Have started researching on this company . Mahle Group has already developed and dispatched sample of a similar tech somewhere in May this year . The Mahle group is touting this tech to be used from PV to CV and expects mass production by end of 2023

However one stark difference is that the technology of Mahle Group is mentioned not to be efficient in E-bikes space whereas what i could get from my understanding what Sona Comstar would be manufacturing would be beneficial to 2 and 3 wheelers.

Also reading this article I guess all EV manufacturers want to remove magnet from their motors and remove their dependency on China

Update 2

Another fun fact during research it does seem Tesla to be the mysterious Global EV which is mentioned in the IPO Draft Prospectus and in a few of the reports lastly mentioned by the article on Ken .

Reading the NSE clarification circular the precise words never say anything relating to they dont deal with Tesla . In fact it pretty clearly mentions that it is not in discussion with Tesla for its India plans only and never clarifies on their existing relationship . As I am late onboard if any member can share a documented proof by management that TESLA is not one of its customers then it may still make me reconsider my thought

In this connection, we would like to state that the Company is not engaged into any

discussion with respect to supply of components to Tesla for its India plan. The Company is

not aware of the source of this news information.

Also cementing this thought is this old 2018 article which clearly states the 3 companies and the parts which they supply ( Which I guess the ET Reporters might have picked up for their spicy article on Tesla Indian Suppliers )

Q3 saw some decline in sales on account of the ~23% decrease in car sell in EU and US during Q3. Handsome addition to the order book which is now 11 times the FY21 sales.

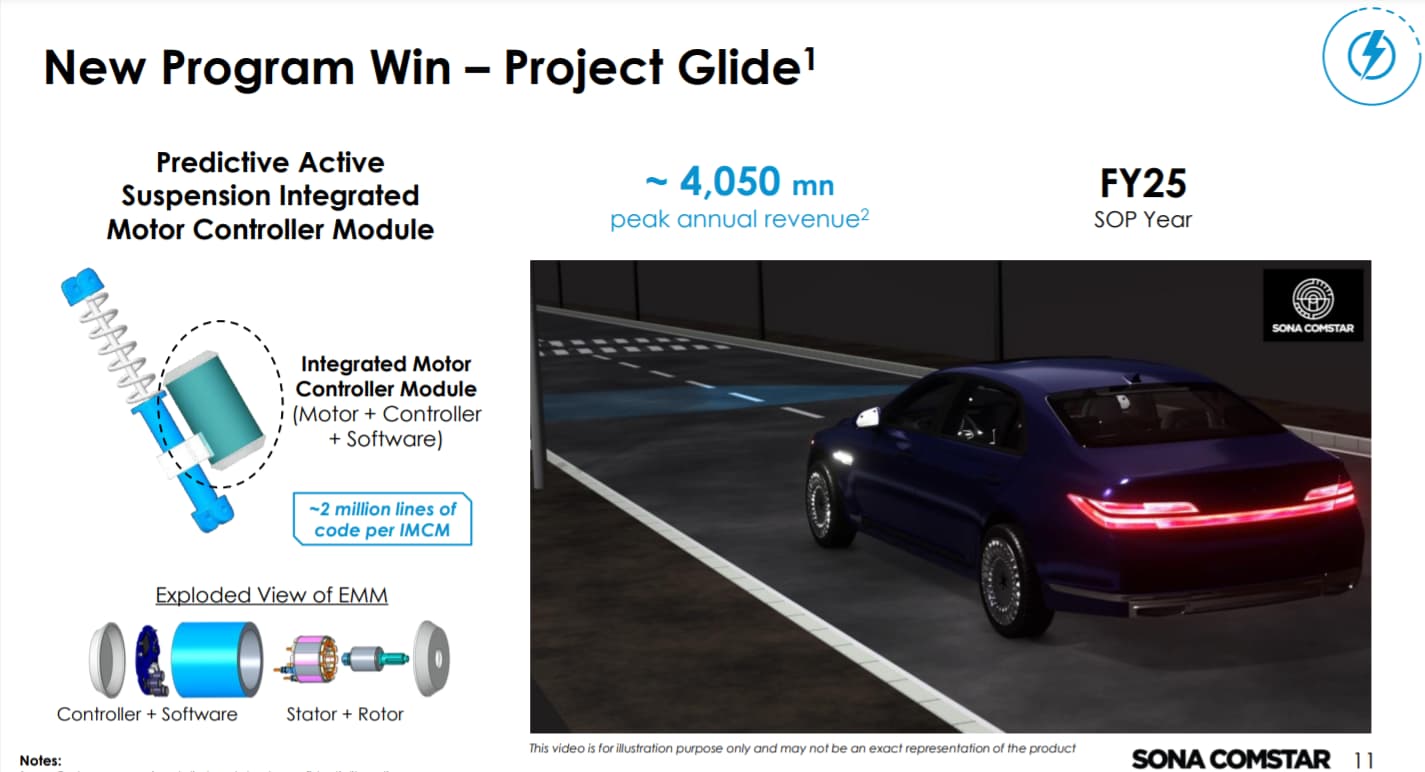

Sona Comstar is making a completely new product - IMCM (Integrated Motor Control module) . This is significant because this single product for a single customer alone can add 400 crores revenue per year - CEO

This new product seems very very exciting to me. The layman term for IMCM will be “voluntary motor control software” . Your code which is embedded in hardware directs the motion(multiple aspects of it actually). The number of lines of code may directly co-relate with the complexity of functionalities being handled. It could be worth watching how they plan to scale this up(huge opportunity here), maintain zero defect run rate(as lines increase, so do chances of bugs) and how do their peers respond to it( these peers can be customer internal teams too).

The working of this tech is clearly presented here

Audi has been using this tech i guess somewhere from 2019 and as stated in the con call this active suspension is for high end luxury cars .

As shown in Audi video the system in itself will be heavy and would require complex systems which I guess will still be some 10 15 years away from our regular EV . Anyways suspensions are already shock absorbers and this tech is just taking absorbing shocks to next level .

However what fascinates me about this is how innovative and forward thinking this company has become . I would rethink of categorizing it as an auto ancillary due to their way of working and innovating which i guess is their moat .

This company is in the race in terms of magnet less motors , now pulls this rabbit out of the hat out of nowhere. And getting an order from a luxury car maker from EU for such an innovative product speaks volume about how the company has been able to instill trust and I guess this is the reason for them to have maintained their margin .

I see the hunger and aggressiveness in the management. They seem to be hustlers looking to take complete advantage of this changing EV landscape and become a global player .

However their statements we haven’t lost a customer till date and all I really don’t know how can one verify such tall claims . And with their rapid innovations and reducing focus on traditional starter motor i can vouch they will surely lose some customer in the future though how much it impacts their top line and bottom line is something to see.

Only time will tell whether the financials tell the same story like the management paints …

Two issues we have to understand to get a idea of the ICE decline impact.

breakdown of individual product contributions to revenue. E.g. how much does starter motors (ICE) contribute to revenue

what products likely to be affected by switch to Hybrid and Pure EV

On (1) , the company does not divulge the data

On (2) , apart from starter motors , every other Sona product is unaffected. (correct me if I am wrong) .

Disclosure: 3.5% portfolio allocation. Biased

PS>What I found Interesting in this Quarters report was in page 19 :

“Motors for Bots and Industrial automation” . That is a digression from the traditional Auto space.

The stock trades at P/E multiples of 120x FY22, 73.2 FY23 and 51.5 FY24 assuming EPS growth of 44% in FY22, 63% in FY23 and 42% in FY24. Very difficult to make money on a stock which is so expensive.

Remember this is not an internet stock, but an auto component company!

The game of judging a company purely on PE is something i have learnt the hard way .

Missed the bus on Dixon before the whole China thing purely thinking it was over priced even back then . Same story when Dmart listing

My current strategy is to ride the wave rather than miss it. The moat is that it is working on the entire drivetrain system which is heart of the EV . I guess they are playing at another league and thats why the premium which no one has . Also having huge order book over 60% of which is EV from International cliente of repute is no mean feat.

The scope for the company is huge and its better to ride it than miss it .

Valuations for such high growth companies always look stretched . I remember reports comparing D marts 2023 2025 PE in 2017 and saying it has upside potential . What will matter more is whether the company delivers on its promises .

Also in such cases of absurd PE i tend to check on the investments by DIIS / FIIS & MFs to console myself that im not alone in this frenzy . Also during the Zomato and recent IPO fall i found that it still stood its ground vis a vis other players.

Even though i tend to keep a neutral view my opinion can be biased but I am game on for any contradictory views which may help in building up the thread

Disc : Recently added forming around 3% of my portfolio

You give an example of Dmart, what else? Asian, Pidi?

On the other side, Infy & tech basket suffered in spite of high growth. The same is for the basket of FMCG, Infra, Japan index, Jocky and recently some mid-cap IT (however history is short - need to see).

I presume that 1-2 may be successful out of say 10 high-value stocks. To find that 1-2 seems difficult,

Its a brilliant company, with brilliant clientele and brilliant orderbook position. I agree with you 100% and wish I had invested in it at 400 levels. I put in an order at 330 levels and kept waiting. Don’t think that order will ever get executed

Having said that, the valuations at present are such that they bake in flawless management execution and topline growth quarter after quarter for the next 5 years at least. Needless to say, valuations don’t give any margin of safety to account for tail risks like an economic crisis, severe liquidity crunch, semiconductor crisis not getting resolved for 3 years etc. Therefore, the upside for new investors to get in at this point with a fresh position is quite limited. At best it can generate moderate CAGR returns, at worst it can give substantial losses. Only way to play this for a new investor would probably be a small portfolio position of 2-3% for moderate gains. But I suspect that investment will come with significant opportunity costs.

Why there is blood bath in the stock in the last few trading sessions ? After the Ukraine crisis fall in markets, all other stocks bounced back and Sona is in downward trend. Can someone share their insights on this ?

Not sure about all stocks bouncing back. If you look at the 2-4 weeks, most stocks were in a downward trend. To me, the broader market was in a state of correction anyway and the global geo-political scenario is only accelerating that correction. During the first major post covid recovery phase, all stocks reached very high valuations (chemicals, IT, big IPOs etc.) and now they are correcting to more reasonable levels. Personally, I think it is a good time to add quality stocks to your portfolio if you think they are trading at a good discount to their ATHs.

Disclaimer - I started investing only 4-5 months ago so please DO NOT consider this to be financial advice in anyway. Purely my personal opinion

Generally comparisons should be made across industry peers and not benchmarking with Nifty Indices or some other top stocks or other industries

Your comment made me curious to find out how its has performed vis a vis its other peers ( prices as of 4th March 2022 ( last 1 months stock price )

Sona BLW - Down 10.59%

Minda Industries - Down 18.45%

Motherson Sumi - Down 24.47 %

Sandhar Technologies Ltd - Down 12.65%

Disc : Invested in Sona BLW and Minda Industries from higher levels. This resistance in share price vis a vis its peers despite a not so good quarterly earnings is something to be aware off.

Also surprised by the resistance shown by Sandhar. Will need to deep dive into the same.

Good session with Mr Vivek to understand Background, frugality, low fixed cost construct (15%), Negative networth to journey of turnaround with $2B+ order book currently( 65% + EV) , one of true globally scale innovation success story

Another key takeaway - ambitions to Become components/ hardware only solutions to integrated hardware + software solutions player- 25 sw engineers currently, scaling to 50+ , they believe to have an edge to deliver better value than pure play software setups - essence being Software is a key differentiation for Auto components majors. Those who can, will stand apart.

Expensive valuations, sector headwinds in short term, took tracking position recently

Sona Comstar launches “Motor T” family of motors & controllers

‐ Next‐gen tech for best efficiency, Torque & Power density in 48V category in the world

‐ Motor T (HS) offers 14kW peak power under 10kg meant for high speed two wheelers

‐ Introducing our rare earth free 5kW peak Motor T‐REF

Sona Comstar’s ‘Motor T with optimised controller’, with next generation technology, has the highest

efficiency (96%), power and torque density in 48V category in the world.

Neodymium breaks easily, while ferrite is much more resistant and resists breakage . Both magnets retain their magnetic force over time, and there is no reason to fear losing the magnetism naturally. However, ferrite magnets can be demagnetized by the influence of stronger neodymium magnets.