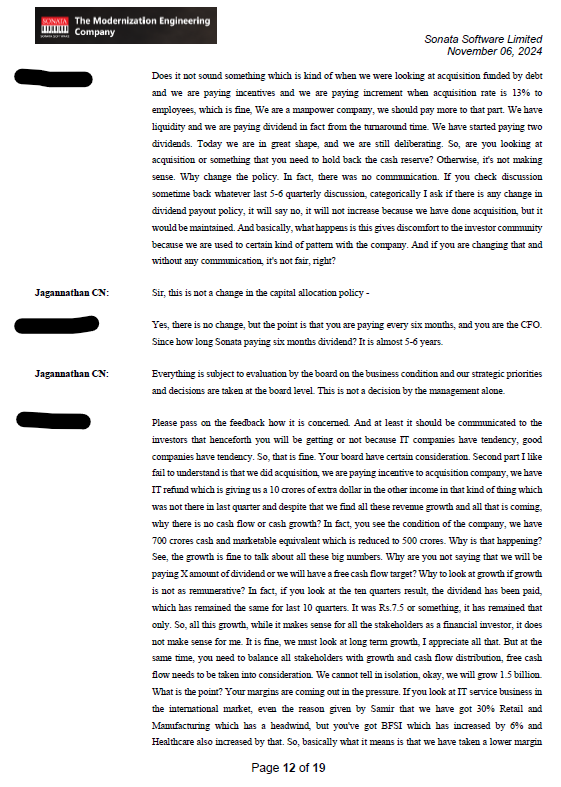

However, in last results for Sep/Dec 2024, the company stopped declaring interim dividend without citing any signficiant reason. When I asked specifically reasons for not declaring inteirm dividend, the management taken shelter of “board decision”. I could not understand when all stakeholders were given rewards higher than pervious year, what was reasons for the company to stop interim dividend, which it declared almost for last 20 years.

Extract from November 2024 transcript of Dividend rekated questions

Enclosed is interim dividend history of Sonata since calendar year 2000, which continued even during COVID period.

| COMPANY NAME | Dividend Type | Div % of FV | Ex-Dividend date | Year | DPS |

|---|---|---|---|---|---|

| Sonata | Interim | 20 | 27-Nov-00 | 2000 | 0.20 |

| Sonata | Interim | 20 | 31-Oct-01 | 2001 | 0.20 |

| Sonata | Interim | 20 | 13-Nov-02 | 2002 | 0.20 |

| Sonata | Interim | 20 | 10-Nov-03 | 2003 | 0.20 |

| Sonata | Interim | 30 | 01-Nov-04 | 2004 | 0.30 |

| Sonata | Interim | 40 | 27-Oct-05 | 2005 | 0.40 |

| Sonata | Interim | 50 | 27-Oct-06 | 2006 | 0.50 |

| Sonata | Interim | 50 | 26-Oct-07 | 2007 | 0.50 |

| Sonata | Interim | 100 | 26-Dec-08 | 2008 | 1.00 |

| Sonata | Interim | 50 | 17-Oct-08 | 2008 | 0.50 |

| Sonata | Interim | 90 | 20-Oct-09 | 2009 | 0.90 |

| Sonata | Interim | 100 | 16-Nov-10 | 2010 | 1.00 |

| Sonata | Interim | 50 | 09-Nov-11 | 2011 | 0.50 |

| Sonata | Interim | 50 | 19-Nov-12 | 2012 | 0.50 |

| Sonata | Interim | 100 | 14-Nov-13 | 2013 | 1.00 |

| Sonata | Interim | 100 | 13-Nov-14 | 2014 | 1.00 |

| Sonata | Interim | 350 | 10-Nov-15 | 2015 | 3.50 |

| Sonata | Interim | 350 | 09-Nov-16 | 2016 | 3.50 |

| Sonata | Interim | 550 | 16-Mar-16 | 2016 | 5.50 |

| Sonata | Interim | 375 | 20-Nov-17 | 2017 | 3.75 |

| Sonata | Interim | 475 | 13-Nov-18 | 2018 | 4.75 |

| Sonata | Interim | 575 | 07-Nov-19 | 2019 | 5.75 |

| Sonata | Interim | 400 | 18-Nov-20 | 2020 | 4.00 |

| Sonata | Interim | 1450 | 06-Mar-20 | 2020 | 14.50 |

| Sonata | Interim | 800 | 29-Oct-21 | 2021 | 8.00 |

| Sonata | Interim | 700 | 31-Oct-22 | 2022 | 9.33 |

| Sonata | Interim | 700 | 07-11-2023 | 2023 | 9.33 |

And now, this nearly 25 years old practice of dividend declared being scrapped and management does not even feel to provide valid explanation to shareholder was a major concern for me.

Post September 2024 result con call, I systmatically reduced my holding in the company as it was not giving me comfort on performance. Since the new MD Mr. Dhir takeover, the company has never increased dividend. We find good presenation with aspirational quote and revenue target, however, no follow up with growth in dividend since last 3 years. That was of kind of major alarm and resulted discomfort to me and hence I exited from investment last week fully.

Over 9 years period, including dividend, my XIRR from Sonata investment was around ~30%. (excluding dividend cashflow XIRR was ~27% per annum). Sonata has been excellent investment returned provider for me. First in 20th century when I got 300 shares allotment and alsmost sold IPO share with 12 months are 3 times investment supported by IT boom in late 1990s. My second phase was investment commenced from December 2015 and ended in April 2025. I would be grateful to Mr. P Srikar Reddy (ex MD and current Vice chairman) and ex Chairman Mr. Pradeep Shah, who grew dividend Rs 3.4 per share during FY16 to Rs 7.9 per share during FY22. Since April 2022, when Samir Dhir became CEO and shared his vision to make USD 1.5 billion revenue company, the company has failed to increase reward for shareholder which remain stagnant at Rs 7.8-Rs 8. I expect the dividend to decline during FY2025 due to weak performance and that too after stagnancy for 3 years. This was a major reason for me to exit from Sonata. While IT sector has faced headwind, but Sonata is probably only company which did not grew dividend in last 4 years. Most companies, despite headwind and large scale of operations, has grown that dividend.

Disclosure: My view may be biased due to my exit from Sonata. I have been multiple time worng in forecasting and may be wrong even in assessment of Sonata future. I am not suggesting any investment/divestment in the company. I am not SEBI registered advisor. I have sold Sonata shares during last 15 days.

12 Likes

Hi Dhiraj, thanks for a detailed write up on your investment thesis and how it panned out. I remember you doing something similar for Aarti Industries and these summaries are very helpful!

Sonata has historically quoted at slightly discounted valuation v/s peers and in post Covid19 IT boom, it was trading at lofty P/E of 40x-50x. From a selling thought process standpoint, would you overweigh a reduction in Dividend distribution as a trigger (as is the current case with Sonata) v./s exiting at bloated valuations (as was past scenario)? Above question is with the benefit of hindsight, but would like to understand your views.

Regards,

Kunal

2 Likes

While there is no perfect answer to perfect investment process, I strive to focus more on my investment process. In case of bloated valuation (like rerating in Sonata PE almost doubling), if the corrosponding busines fundamental are improving, I would carefully observevd, unless it reach crazy valuation like 100 PE. Even that I would hold if I see major growth driver (For instnace, I continue to hold ABB despite very high PE and rerating). Market is cyclical and I can not predict when to enter and exit in single company. I generally hold for more than 5 years and hence if business fundamental are improving/ remaining stable, I would continue to hold with vigilence.

However, in case of Sonata, while the topline was growing in last 2-3 years, from Rs 5,500 cr in FY22 to Rs 8,600 cr in FY24, the cashflow from operation declined from Rs 450 cr in FY22 to Rs 281 cr. Main reason in topline growth was acquisition and also increase in business from lower margin segment. While that may drive growth, it would not impact cashflow growth (which is prime importance in investment process, also reflected in dividend payment). Since there was no growth (rather decline) in free cashflow, there has been corroponding stabilisation of dividend. For same dividend per share, from FY22 to FY24 dividend payout ratio increased 58% to >100% and that is not sustaiable. With decline in FY25 performance, as an investor, I shall expect decline in Dividend, unless company declared special dividend/ or cash distribution from sell of assets. My investment apporach is company shall fund dividend from operating cashflow which shall be recurring and growing. Given the head wind faced by the company, acknowledged by management also in various press release, in addition, no communication to major policy change in dividend (just imagine discountinuation of 25 year policy of dividend payment without even giving any logical explanation), created discomfort for to hold Sonata in portfolio. I am very lazy person to act, but this situation was against core of investment process and hence exited. More than likely decline in dividend, the casual approach of management when asked about critical issue of dividend distribution, was a main factor for exiting. I do understand business would face problems and dividend would decline, but at least management shall be frank to accept same and give clear view. In case of Sonata, I find management was either not aware or wanted to avoid discussion on problem area. In either case, I would not like to be invested in company. We can not project future, but at least give true assessment of situation. Increasing lower margin business, purusing sales growth at cost of profit margin/cashflow and chasing growth by acquisition, I do not like such pursuit and hence exited. As mentioned, my view may biased and may be wrong. I wish Sonata come out of current chellanges with flying colours and continue excellent wealth creation for investor. However, I can not invest based on my well wishes and hence the decision. In case reader need more insight, please read transcript of last 4 calls. One can understand change in management focus of getting foture 500 client, large deal and achieve sales target, even if that mean compromise on cashflow and margin. The management declared two bonuses in last two year. If you can not increase dividend, give bonus. That may be help in short term in my view, but in long term, only thing mater is growth in operating cashlfow (and dividend, as management may deploy growth in cashflow in lower margin business and destroy value).

12 Likes

Sonata opens 200,000 sq ft Hyderabad facility, plans 5,000 jobs over 3-5 years. Seems to be a positive sign on their growth outlook.

4 Likes

After skipping half yearly dividend last FY, going by the communication, Sonata Software seems thinking of Interim dividend during Q1 results !!!

3 Likes