Q3 results (Link)

EPS up by 18%. Continued on going execution with focus on Platformization

Investor Presentation - link

Disclosure: Invested

Q3 results (Link)

EPS up by 18%. Continued on going execution with focus on Platformization

Investor Presentation - link

Disclosure: Invested

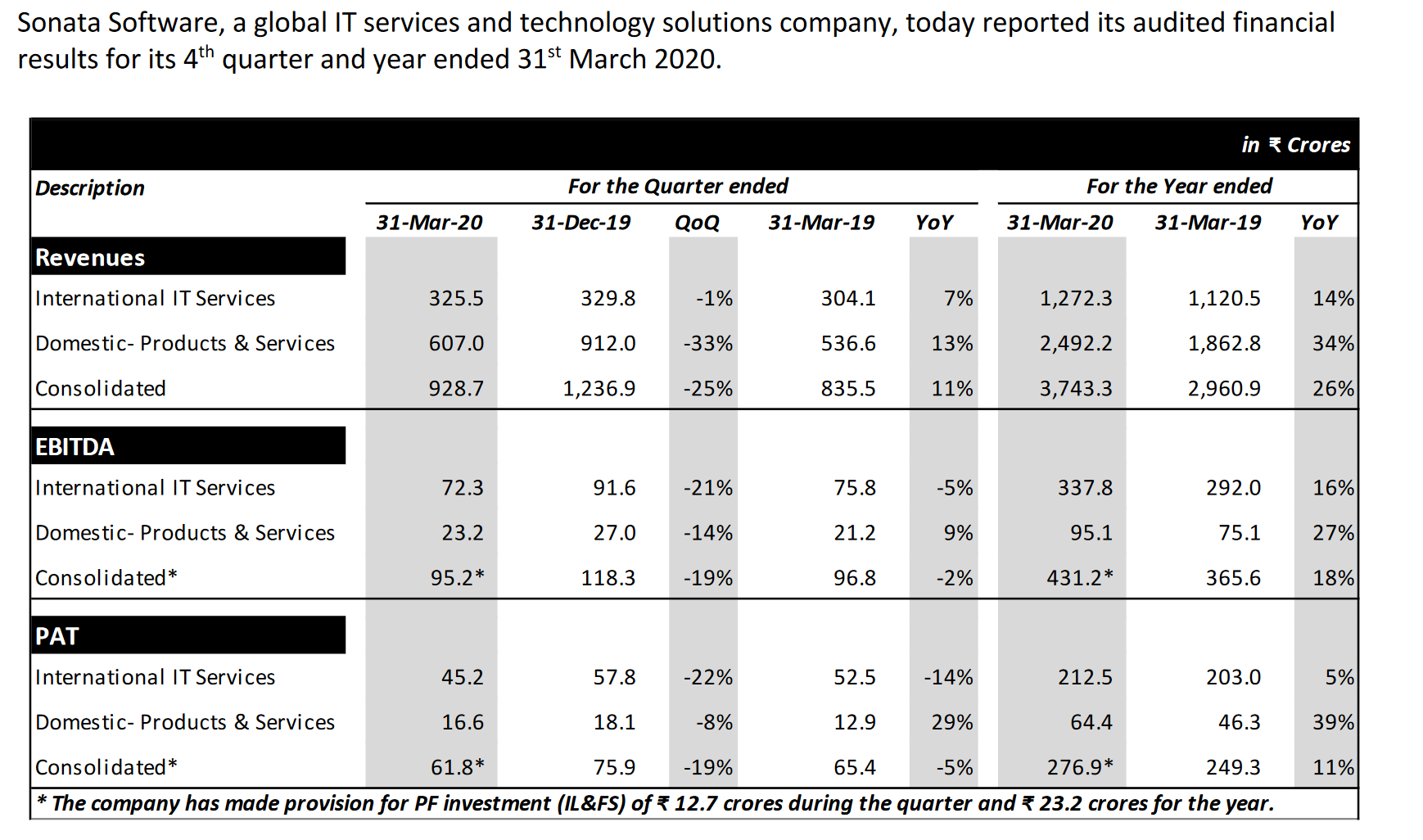

The company has reported a 16.7% growth in EPS for 9 months y-o-y. A large transaction in domestic business resulted in an impressive surge in revenues for Q3 (46% y-o-y growth). While the margins came in a tad lower, overall another quarter of stellar result.

Regards

SJ

Dear investors

I Was looking at this company and found that the trade receivables equals reserves.

Could anybody enlighten more on this.

Disclosure: not invested Just for reading purpose

Just wanted to understand utility of this ratio. What one infer from this ratio? I personally do not able to understand what reserve and receivable has to do with business. I company like IRCTC with share premium also would have high reserve. There is no meaningful point I can infer from linking reserves and receivable in my limited understanding. Appreciate you can provide your perspective.

Sir

I was emphasising more on credit which is not being discussed in the forum. Highlighted by saying that it is close to the reserves of the company .

Nothing to infer.

They haven’t provisioned in their annual report.

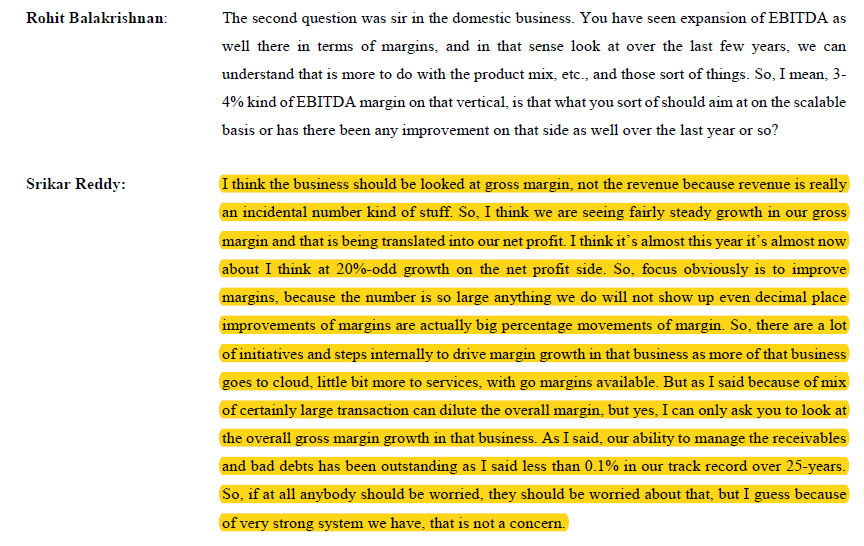

We can not look to Financial in isolation to business . Sonata has been working with Microsoft for more than decades in Indian market as distribution. The Indian business is low margin high volume business where they assist client in selling and implementing MS software in my undersanding. The offshore business is typical IT service business. Hence, receivable days appear very high when one compare sales margin. However, all these factor gets discounted in ROCE and Cashflow from operations. (Higher receivable days would mean limited free cash flow from operation and lower margin coupled with higher rotation of capital employed would result in higher ROCE).

On both these parameter, Sonata is performing well in my understanding. There would increase in receivable day when a large project in India is completed and revenue booked. However, same over a period of couple of quarters get normalised. This point is always highlighted by management in conference call. So while Indian MS business is low margin, it provide entry point to the company to show case its capability to clients.

https://www.screener.in/company/SONATSOFTW/consolidated/

Find enlcosed screener link for the financials. ROCE for Sonata in last 5 years is around 38-40% with positive cashflow from operations being positive in last 4 of 5 years. In FY19, the receivable days increased because of one major project being completed in booked.

Find enclosed extract from Q2FY20 Con call where management explain this point

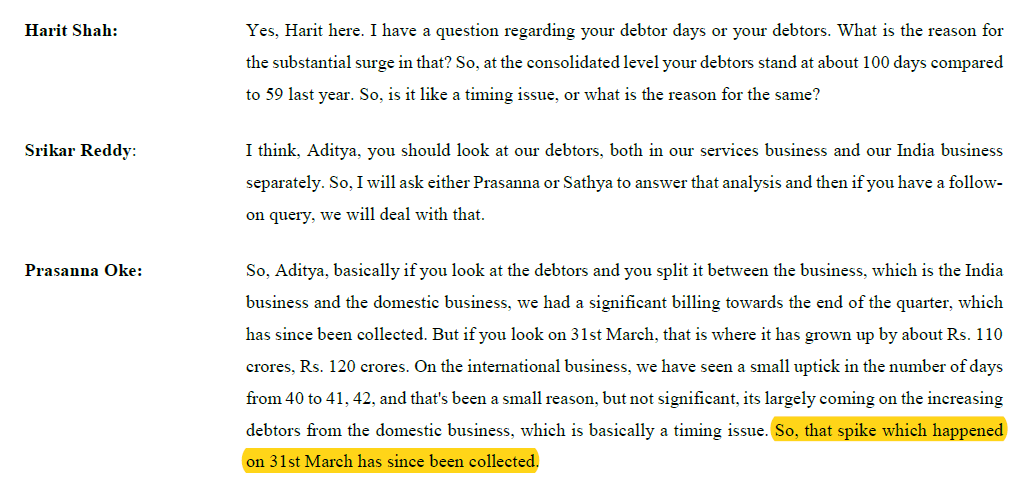

In Q4FY19 con call, there was query about increase in debtor days: I am enclosing portion for same:

The management said on call that they have collected same on May 31 2019 (being con call date). The next avaiable receivable figure on September 2019 Balancesheet also confirm same with decline in Receivable level to Rs 712 Cr as on Sep 30 2019 from Rs 811 Cr as on March 31 2019 despite growth in sales.

Thanks for bringing out important aspect of increase in receivable day in 31 March 2019. But I find no relationship between Increase in receivable day with reserve. Also, we also need to understand financials in context of business wherever possible. ROCE and Cashflow from operations are key parameter for me evaluate the company. Sonata has performed reasonably on both these parameter in past in my opinion (with ROCE around 35% and positive cashflow from operation along with higher dividend distribution).

Discl: Among my top 5 investment position, my view may be biased, not a SEBI registered investment advisor, it is not recommnedation, investor shall do his/her own due diligence before invsting.

I am not sure because

a) Account receivables has been growing at a higher pace since last year

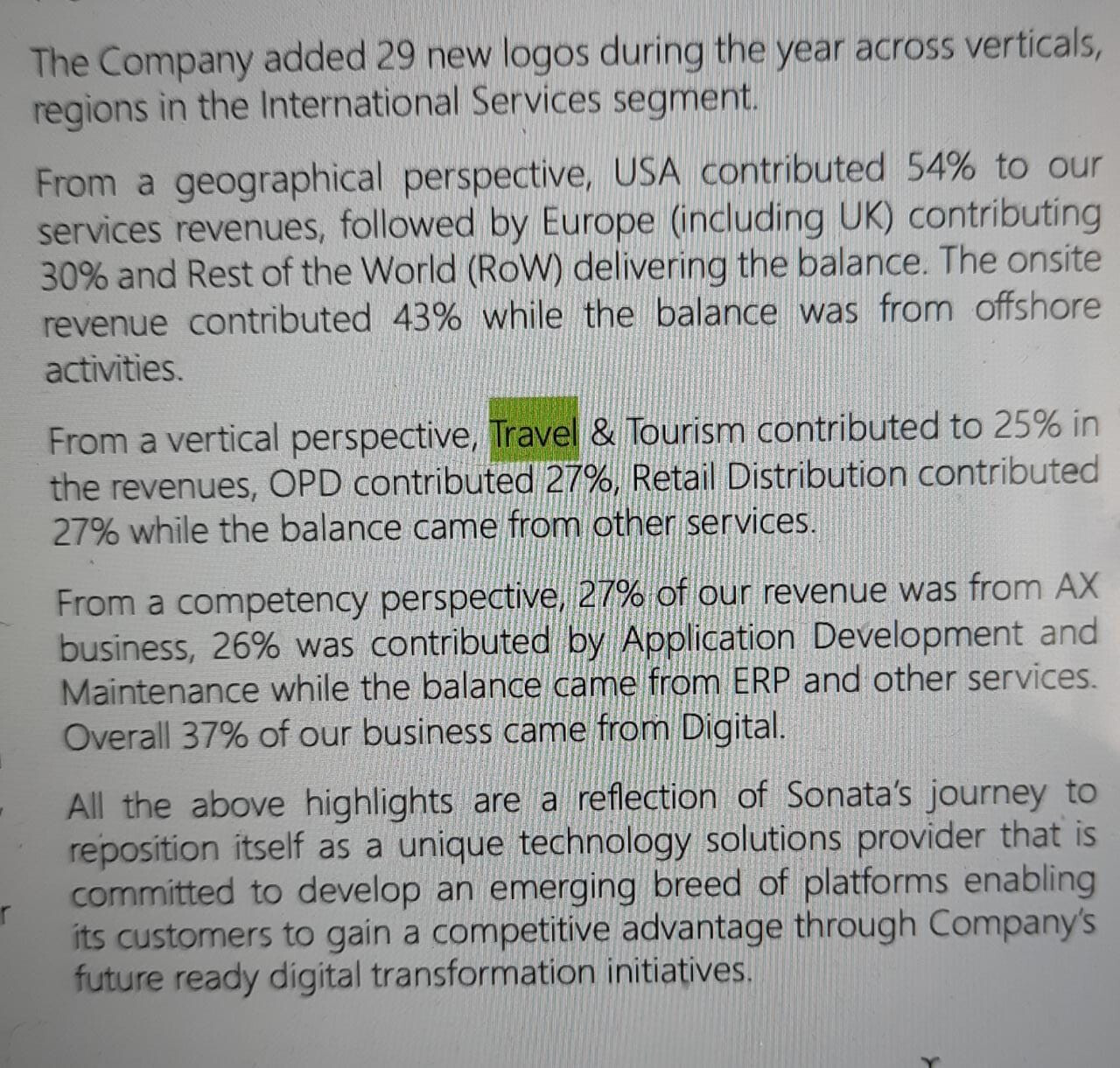

b) 1/3rd of their revenues come from travel and tourism vertical

Better to hear what the management has to say on the recent events and how they explain the increasing trend of account receivables.

Due to the COVID-19 situation one of our large clients had to temporarily suspend their operations thus affecting a majority of our services to them. We believe this will in the immediate future have a significant negative impact on our profits by up to 40%. Currently we expect this to affect our Q1 and Q2 performance for FY 21.

https://www.equitybulls.com/admin/news2006/news_det.asp?id=264831

Thanks for sharing Saumya. Despite this, the stock is on an upswing. Looks like they had an analyst meet and management said things that inspired confidence. We retail investors will have to wait to know. ![]()

https://www.bseindia.com/xml-data/corpfiling/AttachLive/93caf181-b13b-4205-bfe0-91ee61b4544c.pdf

Results look Good!

The above numbers look ok.

Company has exposure to the travel and retail segments,will need to watch how things pan out over the next couple of quarters.

I have uploaded the recorder call to youtube

Sonata Software is an IT solutions company primrily in travel & tourism and product engineering domain. They have been resellers of Microsoft and IBM tools for a while. The co. is owned by Rahejas and Ghias. In 2010 there were news of promoters wanting to exit the business and HCL, others evincing interest.

They have had bad FY12 and H1 FY13 numbers due to issues in TUI Infotech, a company they had acquired in 2006 in Germany. Last year they sold this off and booked losses for this, this was not actual cash flow.

Currently the company has cash of 172 cr. (mgmt conservatively indicates this to 140 cr adjusting for working capital).

The company seems to be turning around and has done some new tie ups with Oracle Axalytics, Tibco. Will be an interesting play as the stock had been beaten down considerably when it was reporting losses.

Hemedra Kothari recently picked up stake from Bhupathi investments. Bhupathi investment has had some pledge and has been reducing stake for a while some of which earlier have been picked by Rahejas.

There were also a few resignations of top management but this also now seems to be inline with Srikar Reddy at helm, he also has more than a percent share.

Numbers:

Mcap: 261 cr.

Cash: 172 cr.

Qtly

Dec-12 Sep-12 Jun-12 Mar-12 Dec-11 Sep-11 Jun-11 Mar-11

Sales 396.95 380.35 404.57 319.47 411 390.06 339.52 326.31

NP 8.64 (26.00) (40.65) (22.36) (12.68) 12.07 5.64 25.71

EPS 0.82 – -- – -- 1.15 0.54 2.45

Yearly

FY08 FY09 FY10 FY11 FY12

ROCE 36.23 40.09 32.75 24.58 0.72

RONW 35.44 32.11 26.83 23.16 -4.3

Sales 1,468.29 1,593.12 1,402.54 1,406.41 1,607.82

NP 58.52 76.57 79.88 85.61 -2.59

EPS 5.38 7.02 7.31 7.81 0

Dividend(%) 110 150 170 200 75

A quick glance and found bunch of issues:-

1). From Mar’08, they have a flat Sale of 1400 odd crore

2). For a company with such high cash, why they have debt. Ideally they should be having 0 debt

3). Promoter stake is reducing slowly. If promoter don’t believe in the future of company (that too with near complete information on it), why should I believe in the future of the company with substantially less info on the business/company.

The only silver lining that I could see here is the possibility of NP reaching 80cr odd mark in future. At a PE of 4 Mcap can go upto 320-470cr (470 after adding 150cr cash component), which is 15-70% higher than CMP. And this will happen only if they reach to their old profitability level.

Some issue in posting, another thread got created. Admin pls. remove the other one if possible.

1). They had acquired TUI Infotech and I guess they have been faced with issues on that one and hence unable to grow. Before that there growth was decent.

Even with flat revenues if they are able to increase margins that should do well for these guys. Before acquiring TUI their margins had been 15%+ which had declined with this acquistion. The management has indicated that they will be able to up the margins to 17-18% in a couple of quarters. The focus on domestic business also would be get margins up instead of revenues.

Also there are new COEs for Oracle exalytics, TIBCO which have come up. They have opened in Qatar which as a country is growing at 17-18% pa. Management had resigned last year which also has stabilised now.

I think they will turnaround fast and the valuations should be better next year.

2). The debt is for working capital which typically a few IT cos. do engage in as their cash might be tied up elsewhere in ST/LT instruments. This is common practice.

3). Promoters have indicated interest in exitting and a couple of years back HCL/CDS had evaluated buying them. They have big group and diversified interests. Rahejas is a well known group and they have increased stake. Bhupathi investments which belongs to Ghias also have diversified business interests and they are in pressure in their textile business and hence having been selling.

Also, they have a few cases on tax which are detailed in the AR. Last year they had got a refund on that, these are significant amounts in some cases thought can’t be used to value.

The company has come out with a solid set of results and is available at a cheap p/e of around 10 and a very good dividend yield

YoY sales growth is at 26%

YoY ebita growth at 19%

PAT growth at 11%

has a healthy ROCE of 38%

The only key negative I see here is low promoter holding and high retail holding

added to watchlist and considering investing

The key issue for Sonata is large exposure to Aviation, Travel, Tourism and Retail, sectors that have been worst hit by Covid. While their IP business has been doing really well. They gave out a pessimistic outlook the Covid impact to the exchanges (one of the first few companies to do so). They might have been conservative or may have overestimated the impact, but they will have a tough time even if one of their large client goes out of business. But I like the quality of management though.

Disc: Exited this month

Regards

SJ

Can someone help me understand why would someone use a website built using Sonata’s Rezopia for travel and tour packages? For e.g I could find that the below 2 websites are built on top of the Rezopia platform.

https://www.sunnylandtours.com/

https://discoverbranson.com/

Both of these seem to be small tour operators in their local area. I would assume that Sonata would try to acquire similar small businesses and help them build a digital platform using Rezopia.

Is Rezopia the flagship product of Sonata in their Travel & Leisure Vertical? If not, please help me identify the product. With so many big players like TripAdvisor, Air B&B, Expedia etc, how much of a growth can we expect from their small tour companies down the line?

EDIT: This article provides a lot of comfort to most of the queries I had w.r.t the role of tour operators in the tourism industry in the future - https://www.tourwriter.com/travel-software-blog/2018-tourism-stats/

Disc: Not invested. But interested if price is down to 10 times earnings.

It has doubled from pre-covid level, maintained good profit considering 25% business is from Tourism and Travel segment. This vertical must have bottomed-out, should we expect better /back to normal margin of 11% (ref FY19 results), it is trading at ~20-22 PE (normalized).

Find enclosed interesting article on Sonata in Fortune India July 2021 issue.