Sona BLW is a direct beneficiary

of electric vehicle (EV) adoption globally as differential assemblies and gears are a critical component to

manage high torque requirements in EV. In FY21, EV contributed 14% of revenues, out of which Tesla

accounts for 13%. Sona BLW has won significantly large orders from Tesla and is the sole supplier to

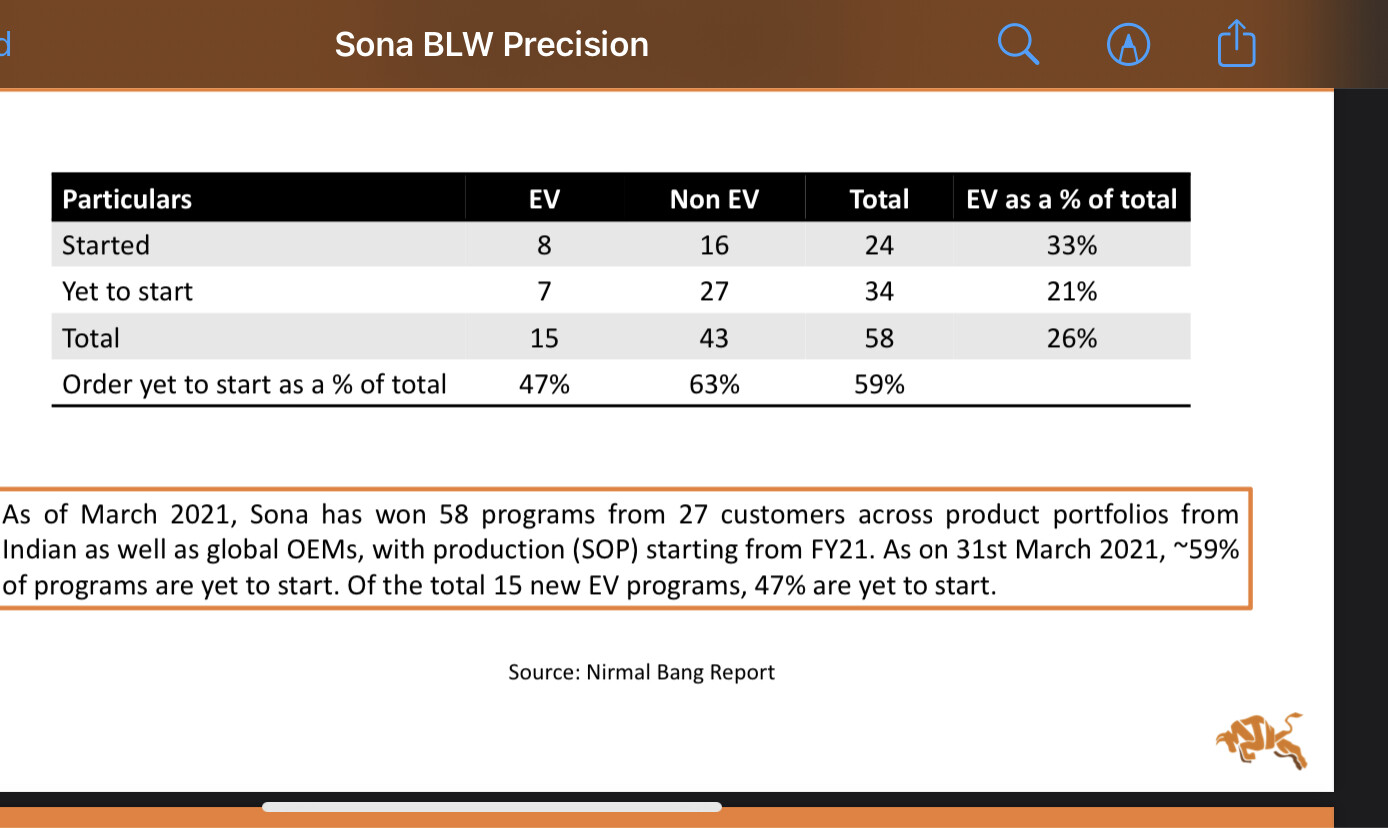

Tesla’s China plant. Beyond this, it has a strong order book, winning 15 deals from 10 EV manufacturers.

Sona BLW’s strength comes from in-house design of dies, knowledge of metallurgy and in-house warm

forging, making it one of the most integrated players in the differential gears market,

10 Likes

I have concerns about the statements made by India Capital Growth Fund in their article from June 2021 . It does sound very dubious and I have a suspicion they are making mis-leading claims. Sona themselves are very shy of naming their OEMs.

Tesla brand is known for the pioneering efforts in EV side and I believe ICGF is riding on their fame to dishonestly push their case for Sona Comstar .

I am willing to be proven wrong.

Sona BLW has won significantly large orders from Tesla and is the sole supplier to

Tesla’s China plant

Sona Comstar official statement on News item linking them to Tesla

6 Likes

Could be. Possibly best way to verify it is to get export data and then verify

Will update here once I get it

8 Likes

If Sona com is the main supplier to Tesla in China definitely they will be in India also

as on date there may not be any agreements for Tesla India that is what is clarified by management.

1 Like

Agreed.

But I would have expected that management would have clarified that in the press release too - that they are the sole supplier for Tesla China

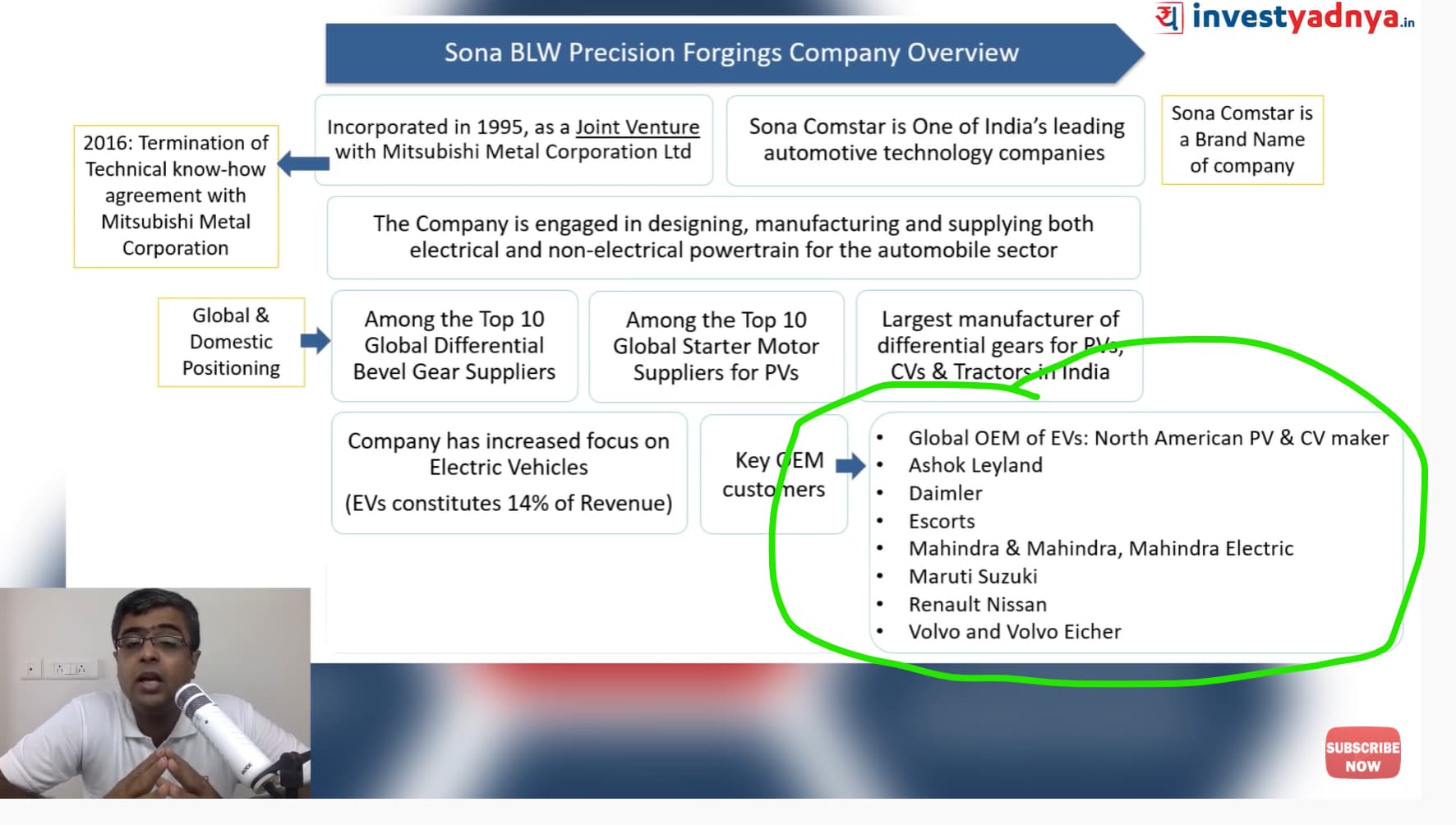

There was a screenshot from one video from a private investor which listed the companies Sona was working with . Let me grab that. I dont recall seeing Tesla in it.

I remember in one of there interviews with Sunjay, they didn’t want to disclose any information of there clients.

True , The Management was hesitant to reveal any info on relation with Tesla. Though Until we get the export Data of Sona , Can’t comment anything

2 Likes

Added the link to the talk…

3 Likes

Link : Sona BLW IPO Review | Should you apply or not? Parimal Ade - YouTube

Video shows some of SOna Comstar customers. It does not include John Deere. There is another video which has a snapshot. Will find that too and post

How to believe this video prepared by some agency.

The credit rating, both long-term and short-term, of Sonacom, has been upgraded. [sonacom.pdf (2.1 MB)]. It looks expansion plan is very positive. Could anyone from the forum summarize the key points (+ve and -ve) of the credit rating here? It would be helpful for us. ![]()

1 Like

[SEBI | Sona BLW Precision Forgings Ltd - RHP] IPO documents

Tesla does not find a mention in their customer list from the IPO documents.

An with an explicit statement from the company that they arent supplying to Tesla, there isnt any further conclusions to make except for:

- India Capital Growth Fund is making a misleading claim .

I think there is a lot more to this company than whether they supply to Tesla or not. With every major player getting in the EV segment and small players emerging, sooner or later this company will benefit. Even if they dont get Tesla EVER, they will still be one of the leading players.

Disc :- Invested at low levels Without thinking of Tesla

5 Likes

IMHO, its a good company but exorbitantly priced with PE of 228 as per screener (based on EV euphoria). So all the positives seems like already in the price. So I am not sure any new investor would like to get into at this point. Once time correction sets in where profit growth will catch up with stock price, can be considered as good entry point. But knowing its a raging bull market, I may be proven completely wrong

Disclosure - mildly interested, not invested

4 Likes

This is exactly what my thinking is & was. However there are 2 schools of thought on these sort of high growth, high quality, high valuation companies:

- In the long term they might not create wealth because all positive are priced in.

- In the short to medium term as the co executes exceptionally & gets 30-50% cagr topline, the valuation will remain same, maybe increase, and investor/trader will make wealth.

#1 & #2 Are not opposite of each other. It’s possible that in short term some wealth can be generated but in longer term (10 years) wealth generated is negligible (of course looking at current company, company can change over time).

As an investor, I think it’s important to remain flexible, adaptable, reflexive. For that reason and that reason alone, I’ve decided to bet against myself by having a tiny ~1% position in the company. I treat this purely as a trading bet by having a well defined, quant stop loss criteria. The idea is more to understand whether any wealth can be generated in short - to - medium term.

I was given this advice by one of vp’s senior investors who said that as an investor we have 2 choices :

- Remain adamant, complain about lack of value, remain like old Buffett & look for value & watch real

value creation in new age companies from afar. - Remain flexible, adaptive, changing with the times, and be ready to invest into highly valued companies, with very strong durable competitive advantages, high growth, high industry tailwinds with a clear exit strategy.

I choose to be in category 1 for 95% of portfolio, but happy to experiment with 5% of Portfolio in category 2. I am most likely right & valuation do matter, but in the off chance that terrific business, exceptional true research & development can result in earnings that our current p/e calculation does.not capture (imagine what will happen if the magnet less motor project reaches fruition) I will be there to witness the story, learn from the experience, & bet bigger next time around, into the next sona comstar. ![]()

Disc: small position, biased

17 Likes

i think sahil bhai…this is the biggest dilemma when u r playing with disruptive companies…

at the start of the S curve (which literally is so steep nowadays that it looks like a J curve) the price looks super expensive…and it carries on being expensive for the good part of the expansion mode…

growth of revenue will beat estimates year after year and eventually sometimes in hindsight…high PE seems justified…

the catch here is…if u catch the curve wrong (when it seems like a disruption but its not)

then u pay a heavy price…

The expansion phase usually last 15 yrs…so even if u catch half of it…:u tend to make decent money…(no matter wut value u catch it)

3 Likes

This is calculated as EPS of 3.76 but if you consider consolidated EPS of last qtr i.e. 1.51, screener is showing just half of true forward EPS. I have had made a mistakes of looking at such obsolute numbers and just avoided many good stocks like for example Dmart etc. I have also seen many people highlighting such incorrect (obsolute) numbers, which makes people specially who are new to market and say read mostly about Buffet and Intelligent investors like books not to even investigate further. It’s true that stock is expensive but it is certainly not trading at 200+ PE. And stock price mostly about future prospects and growth. So I find it important to look at future prospectus instead of obsolute numbers.

6 Likes

i think that the best metric that comes in handy here is…

mcap/sales or mcap/forecasted sales

that gives a decent idea of valuation…rather than PE

1 Like

If Sona compounds it’s EPS at 25% CAGR for next decades ( could be possible as electric vehicles industry itself is suppose to grow at 25% plus CAGR ) you can easily compounds your wealth at 15 to 16 % CAGR from current price for next 10 years assuming if it still trades at 50+ PE. ( I haven’t considered inflation for this high level calculation)

Disc. Invested from lower levels

1 Like