My only argument against any EV play is this - Arrival of EVs will not expand size of the market (number of vehicles sold in the market) , it will only replace current IC engine driven vehicles with electric motor /battery operated vehicles. So volume increase will happen only for those companies which are not supplying to any current IC engine vehicles and will get large business once EVs become mainstream. For the rest, it will be replacement of current product with a new EV product (except may be higher price and better margins for EV products) So I believe its more market fancy than anything. EVs will become mainstream like current IC engine driven 2W/3W/4W in next 10-15 years and will squeeze their component suppliers for every single rupee as current vehicle makers do. So OEM component suppliers would be always a thin margin business (unless one has patented technology like Bosch or has large lucrative aftermarket business like tire companies.)

A few views of my own. I agree that the overall market is actually a replacement marker for ICE.

But , unlike the traditional ICE engine,

(1) As you already pointed, EV drive trains need additional technical know-how and hence there is more margin/product . Fundamentally, gear assemblies need to cater to instant high-torque from the battery . Granted every one will catch up over the next years.By being a early mover Sona does have the advantage as they lock in customers very early on, work with engineering teams in OEMs, relationships are built and trust-confidence for subsequent generation products is established.

(2) The scope for Sona to increase their revenue per vehicle is larger. From gear units, differential gears, which is the their base platform, they are already expanding into differential assemblies invertors, motors, motor control units, software across both EV and Hybrids.

I cant put a number on the revenue increase / per vehicle possibility with gear units as the baseline. But I do feel this is quite large.

And they do have the vision of an integrated system with mix and match options for OEMs to choose.

As the CEO said in previous quarter concall, he doesnt know what the OEMs will produce when companies like Sona go up value chain.

The other dimensions to this are

- the possibility of OEMs taking over Sona.

- Sona taking over an OEM

I potentially see one of above happening if Sona maintains its growth rate.

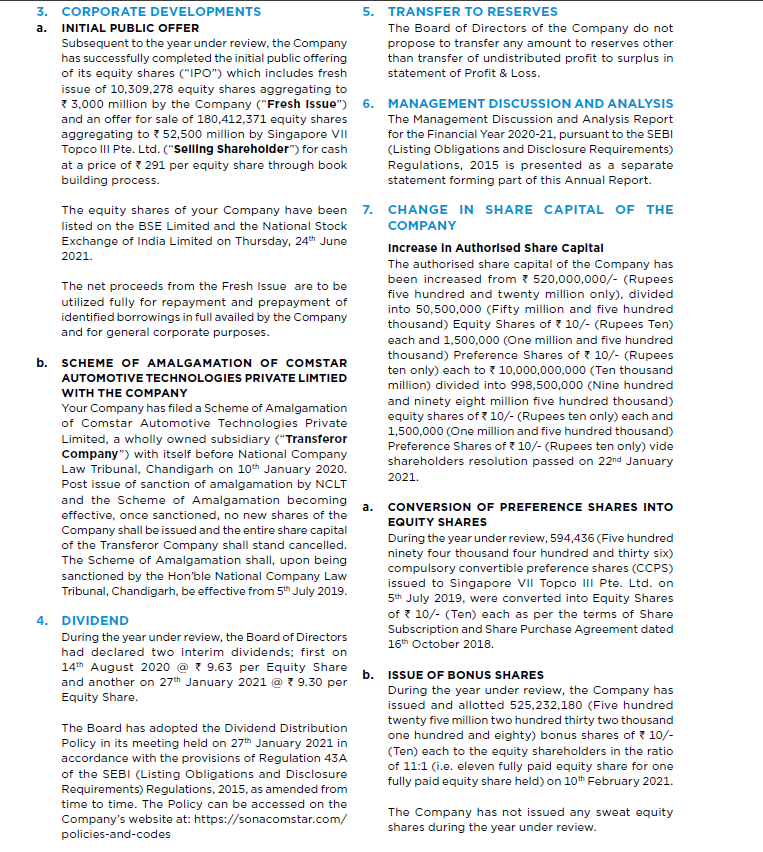

Wanted to highlight these very important equity dilution processes. Hope we haven’t forgotten this in light of such nosebleed valuations. Personally, such business equity dilution is an important event for me whether it’s Pre-IPO / Post-IPO.

Excerpt from AR 21: page 31

Hello Ish, Were you able to verify this?  Thanks!

Thanks!

Normally IPO / public listing will happen by way of fresh issue of shares or OFS.

So nothing wrong in this case as the company has done by way of both.

There are couple of positive points

- Funds are used to repay debt

- Conversation of pref shares into equity.

Mystery continues. This article claims Tesla is Sona’s 3rd largest customer.

In FY21 largest customers was Ford. followed by Volkswagen, followed by Tesla.

13.1% of FY21 sales was from Tesla out of total 14% from BEVs.

In 1HFY22 21-22% sales was from BEV. Tesla contribution is not known but is definitely more than that in FY21. Tesla might have been 2nd largest customer also.

Could you please share the source of this information please?

Download the red herring prospectus. See the business section. It clearly gives a split of revenues yearwise and clientwise. You need to read between the lines.

See page 180

The article confirms that they have information from multiple industry sources about a confidential supply agreement with Tesla.

which article, can u share again ?

It is an article by Ken posted by Aditya in the thread above.

")

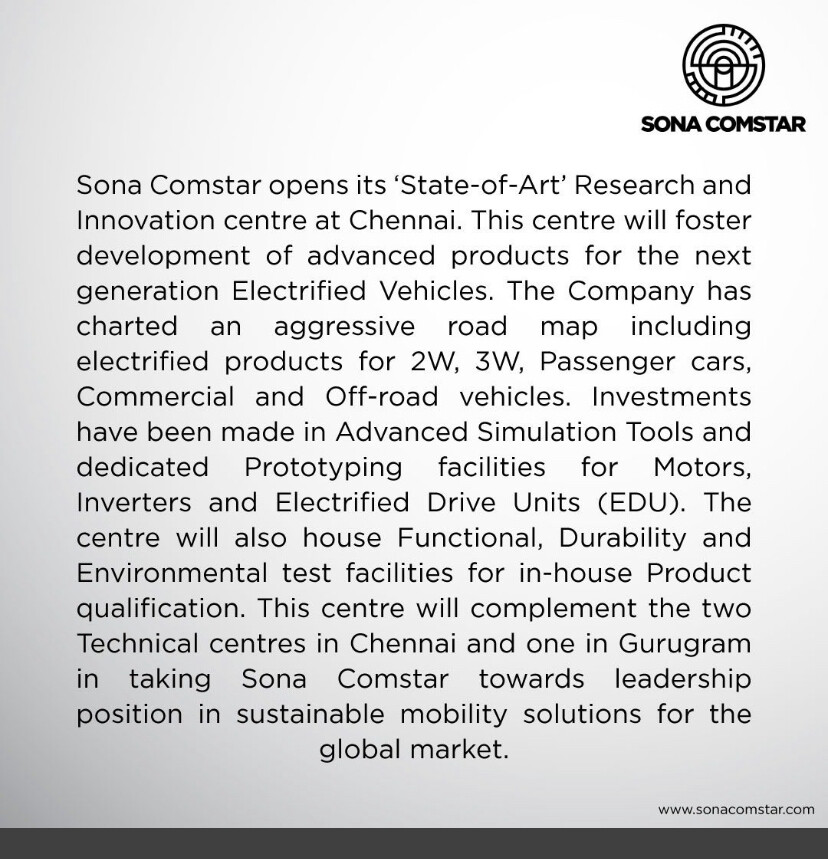

Excellent video on plant visit and management discussions with Sona Comstar

This gives the state of art facility view and future projects.

The management also informed about adding new clients recently.

Big news on EV