A lot has been written and said about the expected growth of EVs across the world.

I came across Sona Comstar recently and really liked the impressive Order Book Growth they have shown recently and their exposure to the EV space.

Sona BLW is an Auto ancillary company that has two established businesses in the form of Bevel Gears and Motors that are an integral part of EV’s & Hybrid vehicles.The Company is likely to be one of the biggest beneficiary of transition towards to BEV (Battery Electric Vehicle) in the coming years. Market to expand to 5x in the next 5 years:

Brief History (Source IDBI Capital Brokerage Report)

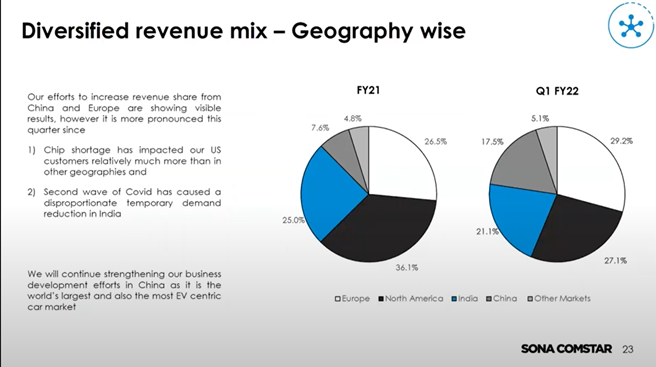

SONA is one of India’s leading auto ancillary Company involved in design, manufacture and supply of differential assemblies, differential gears, conventional and micro hybrid starter motors, BSG systems, EV traction motors (BLDC and PMSM) and motor control unit to automotive OEMs across US, Europe, India and China for both electrified and non-electrified powertrain segment.

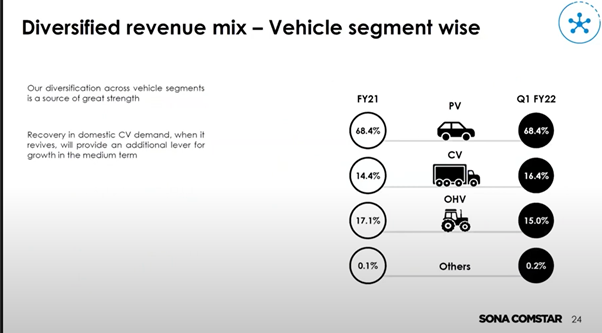

The company has nine manufacturing and assembly facilities across India, China, Mexico and USA. In India the company has six manufacturing facilities from where it supplies its products to six out of top ten global PV OEMs, three out of top ten global CV OEMs and seven out of the top eight global tractors OEMs by volume according to Ricardo Report.

The company is among the top ten players globally for the supply of bevel gears to PVs, CVs and tractors. The company is also among the top 10 players in starter motors supplies to PV.

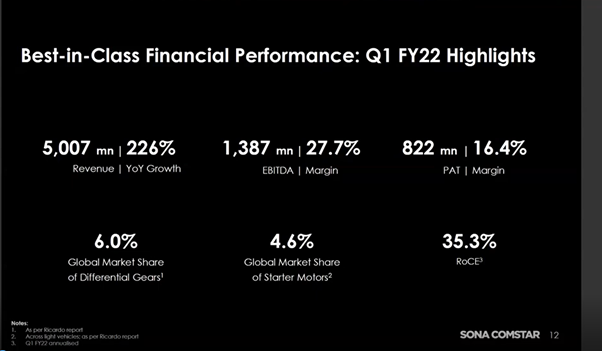

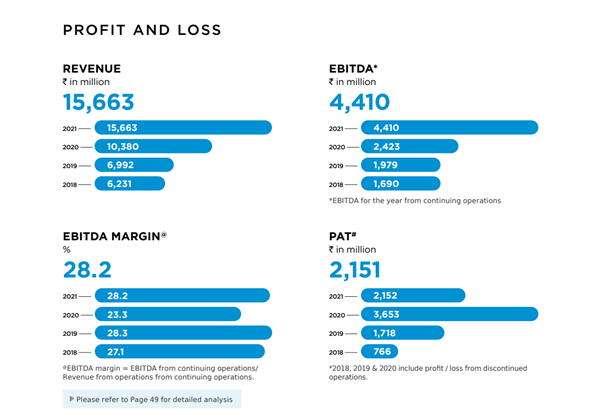

Quick Financials over last 3 years

Great Sales Growth : of 1500+ Cr from 700 Cr

OPM maintained over 23% over 3years

Tax paying company

Fixed Asset increased from 291 Cr to 1200+ Cr

Recently listed and hence not a great deal of information available

A very good video from Mr. Vivek Vikram Singh, MD and Group CEO helps gives some insight of how technology is helping the company to create a small niche for itself

What excites me are the following :

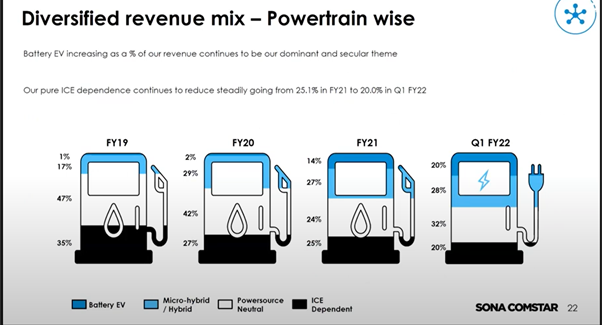

14000 Cr Orderbook and out of which 8000 Cr is in EV space and 6000 Cr in the ICE space

Its FY Revenue in 2021 is around 1500 Cr and the latest Q1 shows Revenue of around 500 Cr so a good growth showed and a decent Orderbook means that it has a good runway for growth

In Q3: around 100 Cr (20% came directly from EV), 20% from ICE, and 60% from Hybrid and Powersource Neutral.

Also they are trying to develop a new Powertrain system for 2W/3W EVs to drive motor without permanent magnets with JV from Israel based company

As per AR

Impressive ROE, ROCE of around 36% and 35%

Capex of 218.9 Cr and Free cashflow of 142.7 Cr

long-term rating to AA- and total debt of 338.7 Cr as of FY 21

Total R&D spend for Fiscal 21 was 5.8 % of our revenue

Started to manufacture and supply BLDC motors for 2V, business is small as of now but the incentives from Central and State Governments

coupled with the necessary regulatory push are expected to bring 2 wheeler EV market in India to life over the next few years as per mgmt

Things that worry me and where I need some guidance from the members

Contingent Liabilities of 124 Cr in the books - lot of these are tax claims but is this a cause for concern.

Trade Receivable of 417 Cr or 27%, I can understand that Revenues have grown by 50% over last year and this is expected. Still, Receivable increased from 23% to 27%. Anyone aware of any steps company is taking in this direction

They have a DSO of 97 days and again this has increased from 62 days, very much related to the above point

The biggest concern is that their consolidated Net Profit over the last 3 years is 748 Cr but their CFFO is around 184 Cr. Typically this is a red flag. At the same time, I have seen that their NFA has increased from 304 Cr to 1124 Cr (almost by 820 Crs) . Any guidance here will be great

I understand that from the current PE of the company this looks very expensive but looking at the growth this looks like an exciting prospect and any guidance will be greatly appreciated

Disclaimer: Currently in research mode and planning to take a tracking position soon. Pls do your own research before taking any call.

This involves R&D at Sonacom end. In his talk on Motilal Oswal Global last week Vikram said that this is a BINARY. Can be zero or a singular success and if it succeeds it will be a game changer. Also that the R&D spend is higher than normal in the last fiscal. It will average 3-4 % going forward.

I think in one of the recent interviews the company denied that they are supplying to Tesla

To me, the more important point is whether the company can walk the talk in terms of being a technology leader across the world in this space.

Also they have a robust Order book and that should translate into Revenue Growth QoQ. I will be watching their Quarterly numbers very closely to build conviction

Yeah, firstly, I think, let us be clear that this is an R&D project. So currently this

motor is not in existence. We are actually co-developing this product along

with the Israeli partner, they have competencies in control algorithm,

hardware, software. We have competencies and expertise in motor design

and manufacture, we are coming together to develop this

In terms of efficiency and

performance, we have set certain benchmarks, certain targets to achieve.

We hope that we achieve them, they will be quite high. But at this moment

I cannot say what is the kind of efficiency, what is the kind of performance

we will get because there’s a product which is going to be developed

All said and done, one must be pragmatic about R&D. It will be a gamechanger if it happens.

Still a long way to go. Proof of concept is one thing. Ability to translate that into a production line, think about servicing , safety etc are additional downstream challenges. Still very early days. I’ll give it two to three years before anything tangible comes out of it.Such is nature of R&D.

Single largest customer business : within 18 months , to come down to 50%

7 customers

FX impact in the Q1FY22

19million positive.

Improvement in margins in Q1FY22

Largely due to foreign business

EBITDA margin expected to be around 27% in coming quarters

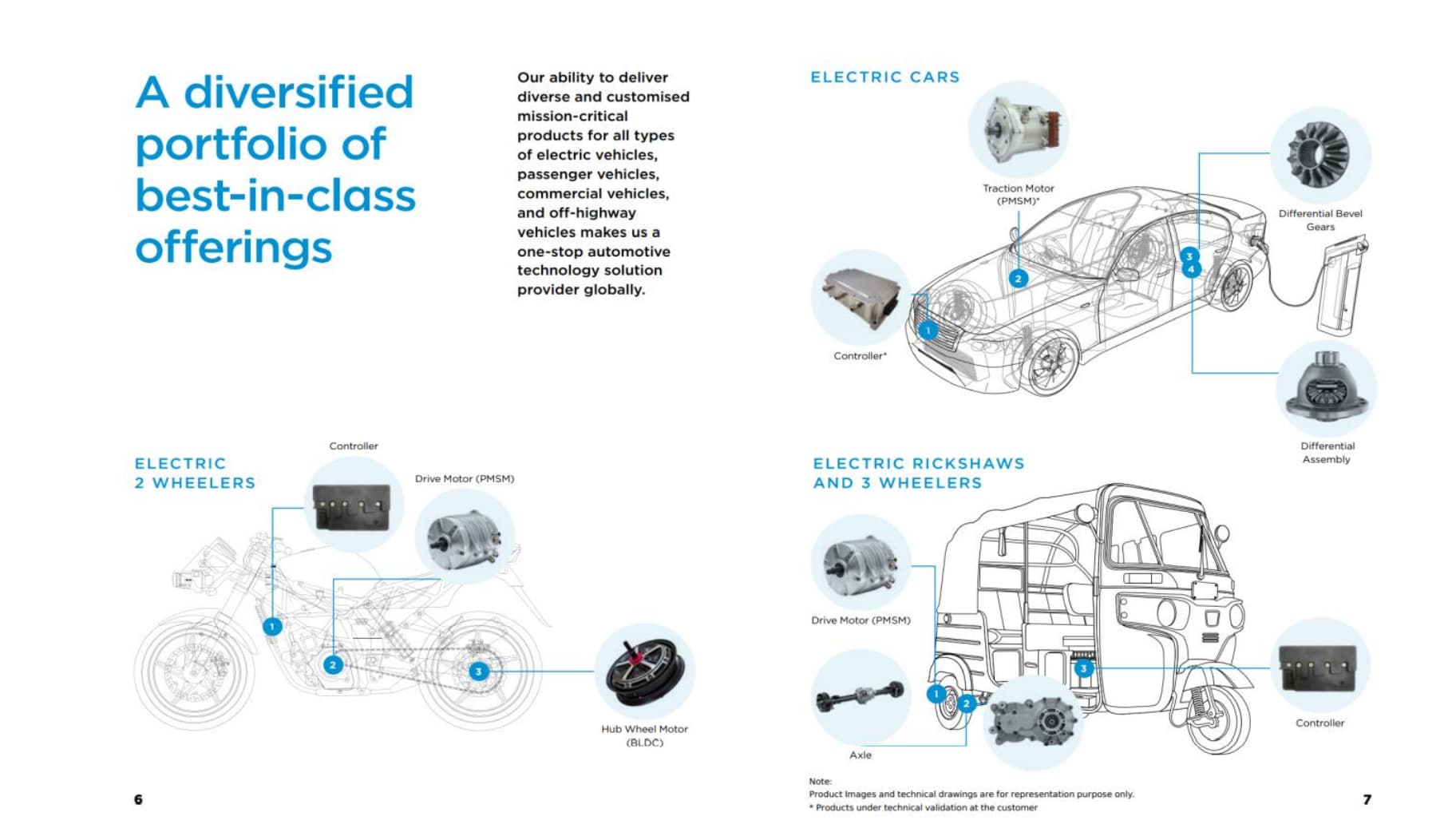

Holy grail is integrated drive train ( motor , controller, axle and differential gear)

** * About 7 pieces in above**

** * Can provide full set or individual (lego) pieces**

** * Will cater to individual OEM needs or requirements**

** * Every OEM has unique programs**

** * Not too many OEMs will be interested in integrated drive train (‘”what else would the OEM do if he does not have control over the drive train?”)**

Magnetless motor

Revolutionary product

Reduces large cost of BLDC motor

In R&D

Israeli input – control algorithm, hardware , software

Sona – design and manufacture

95% magnets from China

Price fluctuation

Large portion of price

Efficiency and performance

Targets are set but too early to tell

*** Net order book**

** * 2000 cr annualized revenue for next 10 years**

** * 14000 cr over next 10 years is over and above the 2000cr annualized revenue**

Commodity price pass through

Steel is main contributor

Copper completely passed through

Domestic biz

1 month of delay and passed to customer

International biz

6 month cycle

Average taken for 6 months and passed through for next cycle

Net – net . no loss seen because of commodity

Next quarters business guidance

Guidance in spite of chip shortage

Assumes problem exists

*** Customer stickiness**

** * Never lost a customer**

** * 13 of 15 top customers have been with Sona BLW for 15 yrs**

** * Lot of time, resources and investment from OEM engineering department & Sona staff for part development to customize for product. Enormous shift required by customer to go away from Sona and there will be product delays if they do.**

** * Example: EU EV customer**

** * Talks in 2019**

** * Development in 2020**

** * Production in 2022**

** * Average duration for product maturity and production : 2-4 years**

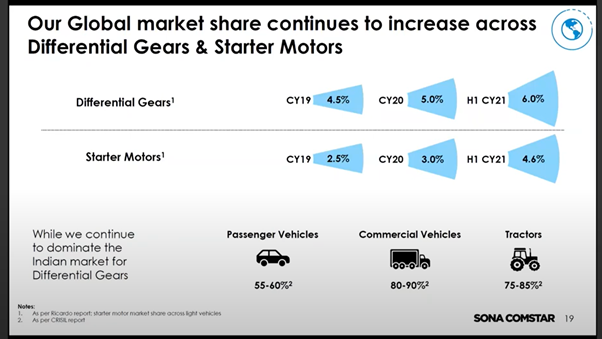

Driveline

Large share in India

7-8% in NA market

Plan to grow in EU, China

6% global share

Motor business

Large share in EU market

Strategy to grow in NAmarkets

4.6% global share

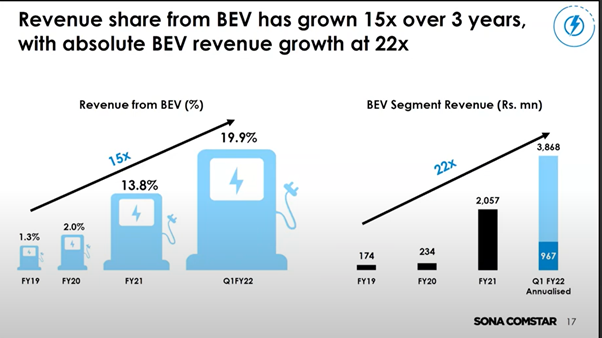

EV breakdown

1 PHEV program

Mostly BEV

22 years EBITDA margin ( 25- 36%)

Growth estimate and risks

Not giving guidance

Covid and Chip shortage are known risks

Even in worst quarter of last year, we did not go negative in profit.

This paradigm raises the plausibility of success. Design is within the innovation and design parameters by the Israel company. Like CDMO model in Pharma, innovator outsourcing one part of drug discovery and the development + manufacturing.

Sona’s primary aim is to get strategic independence from Chinese permanent magnets. The magnets are used in the PMSM and BLDC motors (see pic). With a critical component outside of their control, they feel vulnerable and hence magnetless motors is being pursued by Sona.

It is great to see the company thinking big and in this direction. However R&D is fraught with risks and mentioned earlier, it is either 0 or a 1. Their CEO Vikram Vivek mentioned as much.

We have to wait and see.

I have taken a tracking position on the stock so far…

Am not making any buy or sell recommendation.

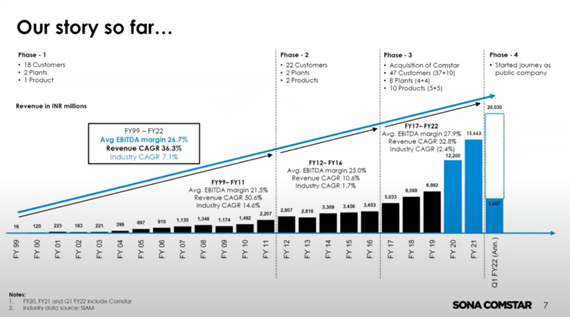

Below are some snapshots from the concall and some charts I prepared. This was to understand that company from a overall business point of view and to understand management intent historically.

Above shows 3 main stages of the company. They start with 1 product ( differential gears ) and then over a decade , get to 10 different products for both ICE and EV vehicles. This decade to reach 10 products and to make components for EV vehicles shows management roadmap , backing it up with R&D and getting the products to market. Mind you, they are dealing with OEM Engg teams and it takes 2-4 years from initial engagement and OEM signoff to ramp up production.

Good sign in my view.

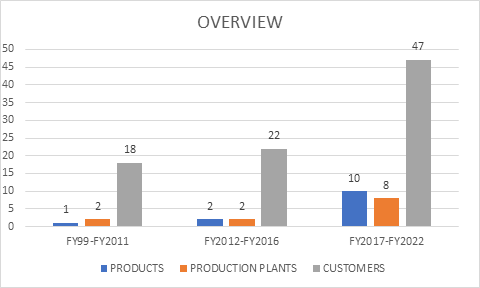

Above is just graphical representation of timelines. products and customers. Seems realistic and believable especially considering time it takes to get 1 product to production with customer.

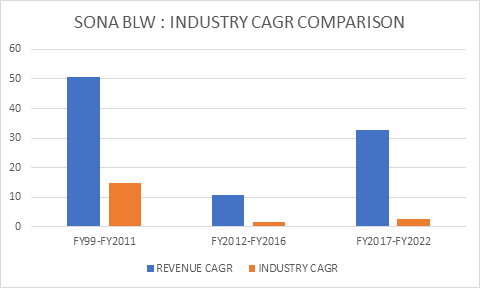

Historical Industry CAGR comparison . The FY2017-22 is interesting even as the industry isnt growing as much. They seemed to have grown a scorching pace with the products.

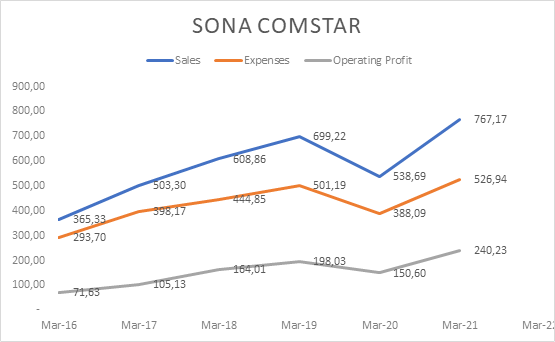

Post covid recovery is very strong.

Wanted to see EBITDA margin . Found it in annual report: barring 2020, generally consistent

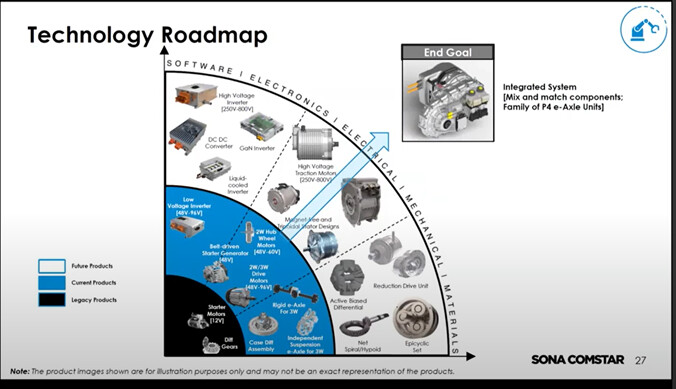

Technology: History & Roadmap of Sona Comstar

At the outset , and at the cost of repeating myself, I have to say that I am particularly impressed with Sona’s history of product development (See my earlier post). Two other points which were noteworthy during the Q1FY22 Concall were:

Their CEO stating that R&D is fraught with risks and the magnetless motor could come to naught.

Their CTO, stating that magnetless motor R&D will take time and a quarter is a short interval to report updates.

You can see that these gentlemen are level headed , aren’t fly-by-night operators, and give realistic guidance.

With regards to product roadmap, Sona shared their plans in the Concall. Snapshot below.

Their CTO mentioned that they are transitioning from the light blue to white area this year.

As for their technology history, I gathered the following from the Annual report

In the driveline division,

our main product is differential bevel gears. We were the first company in India to manufacture gears using the precision forming process. Our material yield is much higher than the gears manufactured using traditional methods because we form the gear teeth and do not cut them from a blank. The internal grain flow of formed gears is aligned with the tooth profile, making these teeth far superior to the teeth of machined gears. We have developed an in-house proprietary gear design software that helps us create gear tooth profiles optimised for specific customer needs. Our over two decades of experience has resulted in several improvements spanning the processes of forging, machining, heat treatment, and surface treatment**

Electric division :

We are primarily engaged in the manufacturing of starter motors for light, passenger, and commercial vehicles. We share long-standing relationships with some of the leading OEMs that have manufacturing plants and consumers worldwide. Our high-performance starter motors withstand extreme temperature conditions experienced in Europe and North America. Given the recent shift towards the electrification of drivetrain, we have focused our R&D efforts towards developing drive motors and controllers for different types of hybrid and electric vehicles. A significant component of these efforts has been in developing the hardware and software for the controllers. We have invested heavily in enabling algorithms, cybersecurity, On-Board Diagnostics, Over-The-Air updates, and other capabilities

We can summarize this as grounds up R&D and building capabilities over many years.

Nice info overall…But I am just curious as to how do they get an orderbook for 10 years, specially when this EV cars industry is so dynamic at this stage and so many players are still experimenting with various technologies.